Loan management software

for Australian lenders

Built for lenders, ACL-holding banks, mutual banks, and BNPL providers. A single platform for CDR data,

responsible lending, and full loan servicing.

Book a demo

Loan management software

built for the lending lifecycle

ACL-ready onboarding

Stand up a white-label application flow for personal credit, car finance, or BNPL customers.

Gather details a single time, connect the KYC and KYB tools you already trust, and flag risk on each file before it reaches an underwriter.

Gather details a single time, connect the KYC and KYB tools you already trust, and flag risk on each file before it reaches an underwriter.

Configurable origination

Check suitability against CDR data, Equifax, Experian, and illion within one decisioning pass.

Adjust rules, pricing, and document templates across asset finance, personal loans, or secured BNPL, then reuse that same flow whenever a new product goes live.

Adjust rules, pricing, and document templates across asset finance, personal loans, or secured BNPL, then reuse that same flow whenever a new product goes live.

Full-cycle servicing

Drive repayment schedules over BECS direct debit, NPP, and PayTo with a live ledger in view.

Handle hardship variations, payment pauses, and rate changes without spreadsheets, and log an audit-ready record at every borrower touchpoint.

Handle hardship variations, payment pauses, and rate changes without spreadsheets, and log an audit-ready record at every borrower touchpoint.

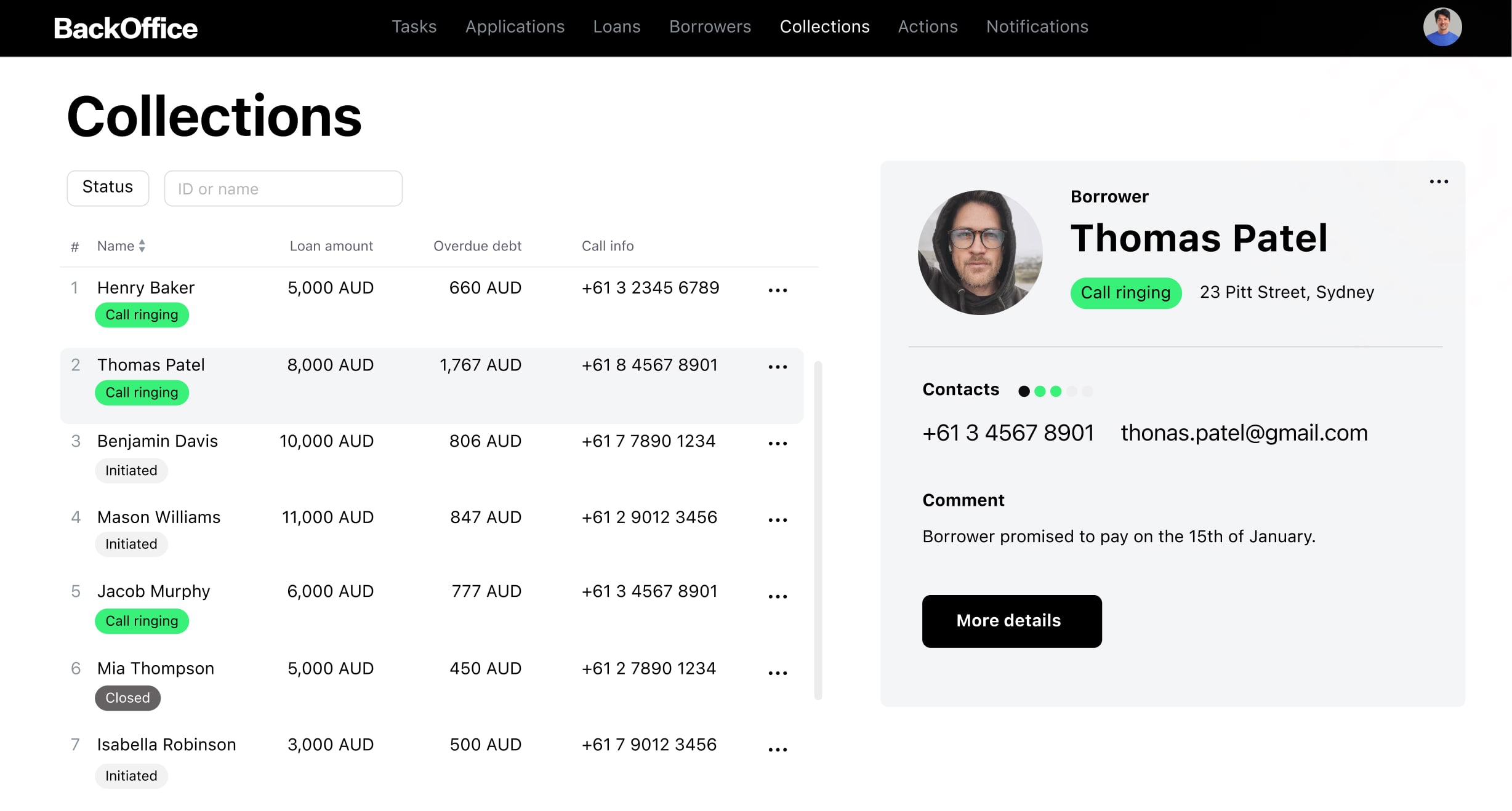

Compliant collection

Work arrears within NCC hardship rules using segmentation by delinquency bucket, outreach across

several channels, and AI models that match a recovery path to each borrower under financial

difficulty.

Get your lending

product estimate

in 3 minutes

STEP:

