PayDay loan software for

short-term lenders

Made for storefront and online short-term lenders. Single-payment payday loans, installment advances,

and small-dollar lines of credit, all from one configurable platform.

Book a demo

Purpose-built PayDay loan software

for the full lending cycle

Rapid onboarding

Launch a fully branded applicant experience optimised for speed and simplicity on any device.

Give borrowers a fast, transparent way to apply, verify identity, and receive a decision in

minutes. Underpinned by KYC compliance, automated affordability checks, and instant document

capture.

Confident origination

Make precise short-term lending decisions using configurable credit rules, AI-enhanced risk

scoring, and real-time access to income and banking data. Define payday loan products with

custom rollover policies, fee structures, and borrower eligibility thresholds.

Controlled servicing

Manage loan terms, repayment dates, and borrower communications from a single, compliant

platform. Maintain clear operational oversight across your payday portfolio with automated

payment tracking and proactive borrower engagement.

Effective collection

Maximise repayment rates on short-term delinquencies with AI-triggered outreach,

salary-cycle-aware retry logic, and flexible repayment arrangements that resolve arrears before

they escalate.

Get your lending

product estimate

in 3 minutes

STEP:

/

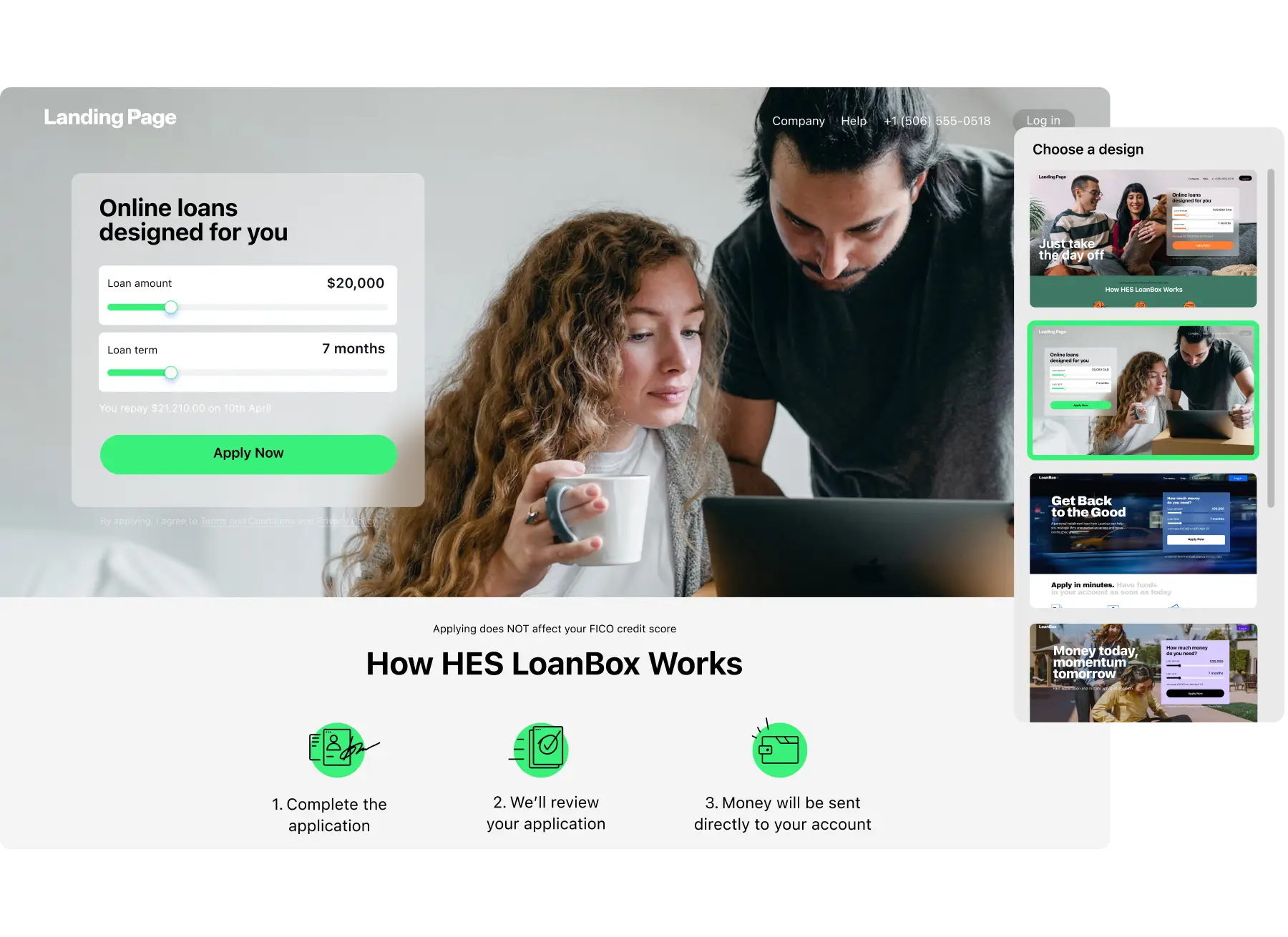

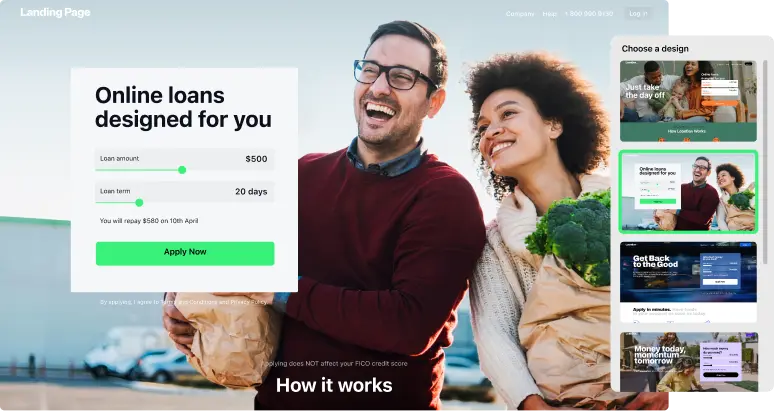

Digital onboarding

Payday loan software that takes

applicants from tap to payout

A short-term borrower will not wait around. The flow runs fully online, from request to payout, so

applicants self-serve and the team relies on automation to handle far higher application counts

without extra effort.

