Loan management software

for US lenders

One system for banks, credit unions, and fintech lenders to originate, service, and collect, wired to

the three bureaus, ACH and FedNow, and every state on the license.

Book a demo

Loan management software

at every step of the loan

White-label onboarding

Show personal, auto, or BNPL borrowers a white-label application. Capture each detail once, hook

in the KYC and KYB providers you trust, and grade risk on the file before it lands in the

underwriting queue.

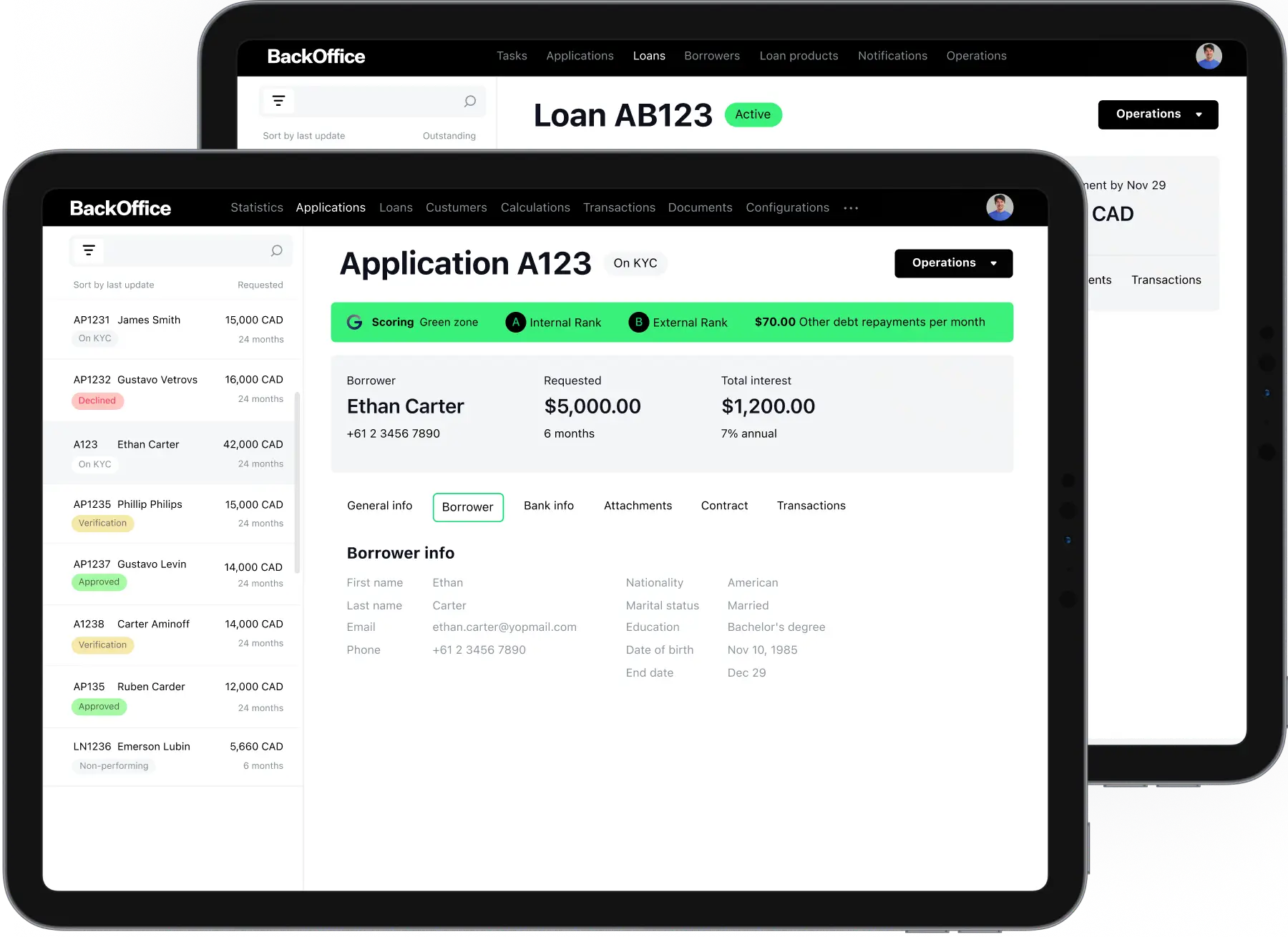

Rules-driven origination

Make one decisioning pass that reads Equifax, Experian, TransUnion, and aggregator cash-flow

data together. Edit rules, pricing, and document templates for installment, auto, or POS

financing, then reuse the same setup when the next product goes live.

Servicing on one ledger

Take payments on ACH and cards, send disbursements in real time over FedNow and RTP, and watch

the ledger update as it happens. Handle forbearance, payment plans, and rate changes off the

spreadsheet, and log a clean, audit-ready trail at each borrower touchpoint.

