Consumer lending software for

digital lenders

Built for banks, credit unions, and fintech lenders. Personal loans, installment loans, revolving

credit, POS finance, and HELOCs — all on one platform.

Book a demo

Flexible software for the full

consumer lending lifecycle

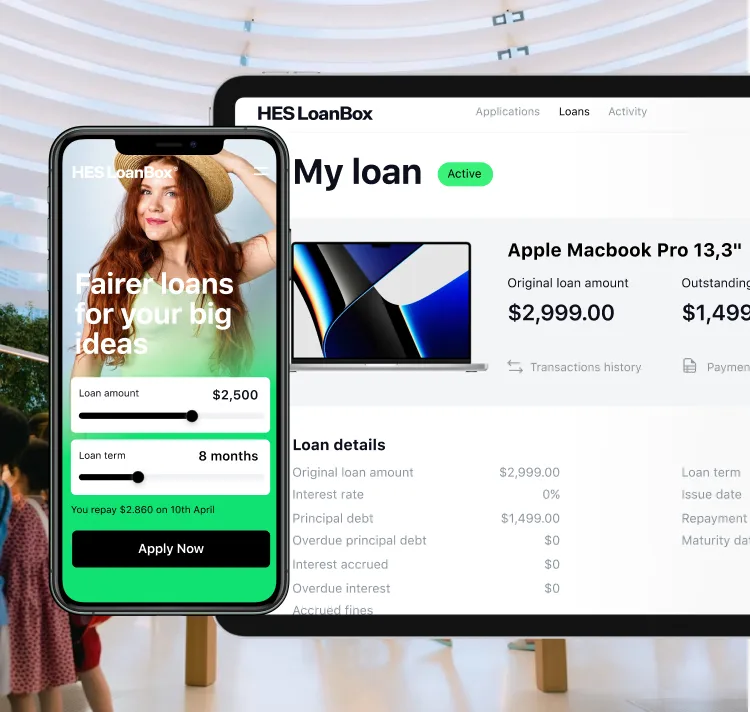

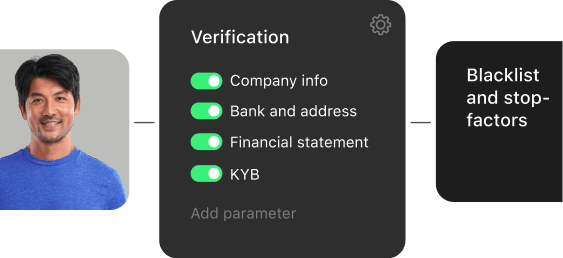

Effortless onboarding

Launch a branded borrower experience optimised for any device or channel.

Give personal loan applicants a simple way to apply, check eligibility, and submit documentation. Powered by KYC verification, automated data validation, and intelligent document processing.

Give personal loan applicants a simple way to apply, check eligibility, and submit documentation. Powered by KYC verification, automated data validation, and intelligent document processing.