Make the cost clear before they apply

Approve in minutes, not by tomorrow

Hold repayment steady after payout

Add storefront and referral channels

From browsing to applying in minutes

Landing Page

Agent Portal

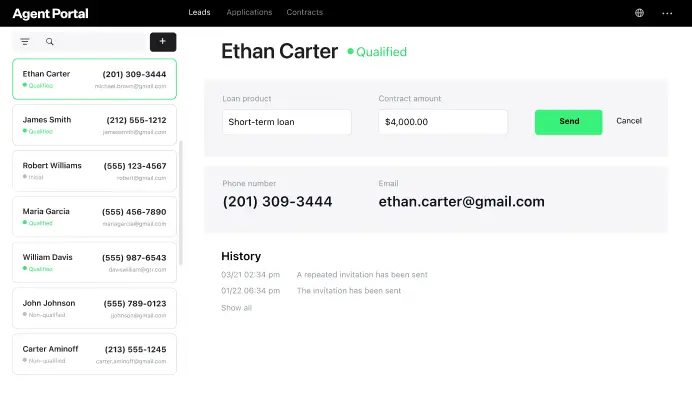

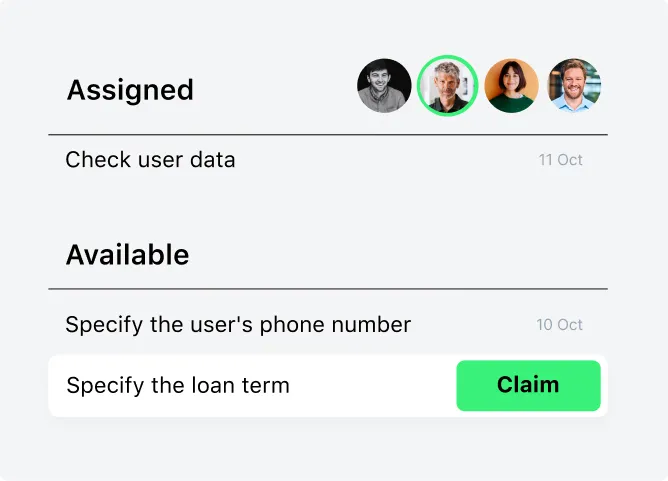

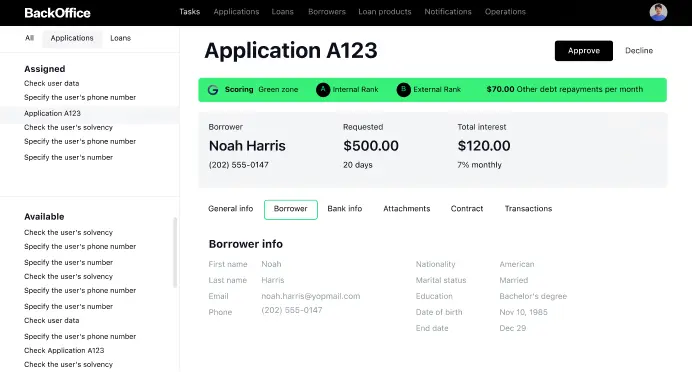

Keep short-term lending teams moving as one

A short-term loan dies in handoffs. Each task lands with the agent who fits, picked on role and live

workload, SLAs stay visible, and verification, underwriting, and collections share one view.

Loan origination

Payday loan software that cuts

decision time with AI

In short-term lending, a slow yes is a lost borrower, and a careless one is a default. Automated

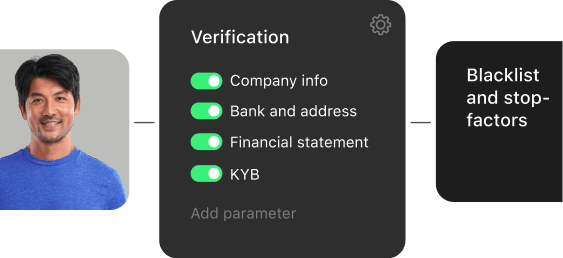