/

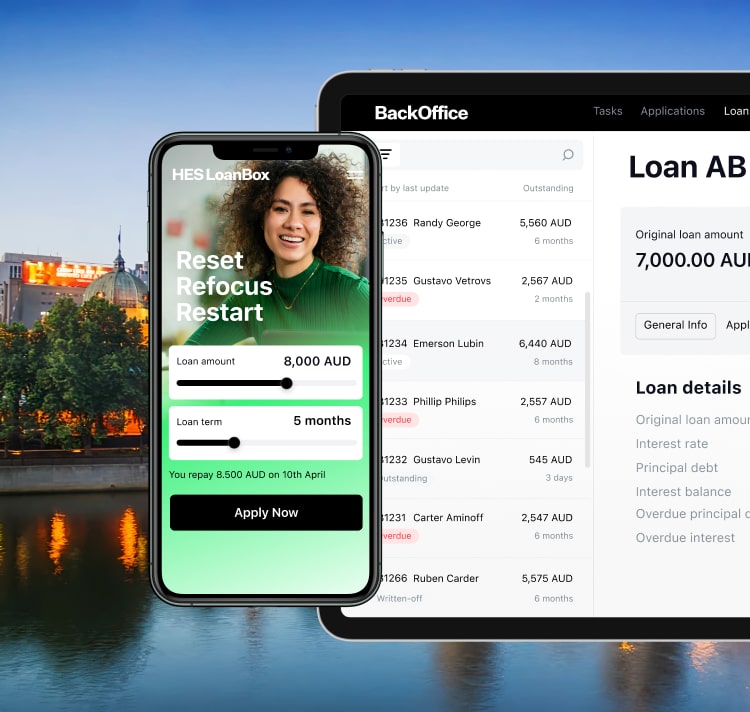

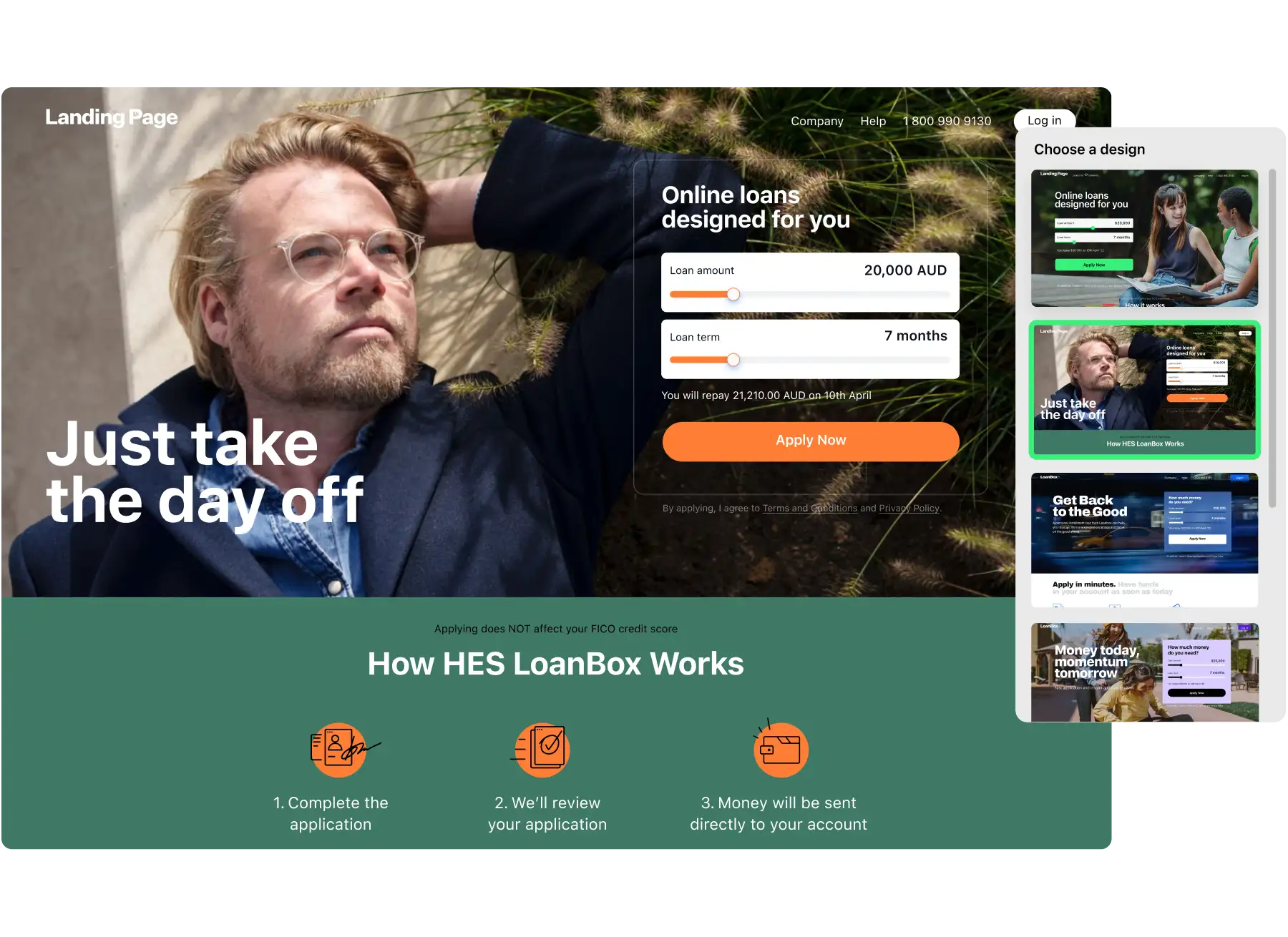

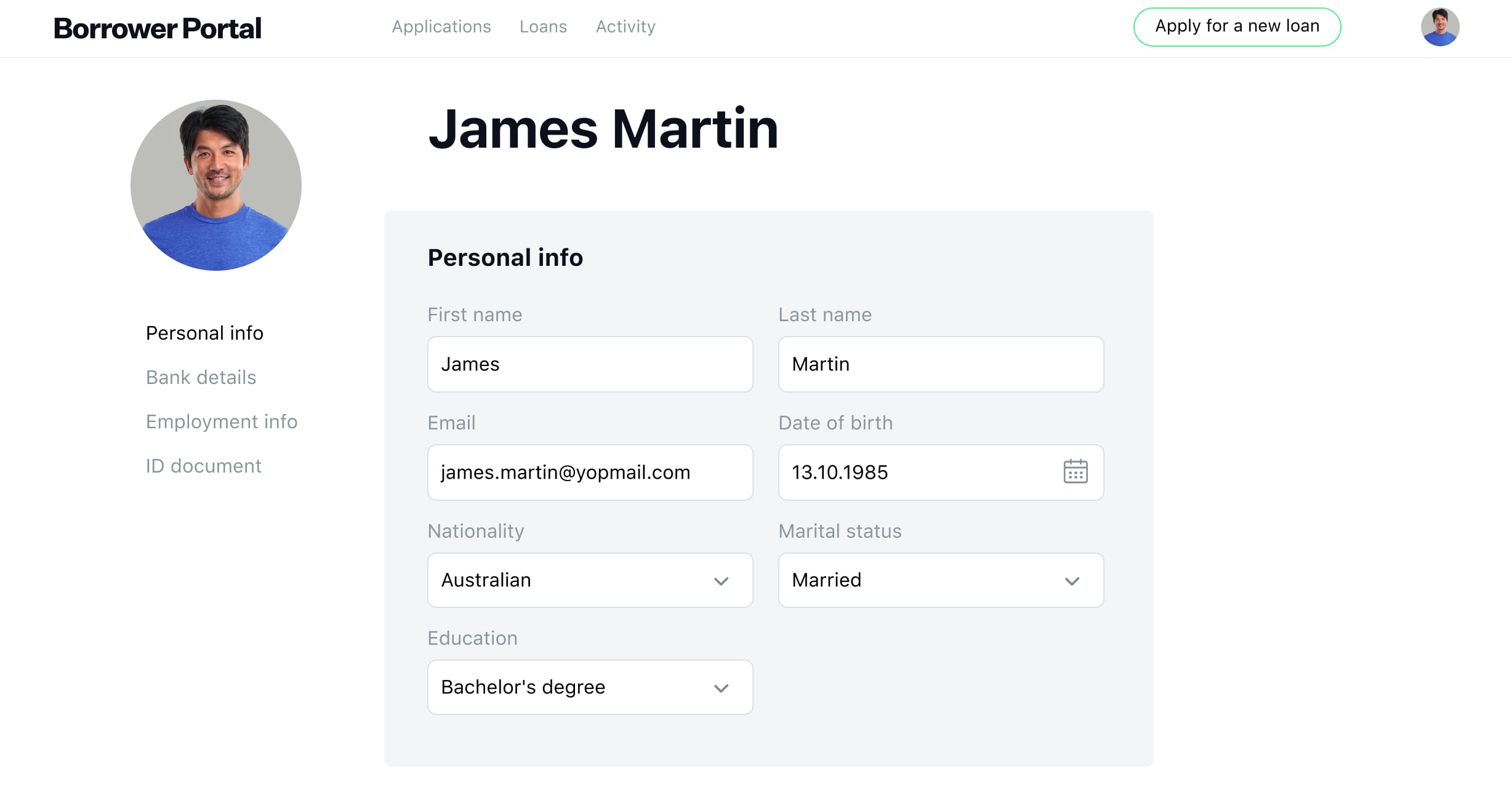

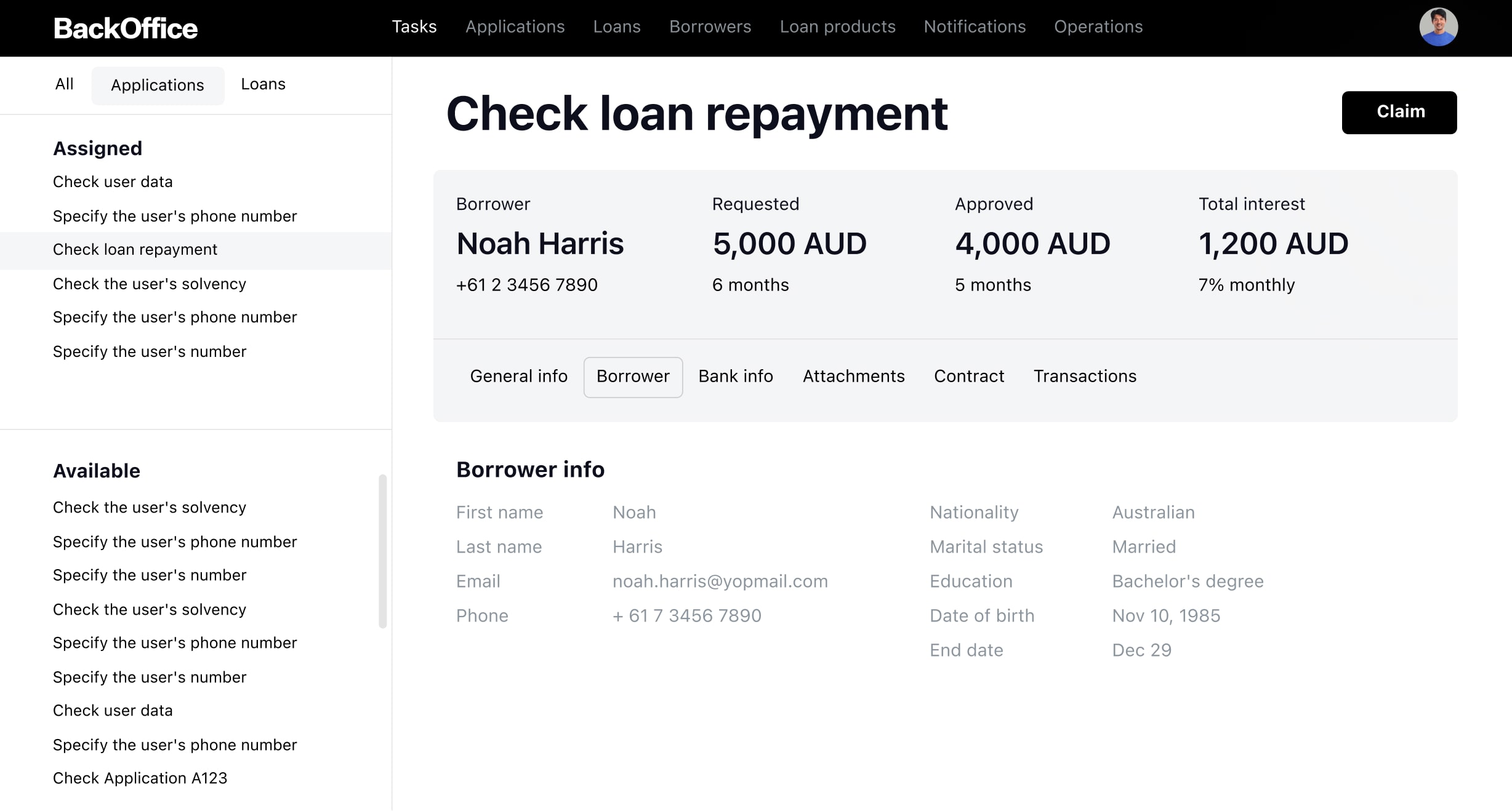

Digital onboarding

Digital onboarding shaped

for Australian lending rules

HES LoanBox AI-powered loan management system moves applicants from first tap to signed contract

without long forms or unclear pricing. Capture what underwriters need, log each step on an

audit-ready trail, and stop your team rekeying details between systems.