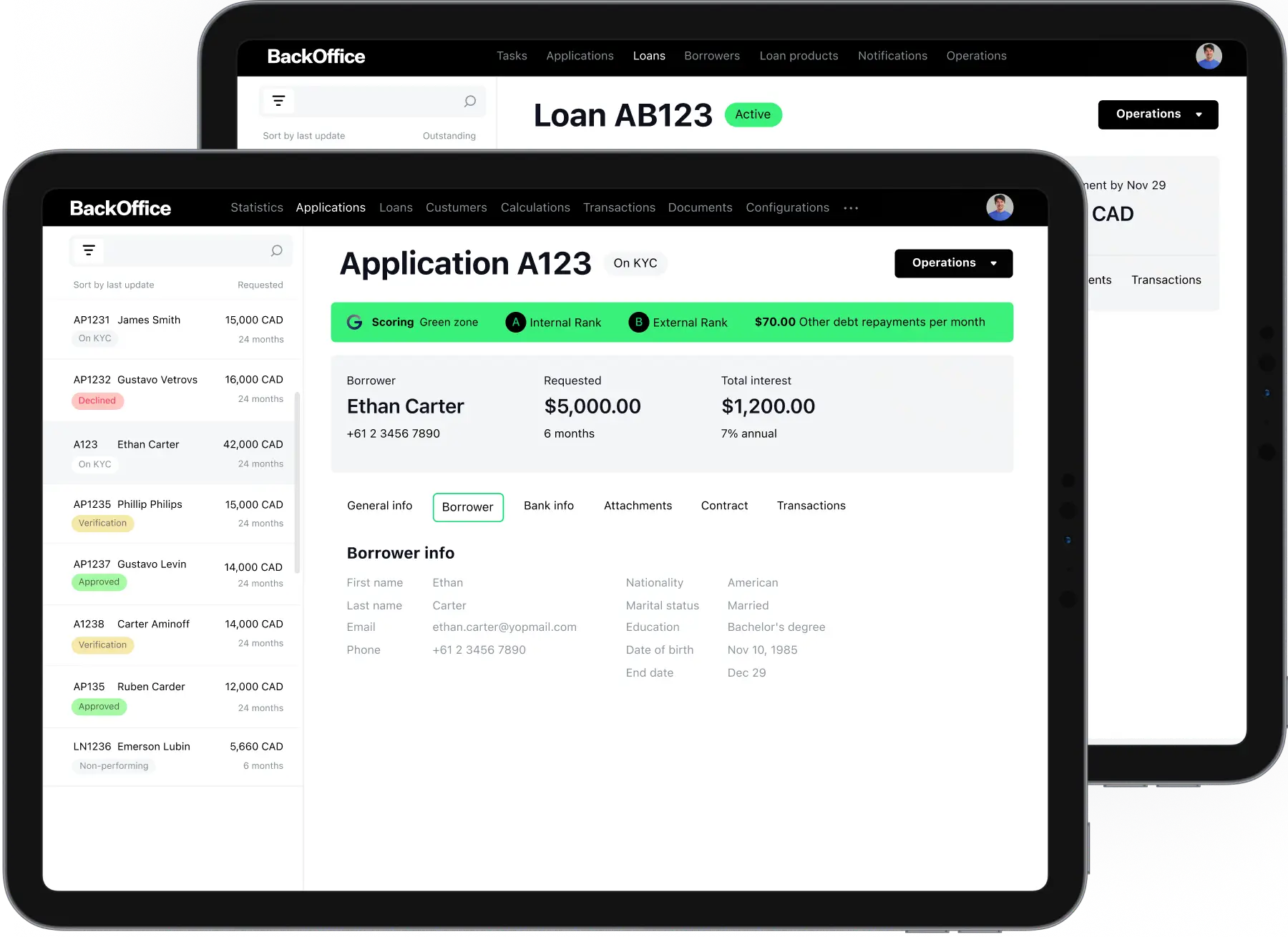

Precise origination

Accelerate credit decisions with configurable underwriting workflows, AI-driven scoring models,

and comprehensive third-party data integrations.

Structure and manage consumer loan products with custom eligibility parameters, dynamic pricing logic, and tailored risk frameworks.

Structure and manage consumer loan products with custom eligibility parameters, dynamic pricing logic, and tailored risk frameworks.

Reliable servicing

Manage repayment schedules, disbursements, and borrower communications from one unified

platform.

Keep operations and customers fully aligned with real-time portfolio visibility and automated lifecycle management.

Keep operations and customers fully aligned with real-time portfolio visibility and automated lifecycle management.

Intelligent collection

Improve recovery performance on overdue consumer loans through AI-powered outreach, predictive

delinquency analytics, and flexible restructuring options designed around each borrower's

circumstances.