verification and AI underwriting turn each application into a quick, defensible decision.

Confirm who they are before underwriting

Underwrite at the speed each product needs

Score with rules plus AI to lend wider, safer

GiniMachine scoring that sharpens itself

No paper from first form to signed contract

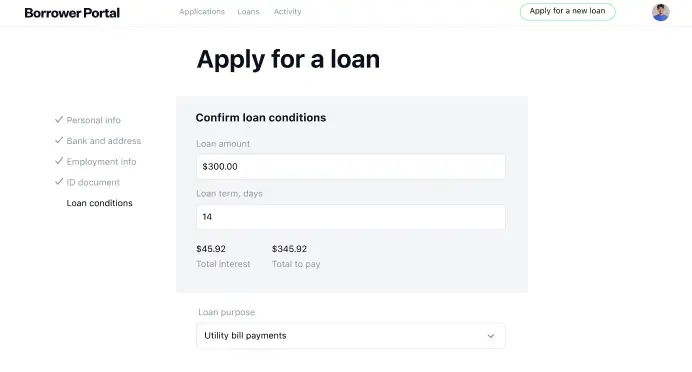

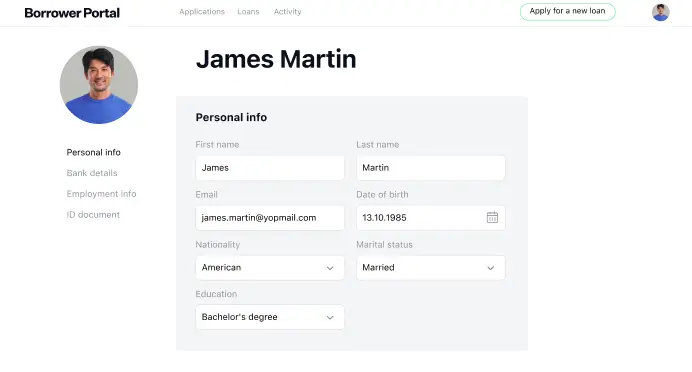

Self-service space for borrowers

Application flow

Borrower profile

Decision-making

and much more

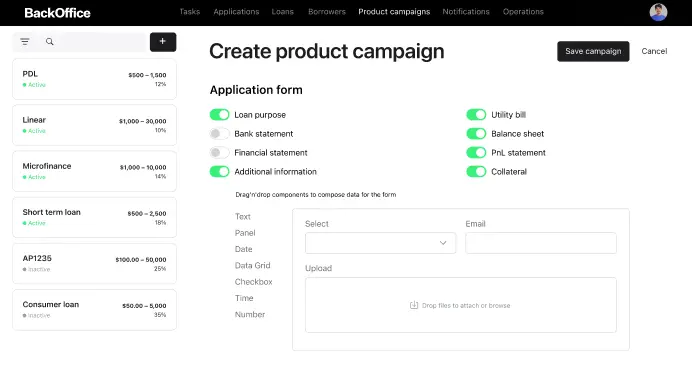

Configure any payday product

Stand up whatever short-term product you sell: single-payment payday, installment advances,

or a small credit line. Tune fees, rates, due dates, and who qualifies, by product or by

segment, with zero developer time.