Show the full cost up front

Faster decisions without dropping checks

Keep borrowers close after payout

Grow through brokers and aggregators

Transform leads into loyal borrowers

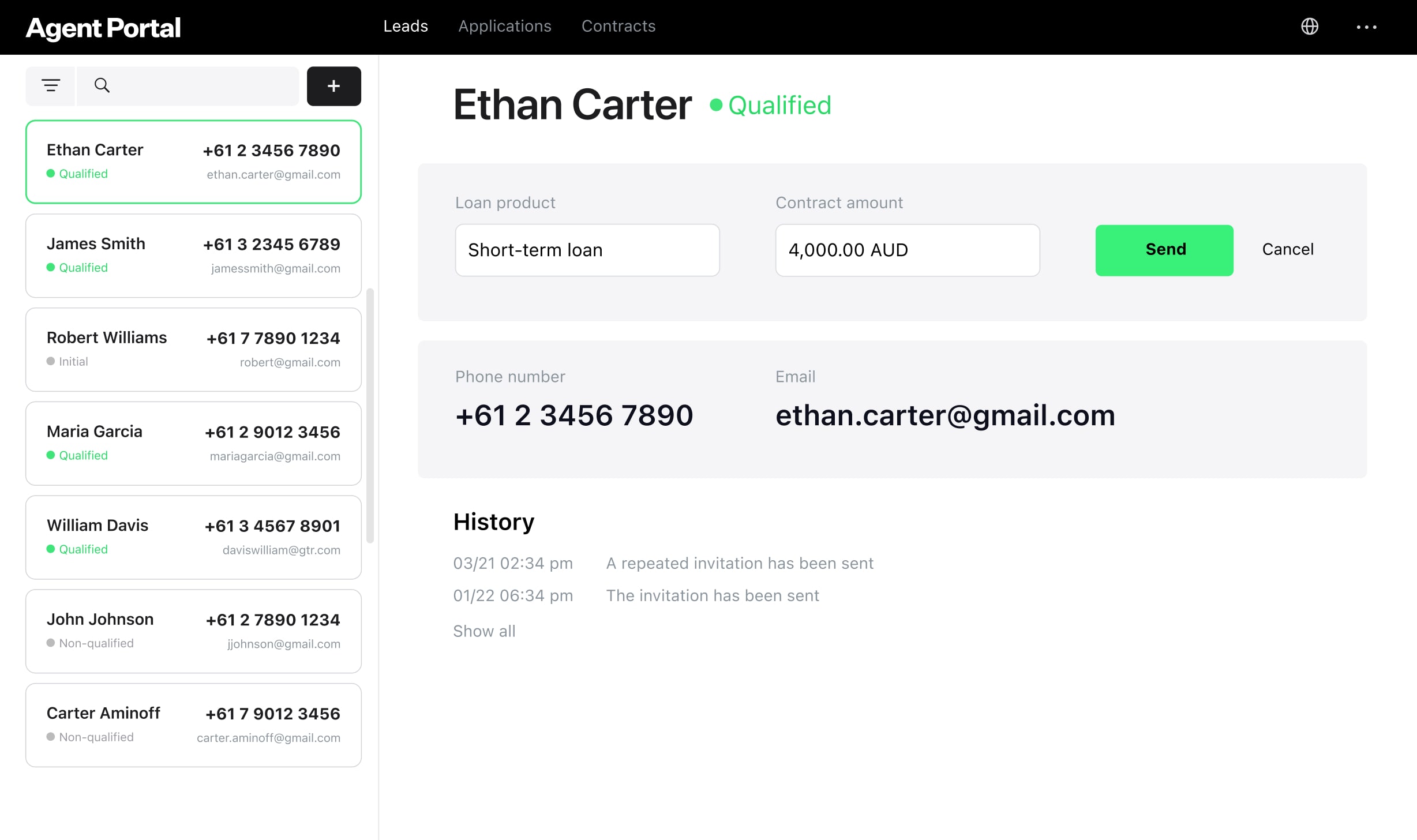

Landing Page

Agent Portal

Integrated plugin

Ensure 24/7 borrower access

Application flow

Borrower profile

Activity

Decision-making

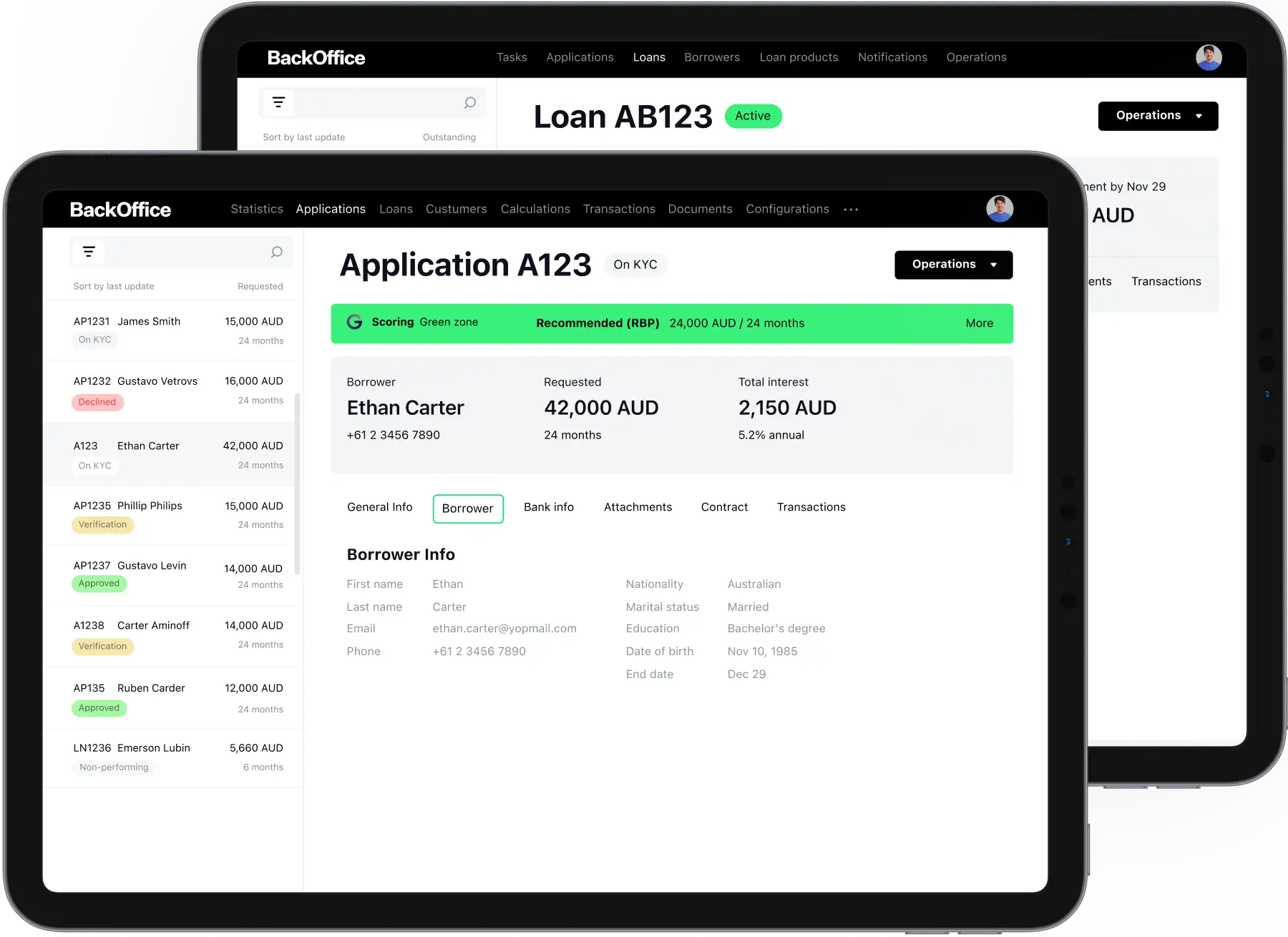

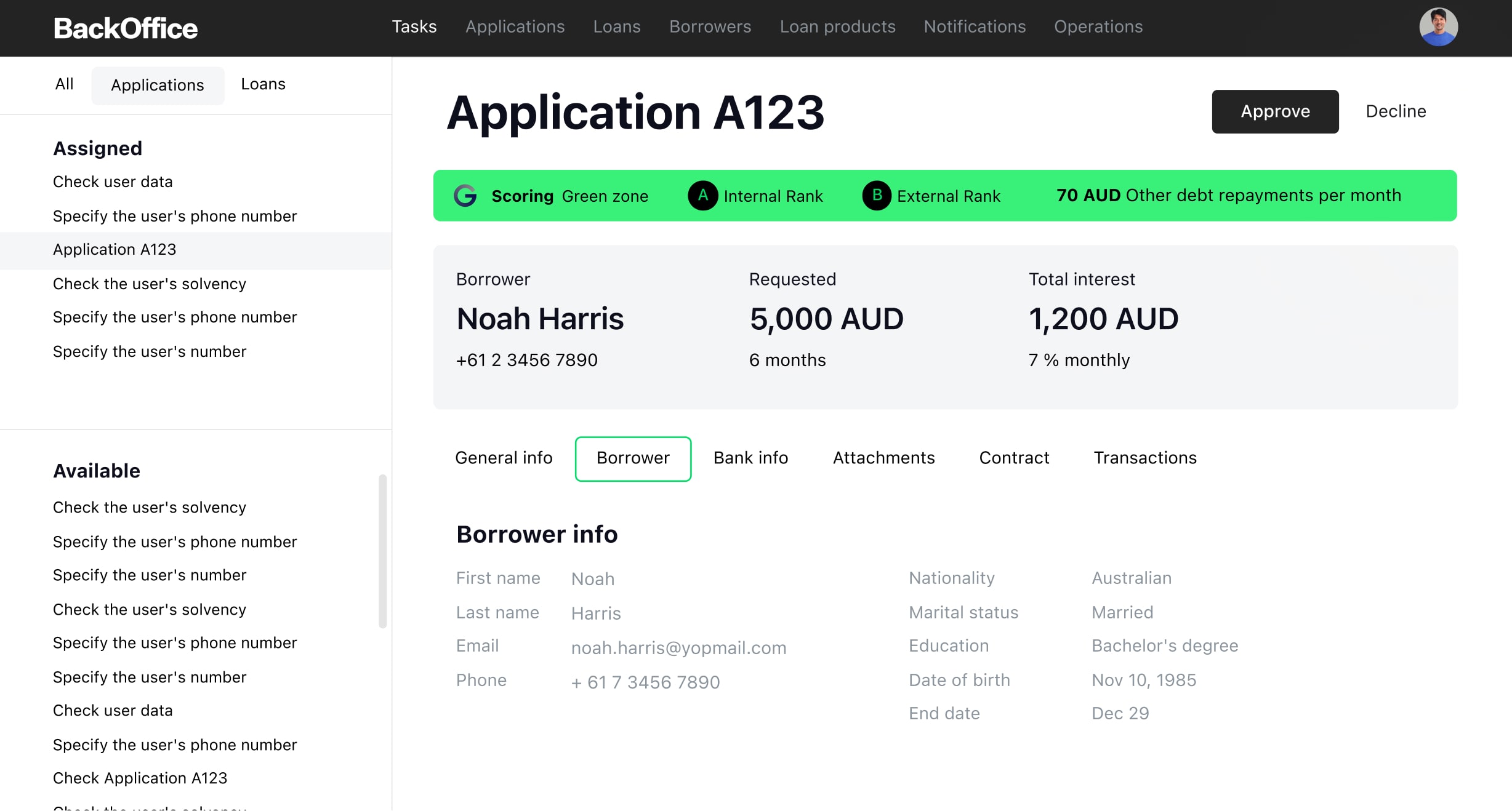

Loan origination

Faster loan origination

through AI and automation