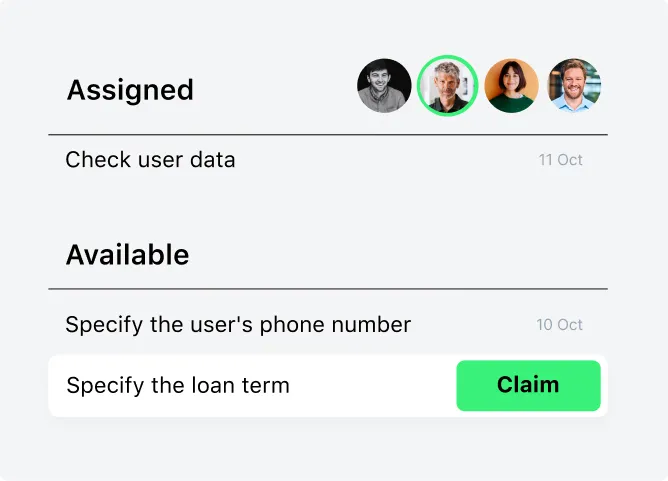

Smart task management for consumer lending teams

Move every consumer loan application forward without bottlenecks. Auto-assign tasks by role and

workload, track SLAs in real time, and keep underwriting, verification, and servicing teams

perfectly aligned.