Auto-generated loan agreements

Dynamic templates with auto-filled fields turn out a binding short-term agreement in

seconds. Drafting errors are gone, payout is faster, and each contract holds to the policy

you apply in every state you lend.

Custom notification templates

Compose text, email, and app-alert templates, each driven by dynamic fields, to cover every

touchpoint: status, approval, repayment nudges tied to payday, and renewal offers.

Access control and data protection

Lock down borrower records behind role-level permissions you define, password rules you

control, and a second sign-in factor. Every action writes to a complete activity log, so the

record stays audit-ready.

Borrower outreach across channels

Push timed outreach to borrowers by rules that react to their behavior and loan status,

across the channels they use. Engagement holds through the whole term, and the support desk

handles fewer manual messages.

No-code process builder

Draw and change short-term lending flows visually, no engineering ticket required. Lay out

application paths, set approval logic, branch decision trees, and ship a new process in days

rather than quarters.

Automated decision processes

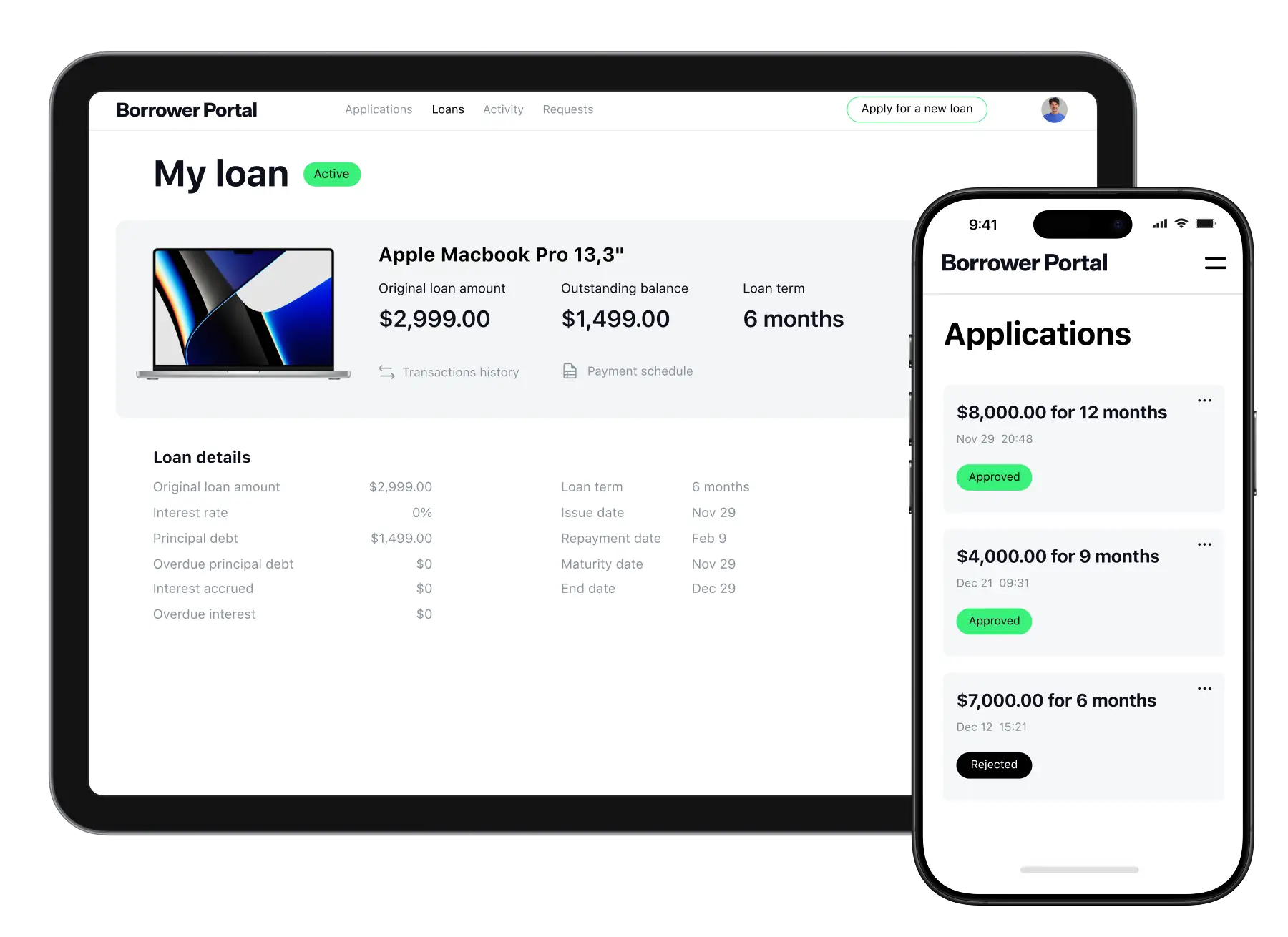

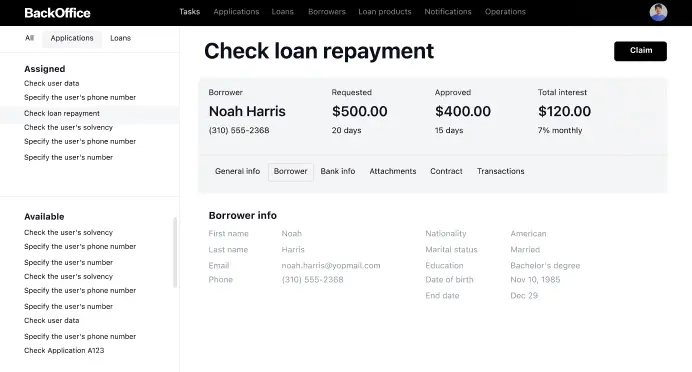

Loan servicing

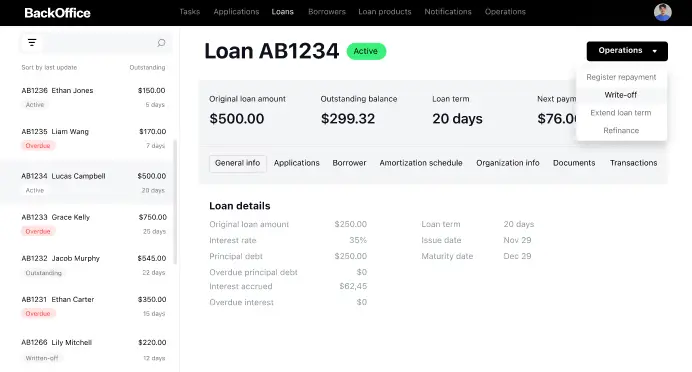

All-in-one payday loan management software

Juggling spreadsheets and separate tools drags servicing down and lets payments slip. Manage the

whole short-term loan, payout through final payment, in HES LoanBox, with live balances, terms you

can flex, and payments handled in place.

Run servicing on autopilot

Manage every product together

One screen per borrower

Payments you can rely on

Centralized hub for loan management

Deal management

Product engine

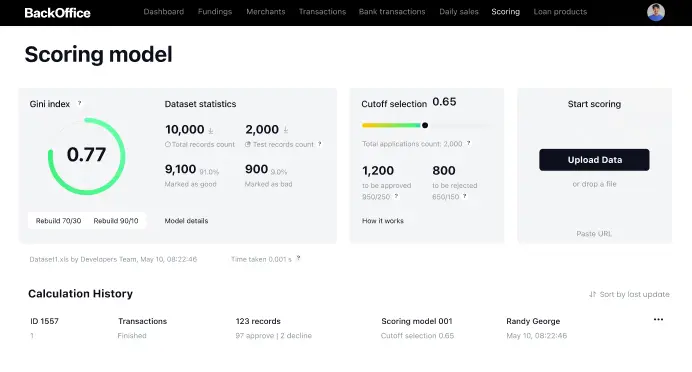

Scoring

Task management

AI risk intelligence that keeps

your short-term book profitable

Scoring you can defend

Scoring spans the short-term flow front to back, pre-KYC filtering through NPL forecasting,

with outputs you can explain and defend in review.

Sharper decisions with AI

Back each short-term credit call with GiniMachine AI, which scores up to three times sharper

than a standard scorecard.