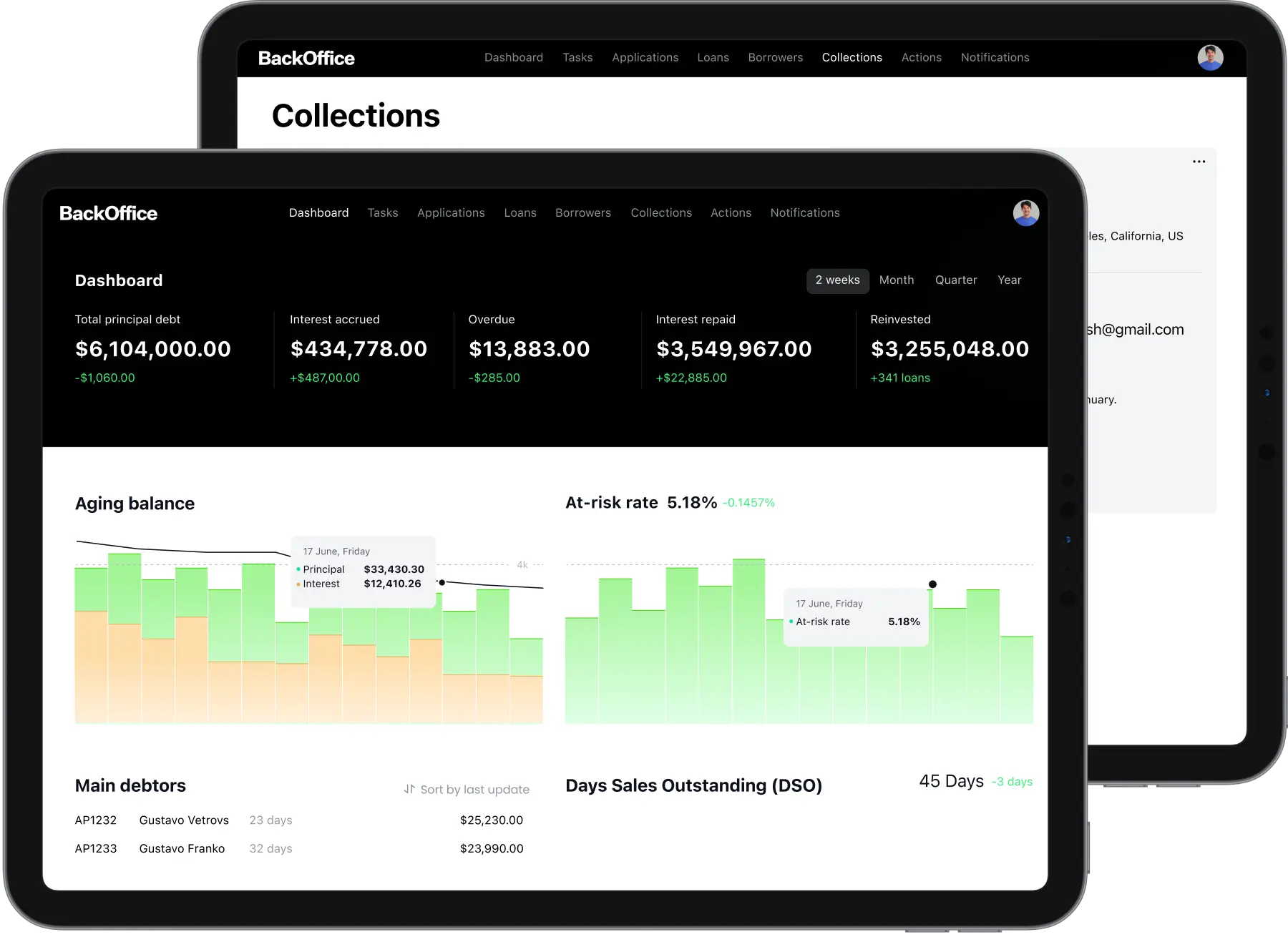

Rule-aware collections

Chase arrears within the contact rules you operate under, sort accounts by delinquency bucket,

reach out on the channels borrowers actually answer, and let AI match a recovery path to each

hardship case.

Get your lending

product estimate

in 3 minutes

STEP:

/

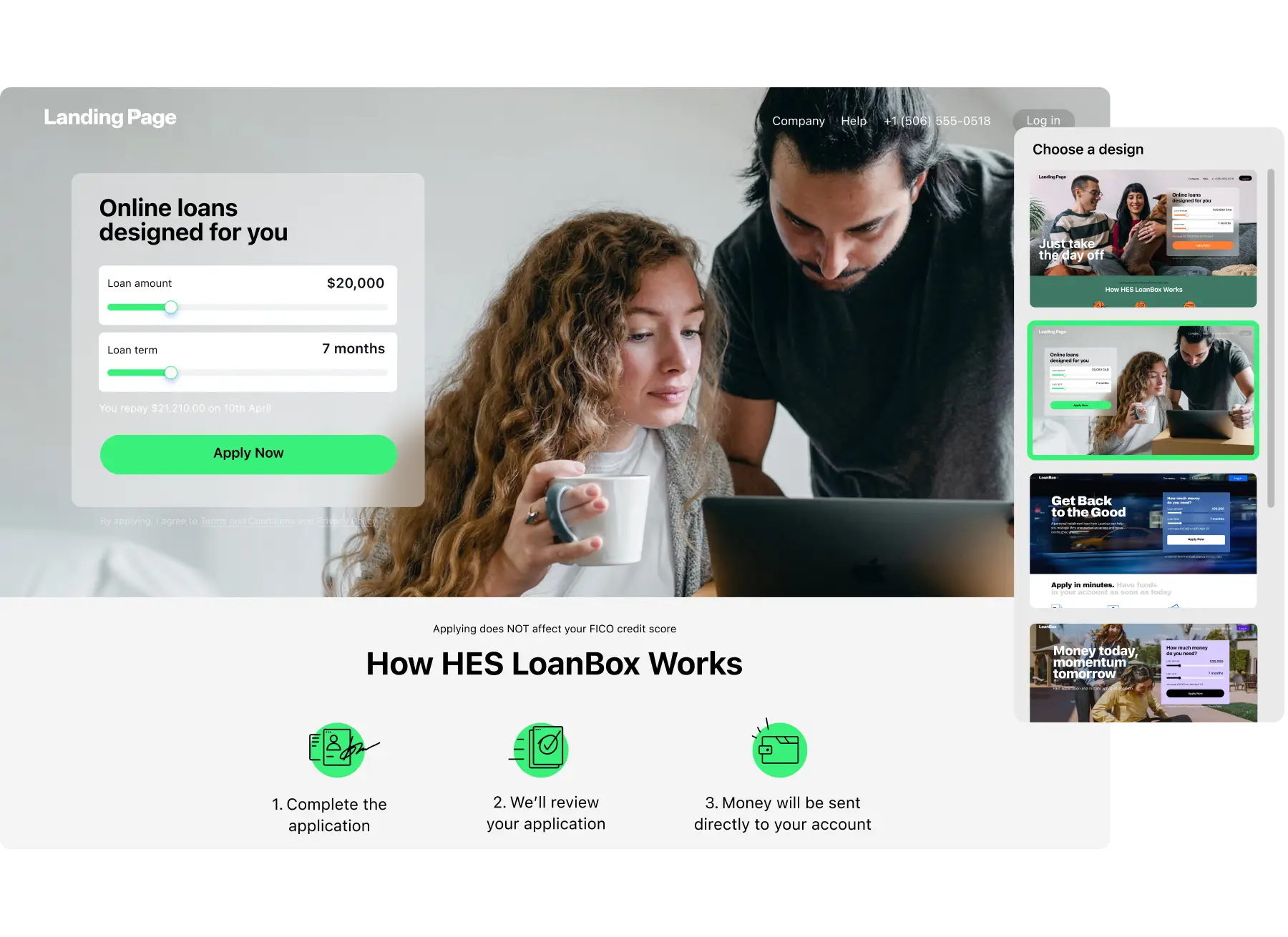

Borrower onboarding

Digital onboarding shaped to

US disclosure rules

The HES LoanBox loan management system moves an applicant from first tap to signed agreement, with

no long forms and no surprises on price. Gather just what underwriters need, hold an audit-ready

trail at each step, and keep your team off duplicate data entry.

Show the APR before they commit

Faster decisions without skipping checks

Keep borrowers close after funding

Grow through brokers and dealers

Loan origination

Faster loan origination,

run on AI scoring

Manual rekeying and weeks-old bureau pulls drag US consumer credit decisions out for weeks. Live

bank-data feeds, OCR across pay stubs and bank statements, and built-in e-signature make each

application a quick, defensible call, and trim document-handling cost by up to 90%.

Prove identity, then build the borrower file

Underwriting that matches your credit policy

Approve more of the right risk

Every loan product, one core

One core runs every product you offer, from personal and auto to BNPL and HELOC. Set

pricing, fees, schedules, and eligibility by configuration, not a developer ticket.

No-code application flows

Shape each lending journey on a no-code builder, with no wait on engineering to ship. Set

the approval gates and routing logic, then launch a new product in days as the rules change.

Permissions tied to each role

Lock borrower data behind permissions set per role, password policies, and two-factor login.

Every user action writes to an audit trail that holds up under examination and internal

review.

Agreements built in one pass

Assemble binding loan agreements from dynamic templates in moments. Cost-of-credit

disclosures, the promissory note, and repayment schedules build in one pass, worded to the

rules you lend under.