Rekeying and month-old bureau files stretch Australian consumer credit decisions out by weeks. Live

CDR data, OCR for payslips and bank statements, and built-in e-signature make each application a

fast, defensible call, and trim up to 90% of document-handling cost.

Verify identity, build the borrower picture

Underwriting that follows your risk policy

Approve more of the good risk

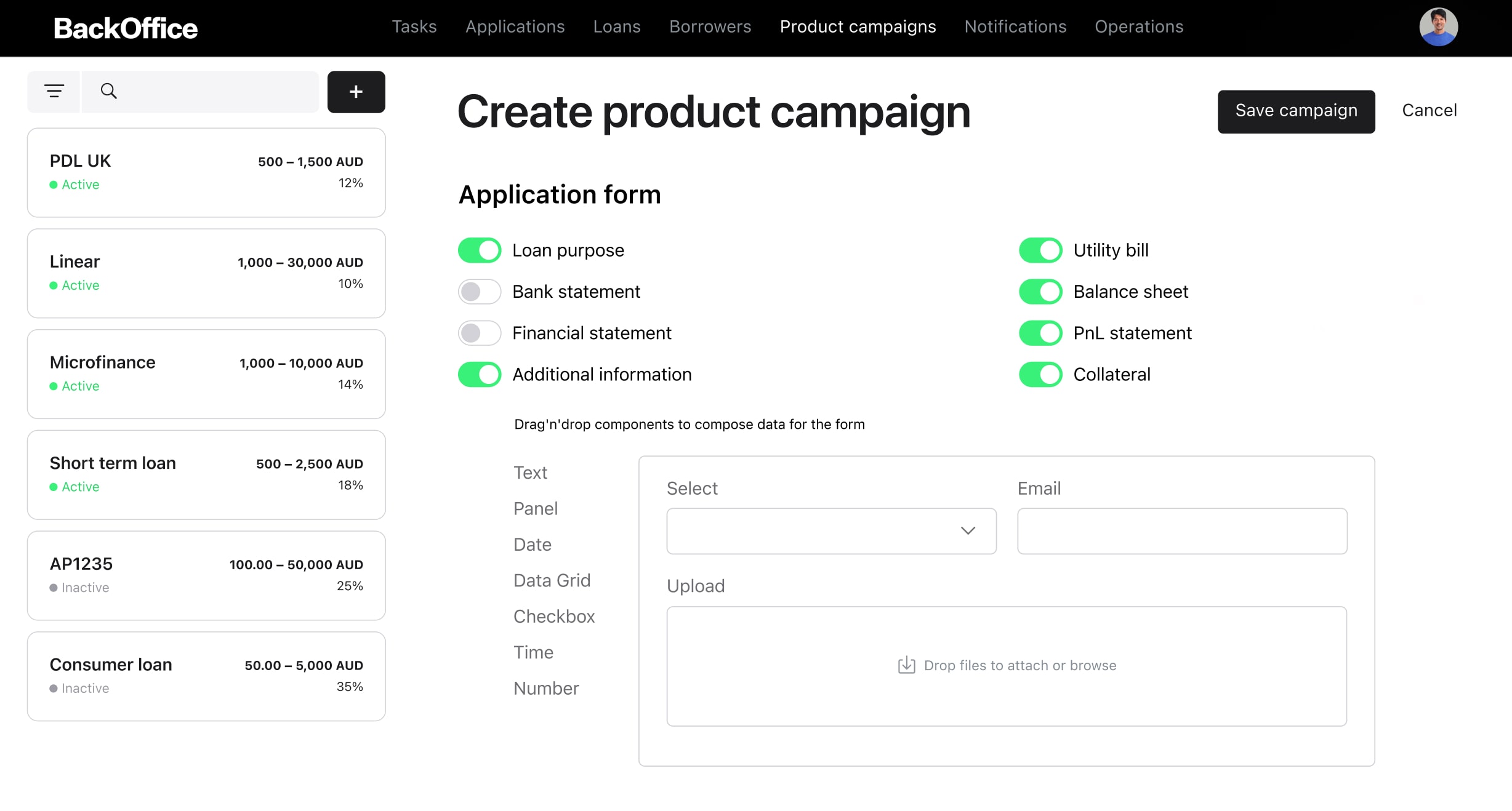

Unlimited product range

One core carries every product you offer, whether personal loans, car finance, or BNPL.