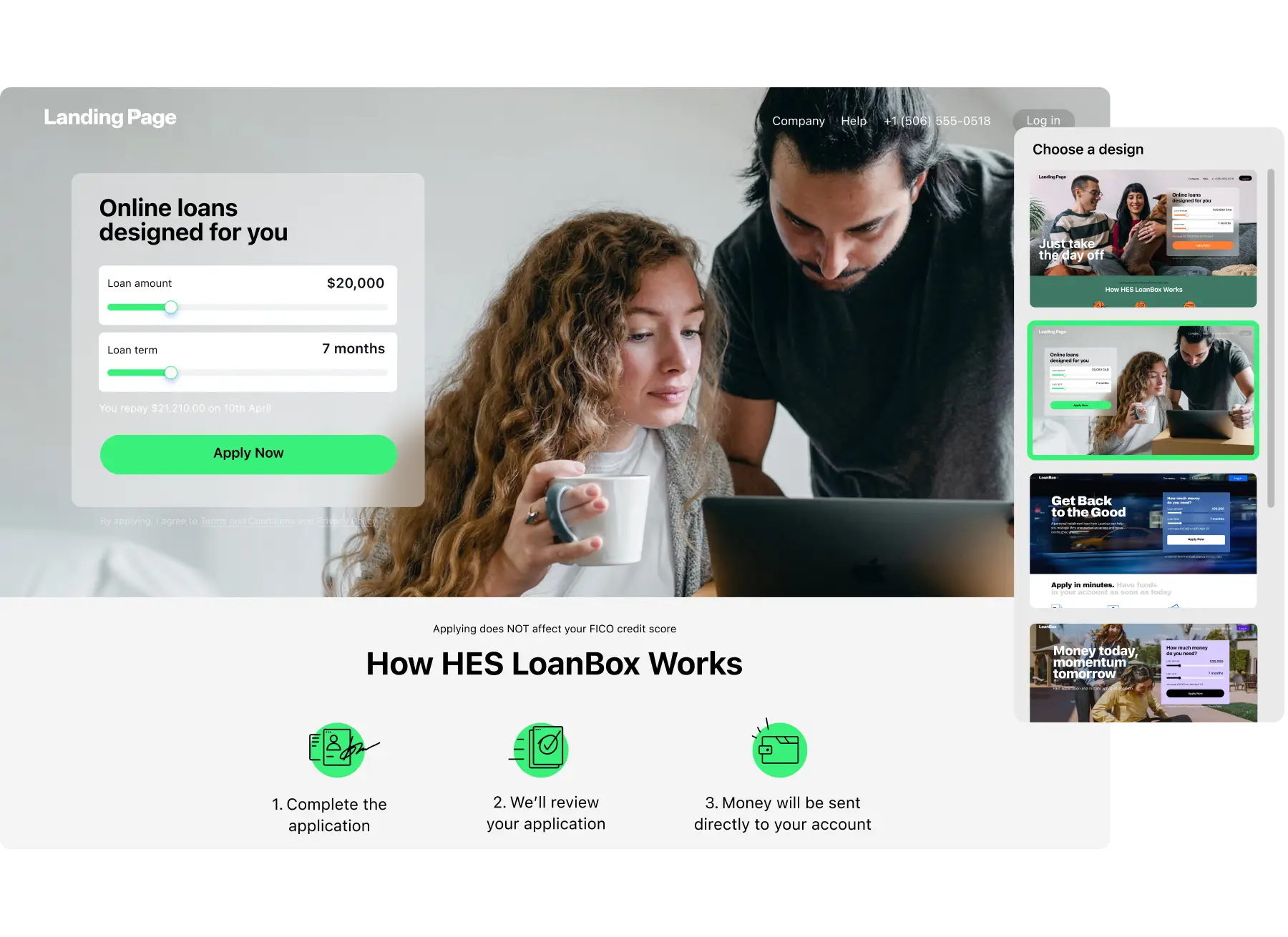

Online onboarding

Consumer lending software that

drives applications to approval

Turn interest into approved applications without friction. Give consumers a fast, fully digital path

to personal financing — and give your team the automation tools to process more applications with

less manual effort.

Boost completion rates from the first step

Cut approval times without cutting corners

Keep borrowers engaged after disbursement

Grow through retail and broker partnerships

Get your lending

product estimate

in 3 minutes

STEP:

/

Loan origination

Cut consumer loan

origination time

with AI and

automation

Slow reviews and patchy data quietly kill conversion and inflate default rates. AI-driven

verification and underwriting turn every consumer application into a fast, confident, compliant

decision.

Instant identity verification and borrower profiling

Configurable underwriting at any speed

AI credit decisioning that grows your book

Self-learning scoring by GiniMachine

Paperless from application to signature

and much more

Unlimited product configuration

Launch any consumer loan product your market needs, from personal loans and installment

plans to revolving credit and co-branded financing. Configure rates, fees, schedules, and

eligibility rules per product or segment, no developers required.

Automated contract generation

Generate legally binding consumer loan agreements in seconds using dynamic templates with

merge variables. Cut drafting errors, speed up disbursement, and stay aligned with consumer

protection rules across every jurisdiction you operate in.

Smart notification templates

Build SMS, email, and push templates with dynamic variables to automate every borrower

touchpoint, from application status and approval confirmations to repayment reminders and

renewal offers.

Role-based security and access control

Protect borrower data with granular role-based permissions, password policies, two-factor

authentication, and device-level access rules. Full activity logs keep you audit-ready

across every user action.

Multichannel communication

Automate outreach across SMS, email, and in-app channels with rule-based triggers tied to

borrower behavior and loan status. Keep consumers engaged at every stage of the lifecycle

and take load off your support team.

No-code workflow builder

Design and adjust consumer lending workflows visually, no developers required. Map

application flows, set approval logic, build conditional decision trees, and launch new

processes in days.