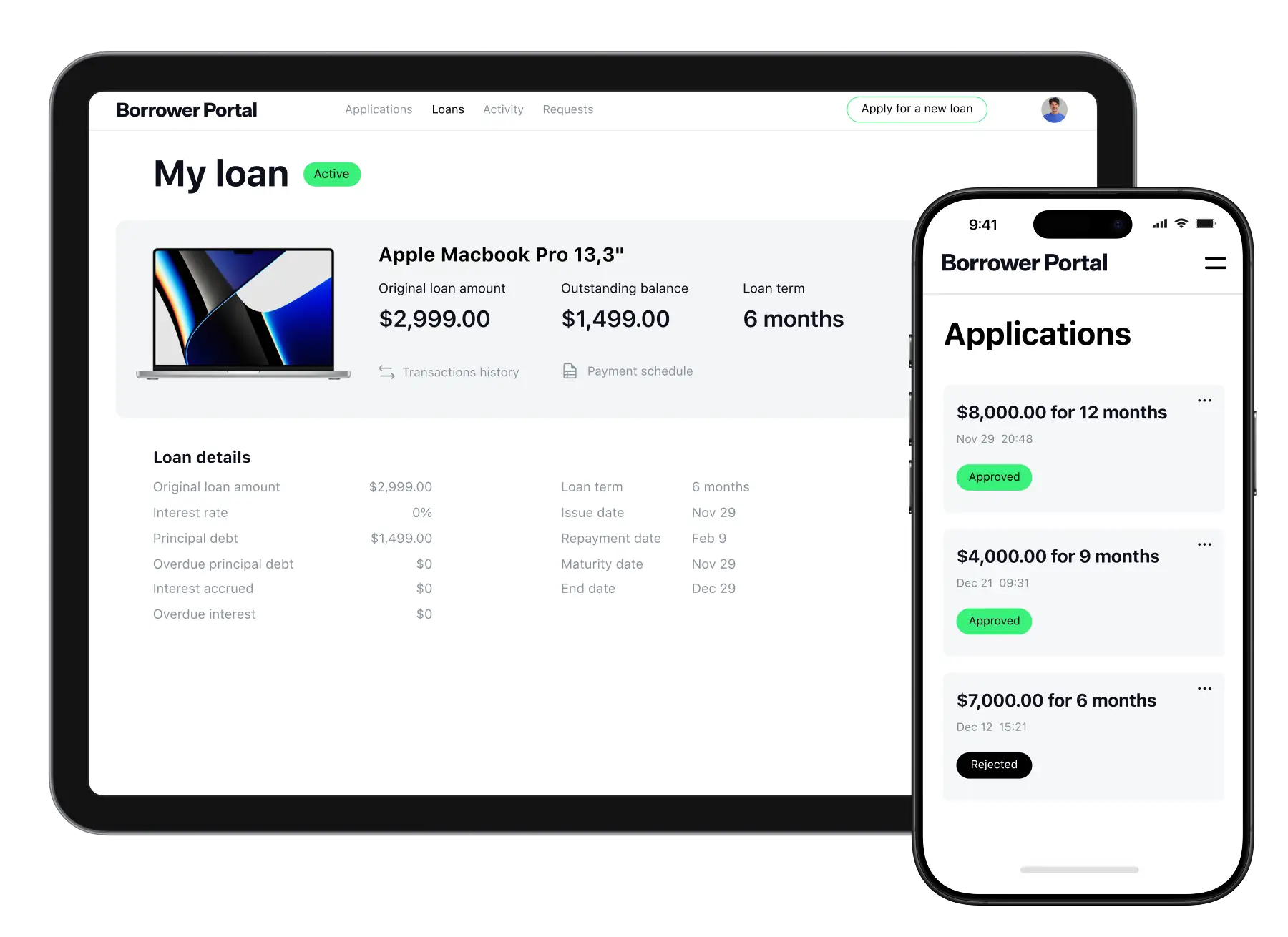

Loan servicing

Loan management software for the whole book

Spreadsheets plus a few loosely connected legacy tools quietly cost you margin and goodwill. HES

LoanBox carries every loan from funding to payoff on live data, terms you set yourself, and built-in

payments, so the book stays clean and ready for review.

From funding to payoff, hands-off

Change terms without a rebuild

Payments on US rails

Stronger loan books

through AI risk intelligence

Scoring your examiner can follow

Score predictively across the whole US lending path, from first screen to NPL forecasting.

The reason codes read clearly to your credit committee, an auditor, and a fair-lending

examiner.

AI accuracy on your own book

Tuned on your own portfolio, the AI model adds up to 3x in accuracy over bureau-only scores,

reading live transactions rather than a credit file pulled months back.

Pricing that tracks the risk

Tune thresholds by segment, spot repayment stress before it becomes arrears, and re-price as

rate moves change borrower cash flow.