Define pricing, fees, schedules, and eligibility through configuration, not a developer

ticket.

Customizable application flow

Build lending journeys on a no-code canvas, without waiting on engineering to ship. Lay out

the approval gates and routing logic, then release a new product within days as obligations

shift.

Roles-based access

Keep borrower data behind role-based permissions, password rules, per-device controls, and

two-factor login. Each user action is written to an audit trail ready for ASIC and Privacy

Act review.

Compliant agreements in seconds

Assemble binding loan contracts from dynamic templates in moments. Pre-contract disclosures,

credit contracts, and repayment schedules build in one pass, worded to Australian consumer

credit expectations.

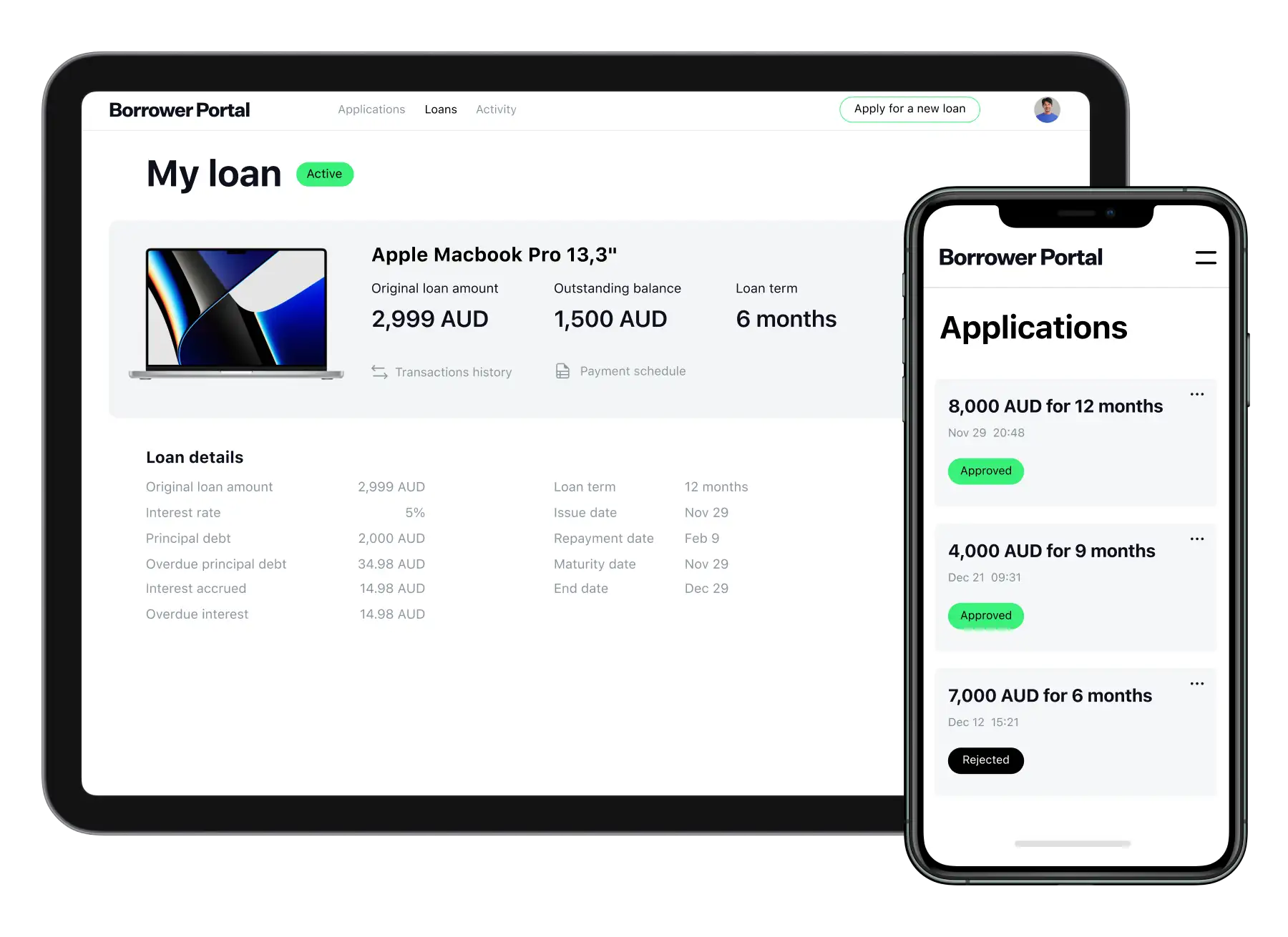

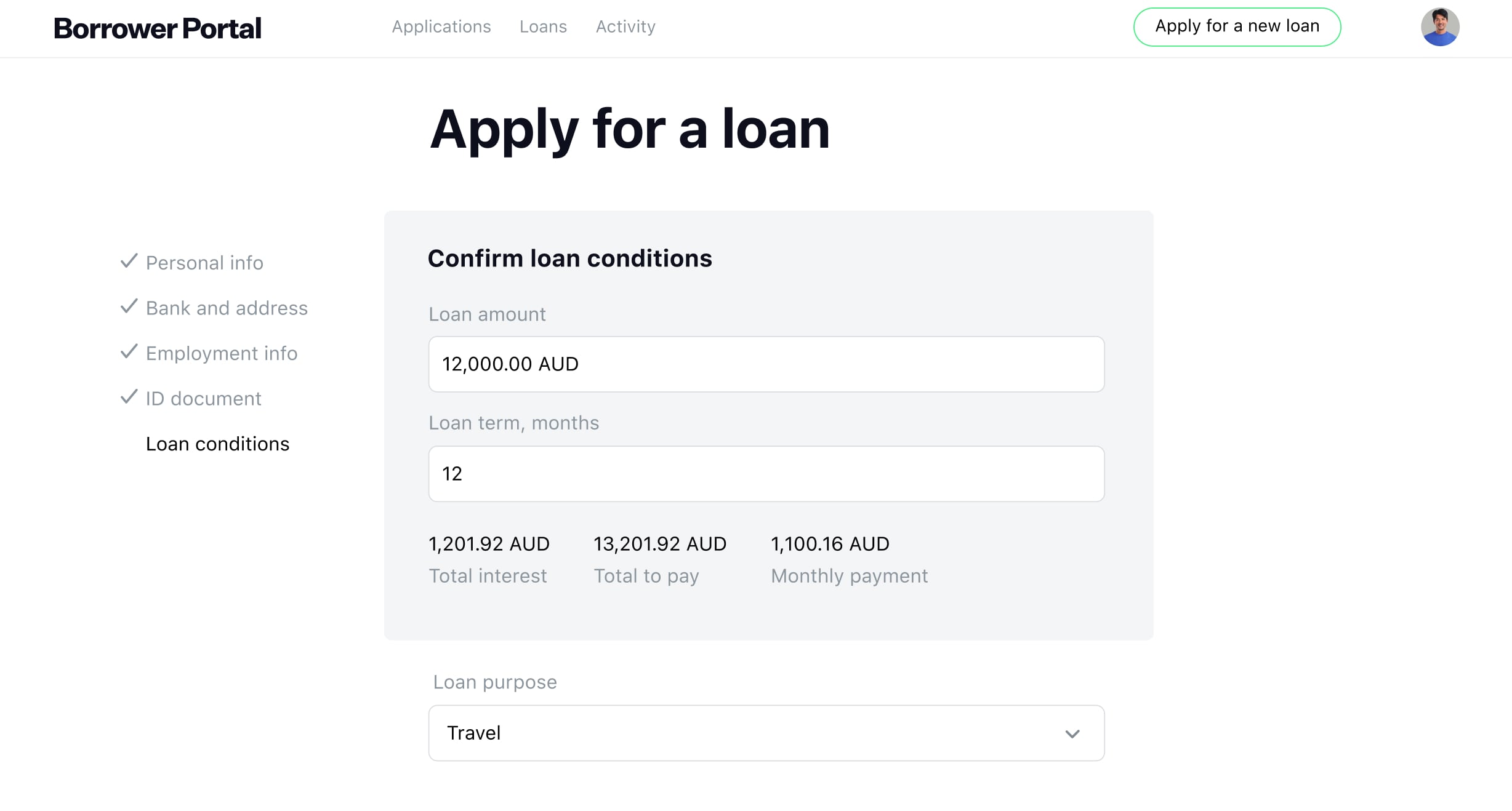

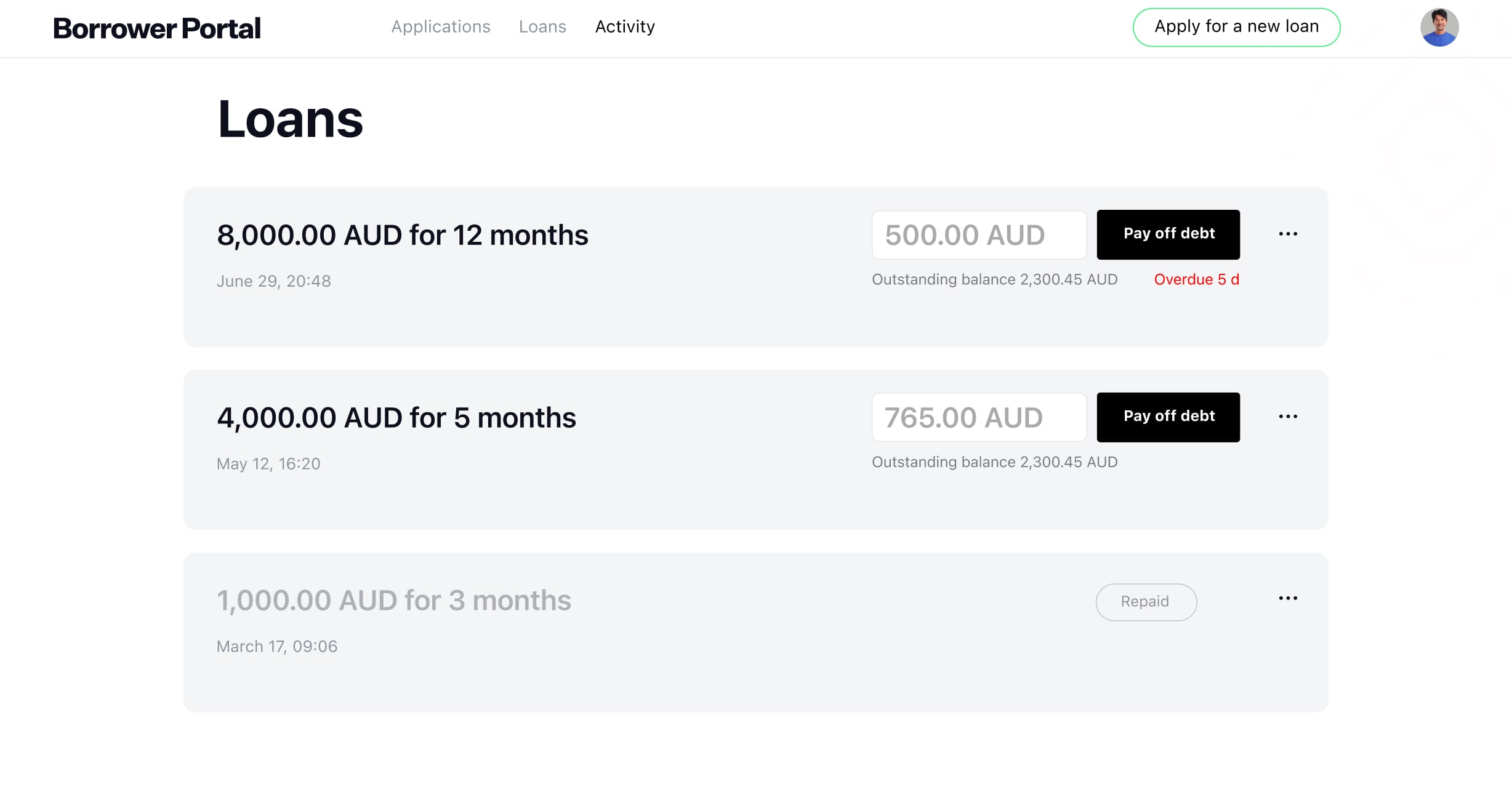

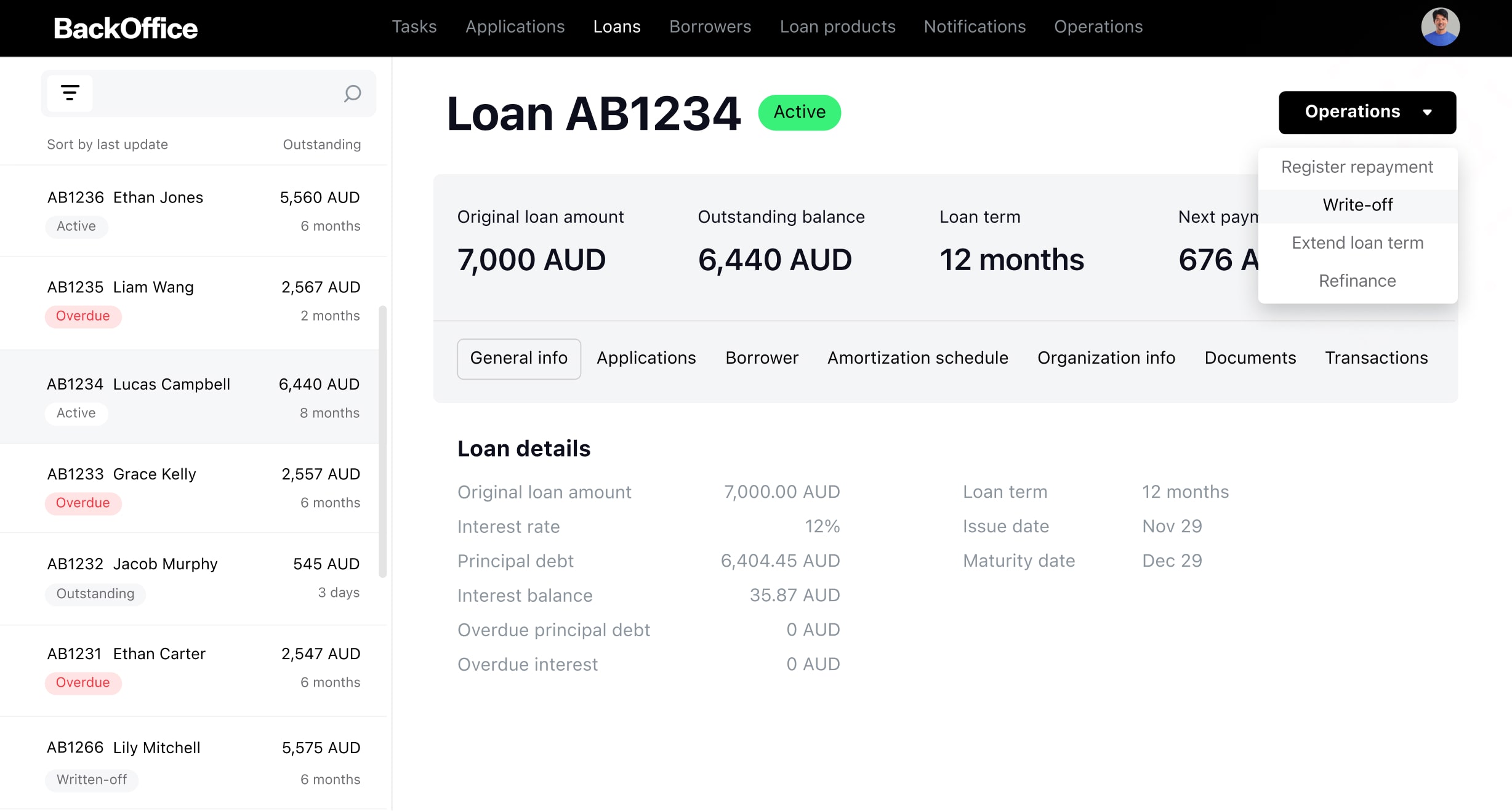

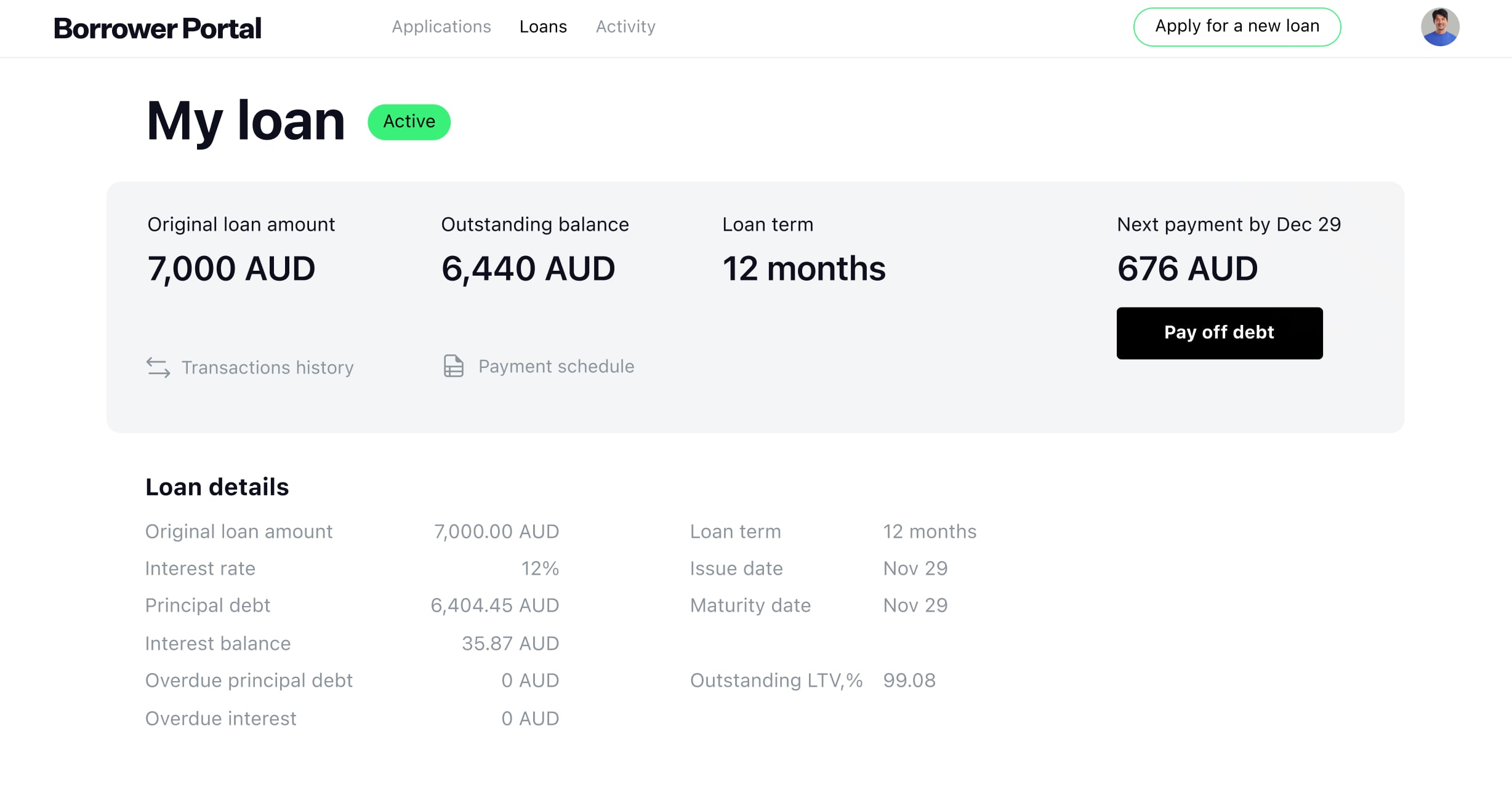

Loan servicing

Complete Australian loan management software

Servicing across Excel and a few half-linked legacy tools quietly drains margin and trust. HES

LoanBox carries the whole loan lifecycle on live data, terms you can configure, and integrated

payments, so servicing stays clean and audit-ready.