Configurable consumer lending workflows

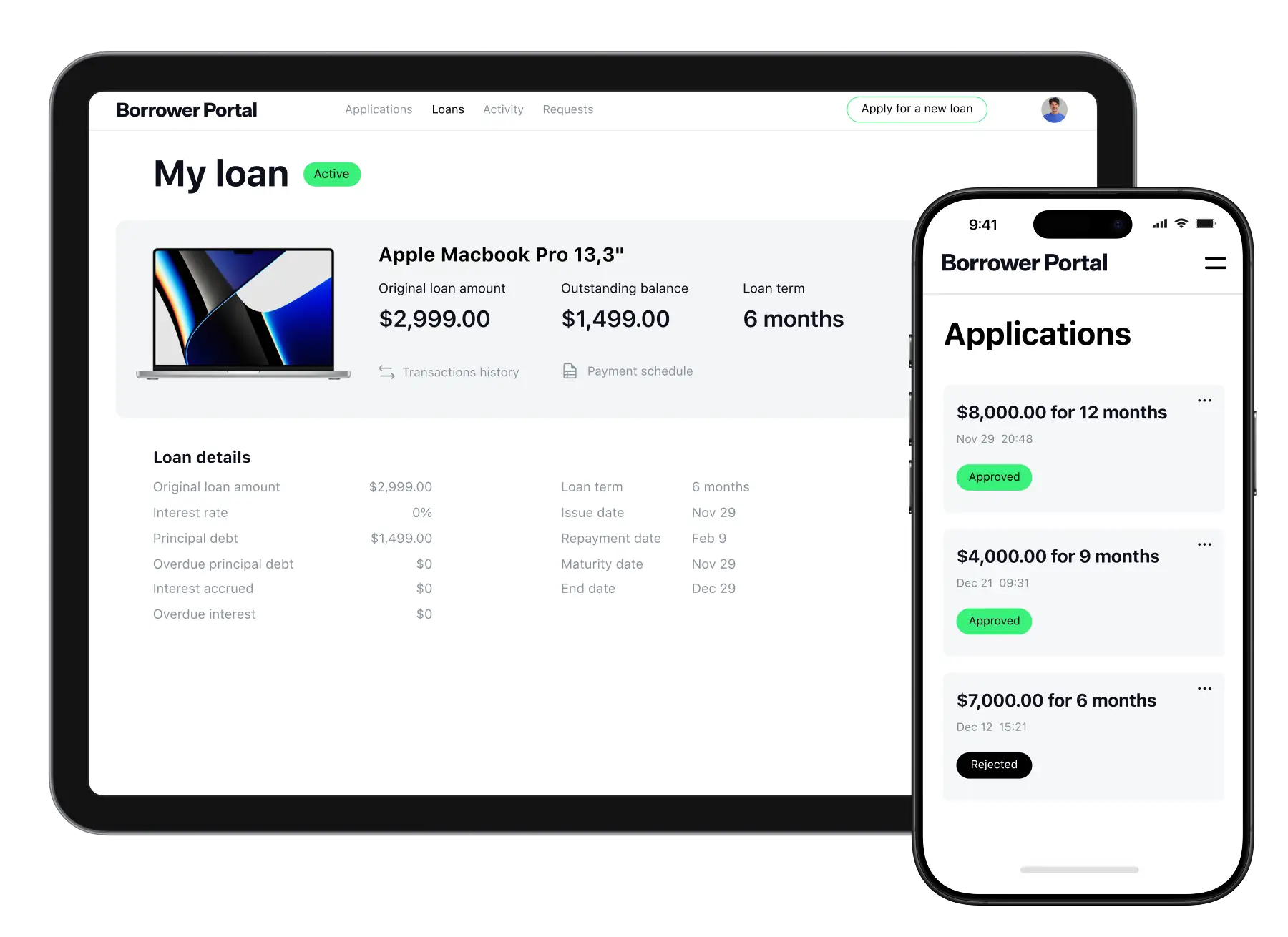

Consumer loan servicing

Complete consumer loan management software

Disconnected systems and manual reconciliations slow teams and erode margins. A unified consumer

lending system automates the full loan lifecycle with real-time data, flexible terms, and built-in

payments for faster, cleaner servicing.

Automate the full consumer loan lifecycle

Adjust loan terms, schedules, and payments

A complete borrower view for faster service

Keep ledgers and transactions in sync

Maximize loan portfolio performance

with AI risk intelligence

Scoring made clear

Apply predictive scoring across the full consumer lending journey, from pre-KYC filtering to

NPL forecasting, with transparent, explainable, and audit-ready outputs.