Risk you stay ahead of

Define the risk thresholds that fit you, flag defaults before they hit, and move pricing to

keep the short-term book in the black.

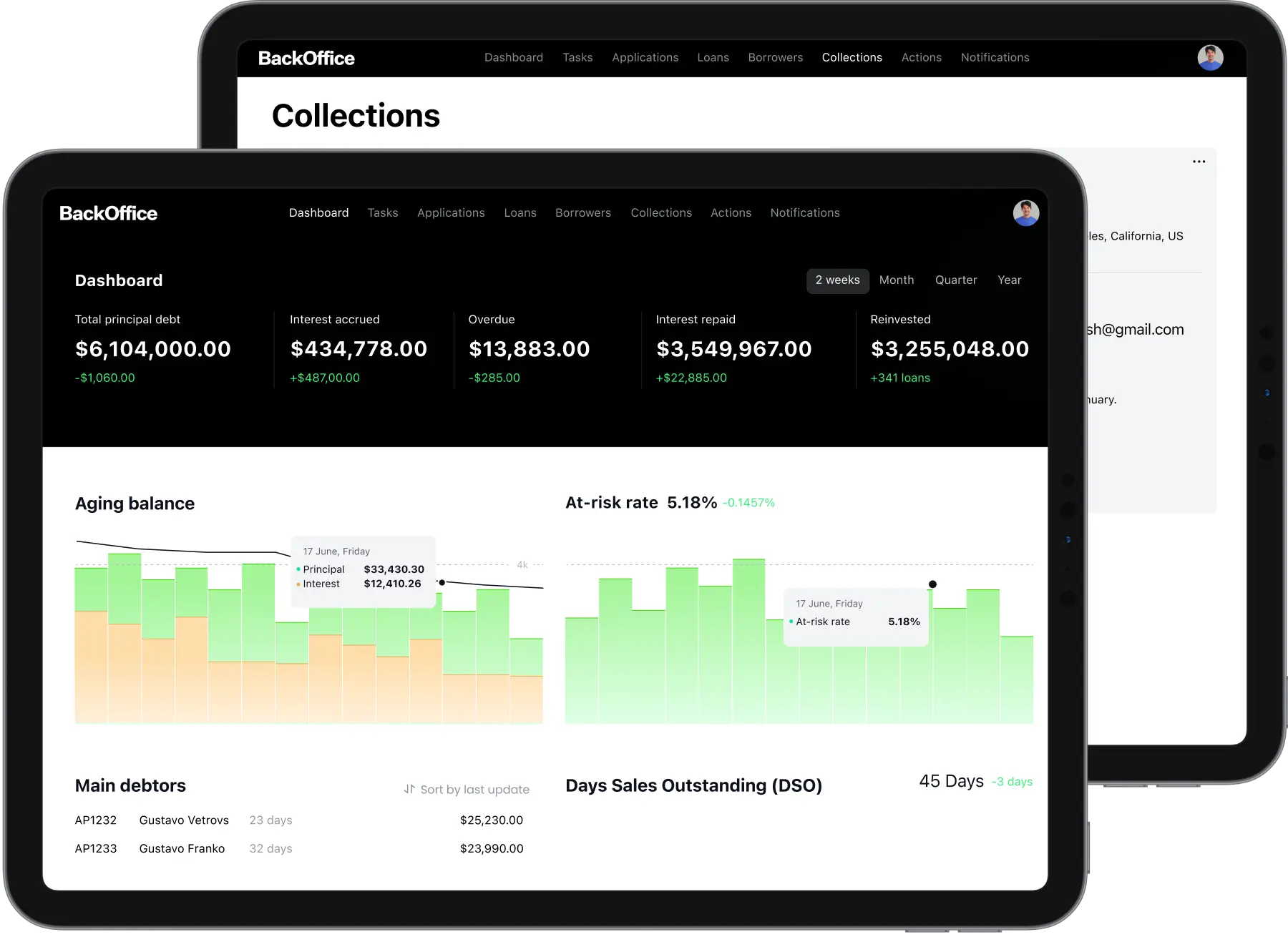

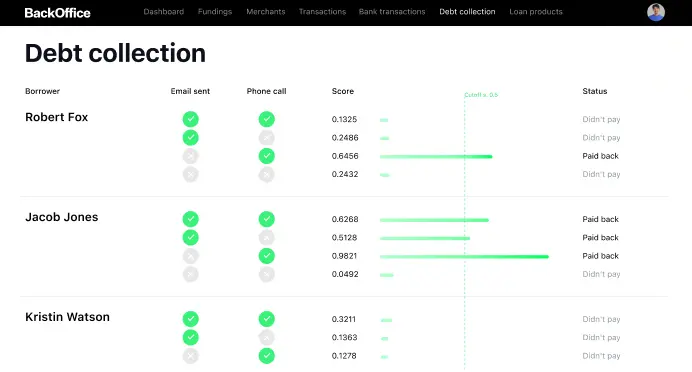

Loan collections

Recover more from automated

short-term collections

Short-term arrears pile up fast, and hand-worked recovery is slow and expensive. Let AI rank who