From drawdown to payoff, automatically

Adjust terms on the fly

Payments on Australian rails

Gain control of lending workflows

Deal management

Active loan

Debt collection

Product engine

Task management

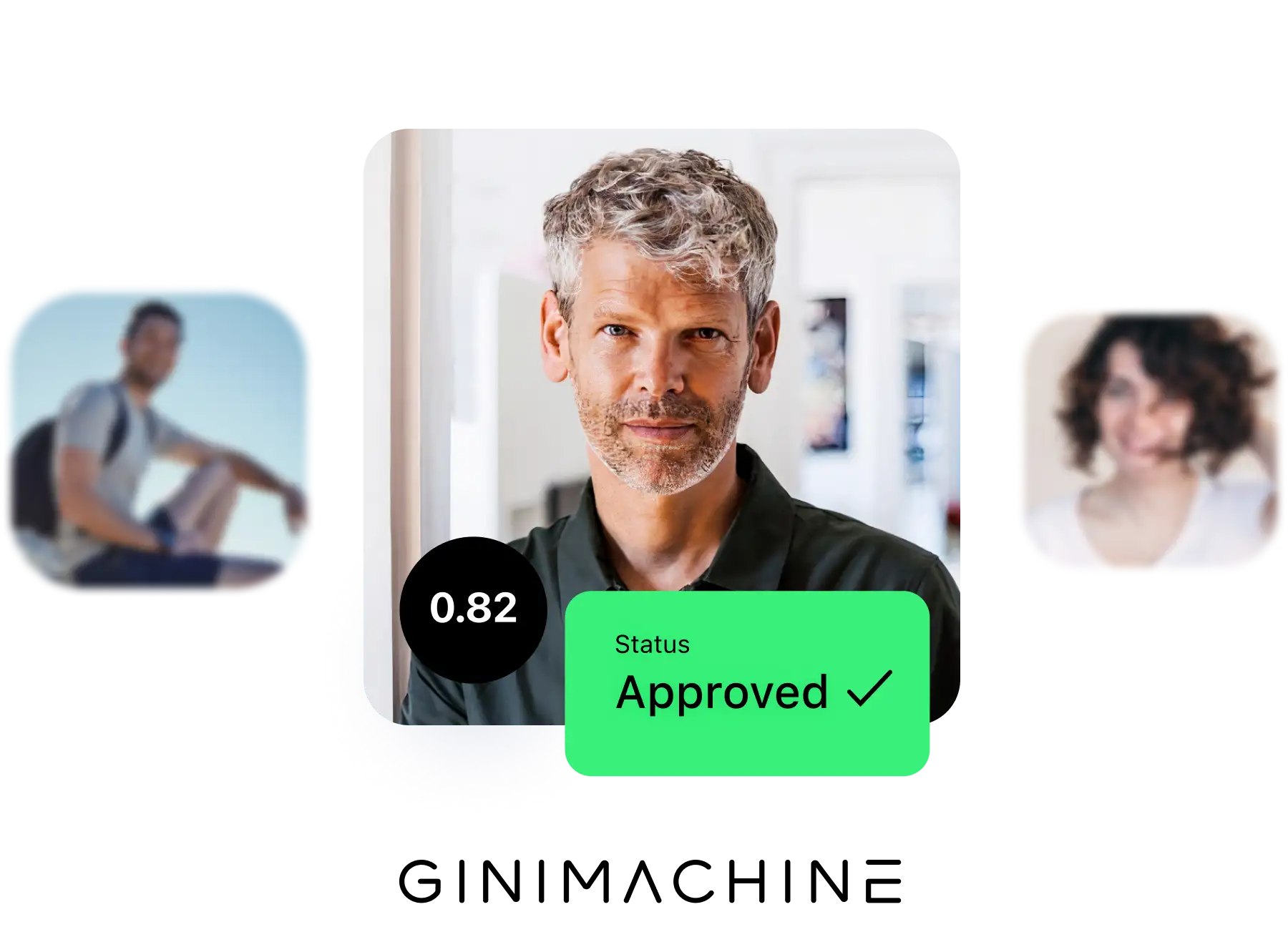

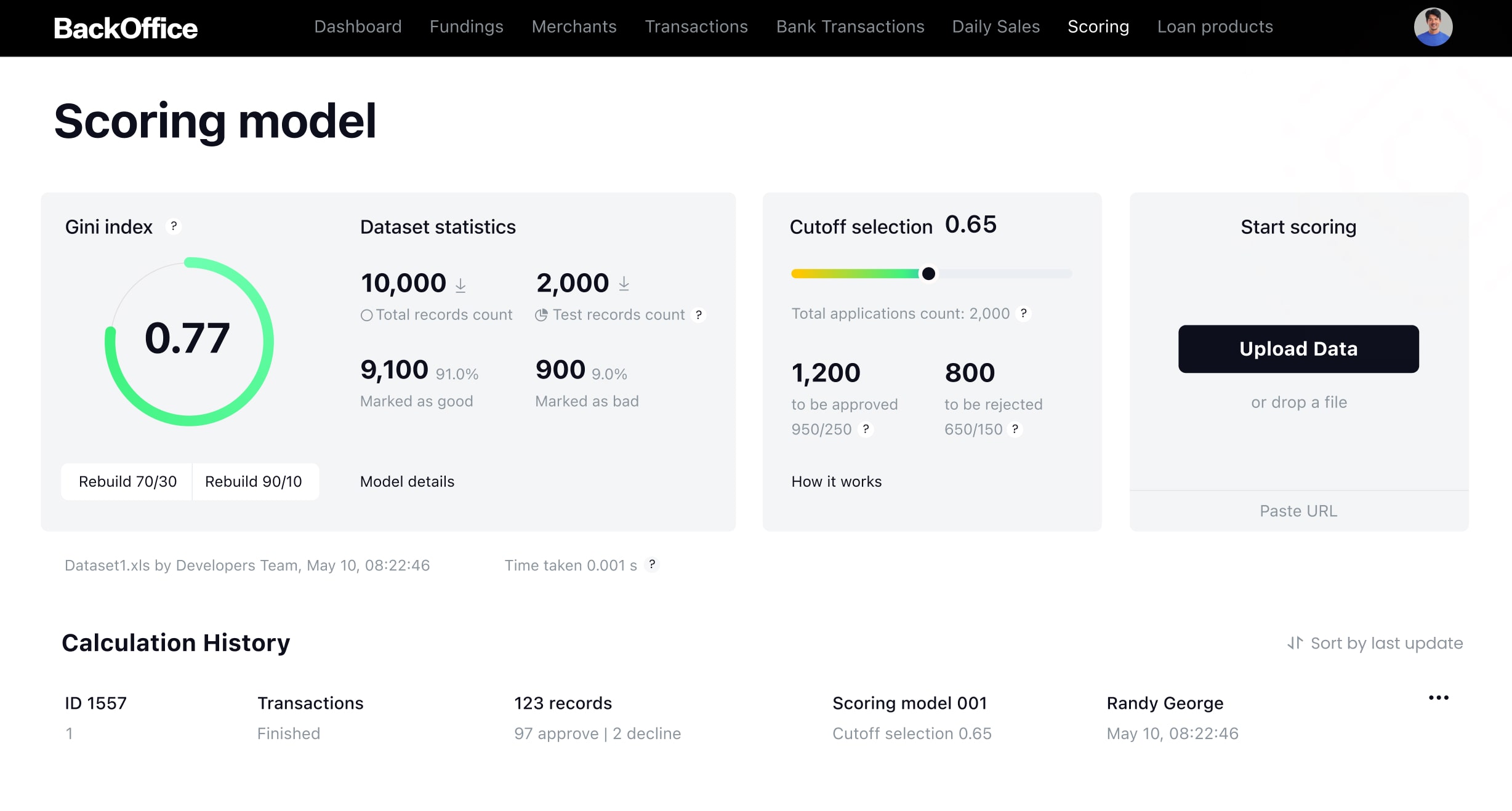

Scoring

Stronger loan portfolio performance

through AI risk intelligence

Explainable scoring for ASIC review

Run predictive scoring along the full Australian lending path, from first screen out to NPL

forecasting. Reason codes stay legible to your credit committee and an ASIC reviewer.

AI accuracy at scale

Trained on your own book, AI scoring raises accuracy up to 3× over bureau-only scores,

drawing on live transactions, not credit files from three months back.

Risk-based pricing controls

Tune thresholds per segment, catch affordability stress before it becomes arrears, then

re-price as refinancing pressure reshapes borrower cashflow.

Debt collection

AI-driven debt collection software

for Australia

In Australia, hardship duties and ASIC's focus on customers under pressure make collections a

compliance matter, not only recovery. HES LoanBox steers each account along workflows built around

affordability, hardship flags, and the rate and fee limits your licence sets.

Automate the full arrears workflow

AI-tuned strategy for each case

Fee and interest charges under licence limits

Lending reporting and analytics

HES LoanBox turns the lending metrics your CFO and credit committee watch into live dashboards. Pull

raw data for regulatory reporting, define custom metrics, and split the book by vintage, channel, or

product.

100+ Australian and global integrations

for your lending stack

HES LoanBox ties into the tools your team already runs, with ready-made links to Equifax, Experian,

illion, Basiq, Frollo, BECS, and NPP, plus the core-banking, accounting, and KYC systems beside

them.

Why Australian lenders

pick HES LoanBox

Unlimited customisation

Adjust modules, rework the borrower flow, and link any Australian service from CDR to

payment rails, then own the code with no lock-in.

Transparent pricing

Licence is what you pay for; custom build is the only add-on. Borrowers, brokers, and

internal users are all unlimited, with no per-seat charge as the book grows.

3-month launch for Australian lenders

Go live on a standard setup in roughly 3 months. Start lending sooner, reach ROI faster, and

keep tuning the platform as you scale.

Australian lending expertise

Lean on a team of analysts and engineers with over a decade building and running lending

products for banks, mutual banks, fintechs, and non-bank specialist lenders.

Bank-grade security

ISO 27001 certified, SOC 2 aligned. Run on AWS, Google Cloud, on-premises, or hybrid, on a

secure Java LTS stack with regular updates.

Dedicated support

Get quick help from a support team fluent in Australian lending and working in your

timezone.

HES FinTech has been our reliable technology partner since 2012. I believe much of our success is due to the well-architected HES LoanBox solution.

HES FinTech offers comprehensive front-to-back solutions with integrations. Our machine learning platform will allow clients best-in-class investment advice.

In just 6 months, we went from storing all our data in Excel to a fast, reliable, and user-friendly platform that caters to our specific needs.

HES FinTech developed our lending software and predictive analytics. Their expertise delivered automation, clear UI/UX and customer portal.

The LMS provided flexible repayment options, automated restructuring and branch-level management, enhancing efficiency and risk mitigation.

Security

Deployment

Tech stack

ISO 27001 security

ISO 27001 certification, SOC 2 alignment, and SDLC keep security tight

across every operation, with full data encryption, role-based access, audit

trails ready for ASIC review, and a hardened hosting setup.

Learn more

Cloud, on-premises,

or hybrid

HES LoanBox deploys on AWS, Google Cloud, on-premises, or in a hybrid setup,

matching your IT estate and your board's data preferences.

Open-source

backend stack

HES LoanBox runs on free and open-source foundations like Java LTS, BPMN

2.0, Camunda, and Form.io modeler. The stack keeps licensing fees off the

table apart from the platform source code, so Australian teams know what

they own.

The 2026 reality of

Australian lending

A$2.18B

lost to scams in 2025

Australians reported

A$2.18 billion

in scam losses across 2025, led by investment and payment-redirection fraud. Layered

identity, CDR, and device checks catch more of it before payout.

100,745

complaints to AFCA in 2024-25

AFCA logged

100,745 complaints

in 2024-25, and banking and finance made up 54% of them. Clean audit trails and quick

hardship handling keep disputes from escalating.

Jun 2025

BNPL under the Credit Act

From

10 June 2025, BNPL providers need an Australian Credit Licence and suitability checks. Only automated

affordability decisioning can clear those checks at the point of sale.

7.4%

annual growth in Australian credit

Total credit grew

7.4%

in the year to November 2025, with business lending at its fastest pace since 2008. Volumes

climb faster than headcount, pushing lenders to drive down the cost of each decision.

Start Australian lending

in 3 months

You grow the Australian book; HES LoanBox runs everything behind it.