AI-driven risk precision

Sharpen consumer credit decisions with integrated AI that delivers up to 3× better accuracy

than traditional scoring models.

Smarter risk control

Set custom risk thresholds, anticipate defaults early, and rebalance pricing to keep your

consumer loan portfolio profitable.

Consumer loan collections

Boost recovery with automated

consumer loan collections

Manual collections move slowly, cost too much, and leave borrowers with a bad taste. Let AI handle

outreach, scoring, and penalties: it predicts who will repay, picks the right channel, and keeps

every consumer loan compliant.

Automate the full recovery workflow

Tailor every recovery action with AI

Penalty management built for compliance

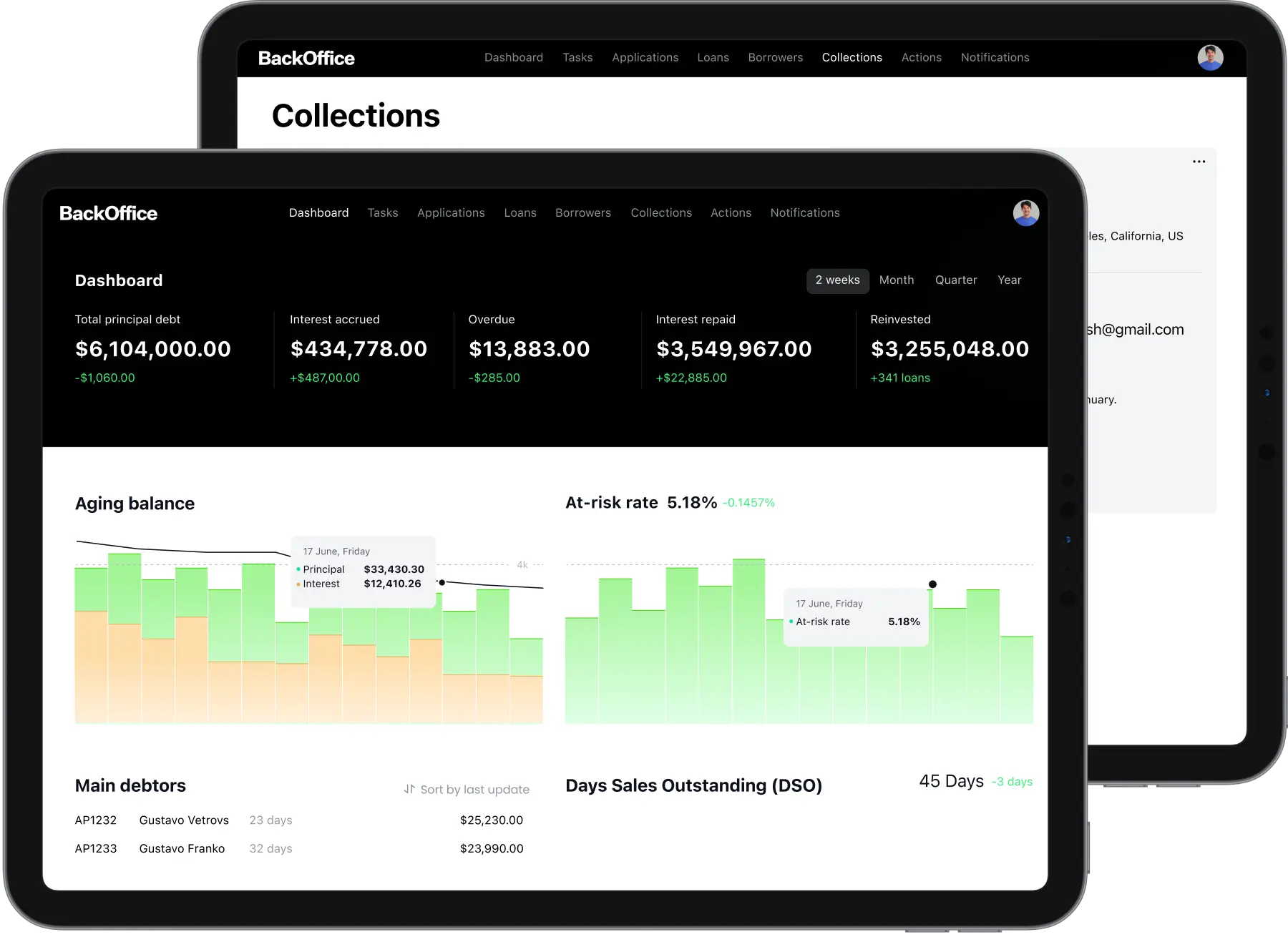

Consumer lending reporting and analytics

HES LoanBox builds interactive dashboards around the consumer lending KPIs your team actually uses.

Export raw data, configure custom metrics, and slice your portfolio any way your business needs.

100+ integrations to power

up your lending system

With flexible connection options and full customization, HES LoanBox provides a broad ecosystem of

integrations that enhance consumer operations across onboarding, scoring, payments, communication,

analytics, and core banking.

What you get by choosing

our consumer lending software

Unlimited customization

Customize endlessly: tailor modules, add features, adjust interfaces, and integrate with any

service — from payments to credit bureaus.

Transparent pricing

HES offers simple pricing: you pay for the license, with extra costs only for custom

features. Unlimited internal users and borrowers included.

3-month product launch

Go live in just 3 months. Start lending fast and see ROI sooner with a ready-to-deploy

consumer lending platform.

Industry expertise

Work with business analysts who bring 10+ years of consumer lending experience across the

US, EU, and emerging markets. Built by lenders, for lenders.

Proven security

ISO 27001 and SOC 2 certified. Hosted on AWS or Google Cloud with a secure Java LTS stack

and regular updates.

Dedicated support

Get fast, expert help from our dedicated support team — whenever you need it.