Debt collection

Recover more with AI-led

debt collection software

In the US, conduct rules, state rate caps, and growing scrutiny of borrowers under strain turn

collections into a compliance question, not just recovery. HES LoanBox routes each account through

workflows built around affordability, hardship flags, and the contact and fee limits you work

within.

Automate the whole arrears workflow

AI-tuned strategy per account

Fees and interest within the legal caps

Reporting and analytics on the whole book

HES LoanBox puts the numbers your CFO and credit committee watch onto live dashboards. Pull raw data

for regulatory filings, define your own metrics, and slice the book by vintage, channel, or product.

100+ integrations for your US

lending stack

HES LoanBox slots into the systems your team already runs, with ready-made connectors for Equifax,

Experian, TransUnion, Plaid, MX, ACH, and FedNow, plus the core-banking, accounting, and KYC tools

beside them.

Why US lenders

choose HES LoanBox

Customization without limits

Reshape modules, rework the borrower flow, and wire in any US service from the bureaus to

payment rails, with the option to own the source code, no lock-in.

Pricing you can actually read

You pay for the license, and the only add-on is a custom build. Borrowers, partners, and

staff seats are all unlimited, with no per-seat fee as volume grows.

Launch in 3 months

A standard setup goes live in roughly 3 months. Lend sooner, reach ROI quicker, and keep

tuning the platform as you grow.

US lending expertise

Work with analysts and engineers who have spent more than a decade building and running

lending products for banks, credit unions, fintechs, and specialty lenders.

Security at bank grade

ISO 27001 certified and SOC 2 aligned. Run on AWS, Google Cloud, hybrid, or on-premises,

over a hardened Java LTS stack that stays current with regular updates.

Support that stays close

Reach a support team that knows US lending and sits in your time zone.

HES FinTech has been our reliable technology partner since 2012. I believe much

of our success is due to the well-architected HES LoanBox solution.

HES FinTech offers comprehensive front-to-back solutions with integrations. Our

machine learning platform will allow clients best-in-class investment advice.

In just 6 months, we went from storing all our data in Excel to a fast,

reliable, and user-friendly platform that caters to our specific needs.

HES FinTech developed our lending software and predictive analytics. Their

expertise delivered automation, clear UI/UX and customer portal.

The LMS provided flexible repayment options, automated restructuring and

branch-level management, enhancing efficiency and risk mitigation.

Security

Deployment

Tech stack

Security built to ISO 27001

ISO 27001 certified, SOC 2 aligned, with a secure SDLC behind it: full data

encryption, role-based access, audit trails ready for examination, and

hardened hosting end to end.

Learn more

Cloud, hybrid,

or on-premises

HES LoanBox deploys on AWS, Google Cloud, on-premises, or a hybrid mix,

matching your IT estate and the data-residency line your board sets.

Open-source

under the hood

HES LoanBox sits on free, open-source foundations: Java LTS, BPMN 2.0,

Camunda, and the Form.io modeler. Nothing carries a license fee beyond the

platform source code, so your team always knows what it owns.

The 2026 reality of

US lending

$15.9B

lost to fraud in 2025

Americans reported

$15.9 billion

in fraud losses in 2025, up from $12.5 billion the year before. Layered identity, document,

and device checks stop more of it before any money moves.

6.6M

complaints to the CFPB in 2025

The CFPB logged

6.6 million complaints

in 2025, with debt-collection complaints up 86% over 2024. Clean audit trails and quick

dispute handling keep them from escalating.

$18.8T

in US household debt

US household debt hit a record

$18.8 trillion

in the first quarter of 2026, and balances keep growing faster than headcount. That gap

pushes lenders to cut the cost of every decision they make.

4.8%

of balances are delinquent

By the first quarter of 2026,

4.8%

of outstanding consumer debt sat in some stage of delinquency. Early-warning scoring and

configurable workflows flag stress on an account before it becomes a charge-off.