will pay, route each case to the channel that lands, and charge fees only inside the caps you have

set.

Put recovery on a workflow

Make each action borrower-specific

Head off missed payments early

Fees and penalties within your limits

Recover debts quickly and compliantly

Analytics built for short-term lenders

HES LoanBox shapes live dashboards around the short-term KPIs your team watches. Get the underlying

numbers out, set up whatever metrics matter, and view the book across product, vintage, and channel

as needed.

100+ integrations across the

payday lending stack

HES LoanBox links up with the tools a short-term lender depends on, connection options stay flexible

and fully customizable. Plug in onboarding, scoring, payments, messaging, reporting, and your core

system, fitted to the way you run.

What short-term lenders get

from our payday loan software

Configure, customize, or own the code

Short-term rules shift by state and product, so set caps, fees, rollover terms, and

eligibility yourself. Need more? Commission custom development, or take ownership of the

source code. There is no vendor lock-in.

Pricing that survives high volume

Small-dollar margins do not survive per-seat or per-loan fees. With HES LoanBox you license

the platform once, custom work aside, and add users and borrowers without a cap at any

volume.

Live, and lending, from 3 months

Launch a short-term product, or open a new state, from 3 months. It deploys ready to lend,

so you book loans early and reach ROI while rivals are still scoping.

Specialists in short-term lending

We have spent 14+ years on consumer and short-term lending across the US, EU, and emerging

markets. We know the model cold and build the software that runs it.

Security that passes audits

Borrower data sits behind ISO 27001 and SOC 2 certified controls, on a hardened Java LTS

stack and hosted on AWS or Google Cloud. Records stay audit-ready for every examination

cycle.

A team that answers, fast

When volume spikes or a question is urgent, you reach engineers who know your build and

respond quickly, not a ticket queue that goes cold.

HES FinTech has been our reliable technology partner since 2012. I believe much of our success is due to the well-architected HES LoanBox solution.

HES FinTech offers comprehensive front-to-back solutions with integrations. Our machine learning platform will allow clients best-in-class investment advice.

In just 6 months, we went from storing all our data in Excel to a fast, reliable, and user-friendly platform that caters to our specific needs.

HES FinTech developed our lending software and predictive analytics. Their expertise delivered automation, clear UI/UX and customer portal.

The LMS provided flexible repayment options, automated restructuring and branch-level management, enhancing efficiency and risk mitigation.

Security

Deployment

Tech stack

Security at the

core

ISO 27001 and SOC 2 certification and a secure SDLC keep protection steady

across operations. Data is fully encrypted, access runs by role, and hosting

is locked down.

Learn more

Run it in the cloud

or on-prem

Deploy HES LoanBox on-premises, in the cloud provider you choose, or across

a hybrid mix, whatever your security and ops teams need.

Open-source at the

foundation

HES FinTech keeps the backend on cost-free, open-source tooling: Java LTS,

BPMN 2.0, Camunda, and the Form.io modeler. No license fees stack up, just

the platform source code.

The 2026 reality of

payday lending

12M+

Americans borrow payday yearly

More than

12 million Americans

use payday loans every year, a high-volume, fast-turnaround market where manual processing

cannot keep pace.

391%

typical payday loan APR

A median storefront payday loan runs about

391% APR

at $15 per $100 over two weeks. Caps this tight on fees and interest must be set precisely

and logged behind every charge.

80%

of loans rolled over or reborrowed

Over

80% of payday loans

are rolled over or reborrowed within two weeks. Scoring real repayment capacity up front is

what separates a sustainable book from a churn of renewals.

20%

of payday borrowers default

Around

20% of payday borrowers

default over the course of a year. AI scoring that filters weak applications before payout

is the gap between a 40% NPL cut and a growing pile of charge-offs.