HES FinTech has been our reliable technology partner since 2012. I believe much of our success is due to the well-architected HES LoanBox solution.

HES FinTech offers comprehensive front-to-back solutions with integrations. Our machine learning platform will allow clients best-in-class investment advice.

In just 6 months, we went from storing all our data in Excel to a fast, reliable, and user-friendly platform that caters to our specific needs.

HES FinTech developed our lending software and predictive analytics. Their expertise delivered automation, clear UI/UX and customer portal.

The LMS provided flexible repayment options, automated restructuring and branch-level management, enhancing efficiency and risk mitigation.

Security

Deployment

Tech stack

Enterprise-grade

security

ISO 27001 certification, SOC 2 and SDLC ensure consistent security across

all operations, supported by full data encryption, role-based access

control, and a secure hosting infrastructure.

Learn more

Built on cloud

technologies

HES FinTech consumer lending solution can be deployed on-premises or in the

cloud of any chosen provider.

Powerful

backend tools

HES Fintech builds solutions using free and open-source solutions, like Java

11, BPMN 2.0, Camunda, and Form.io modeler. This approach allows us to

exclude any additional licensing fees, except for the platform's source

code.

The 2026 reality of

consumer lending

75%

of credit unions on legacy systems

Up to

75% of credit unions still operate on legacy loan origination systems that don't offer true

automation. Modernization is no longer optional for lenders competing on speed.

2008-level

consumer delinquencies in 2025

US credit card and auto loan delinquencies have climbed to

levels not seen since the 2008 financial crisis. Static scorecards and manual reviews can't keep

up.

+89%

CFPB debt collection complaints YoY

CFPB debt collection complaints nearly doubled year-over-year, climbing from 109,900 in 2023 to 207,800 in 2024. Every compliance gap is now a

measurable regulatory cost.

$3.3B

synthetic identity fraud exposure

US lenders faced over

$3.3 billion , in synthetic identity fraud exposure in 2024 and 44% of FIs now rank it as their top

tracked threat.

Start lending

in just 3 months

While you focus on deals, HES FinTech handles the platform.