The selection process works better when it starts with constraints rather than features.

Before evaluating platforms, define three things: which loan products you need to originate,

which regulatory requirements apply to your markets, and what your current technology stack

looks like — because the cost and complexity of integration often determines the realistic

shortlist more than any feature comparison does.

From there, four questions tend to separate platforms that will actually work for your

operation from those that look good in a demo. First, can the platform configure your credit

policy — your specific rules, stop factors, and product terms — without custom development,

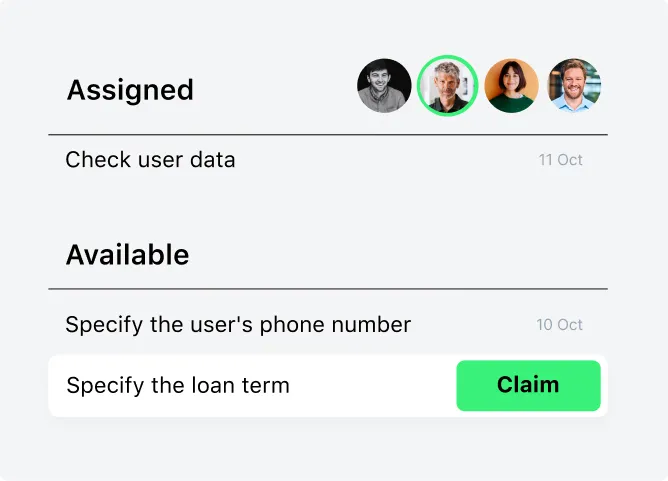

or does every change require vendor involvement? Second, how does the system handle

exceptions, which are inevitable in any real lending operation? Third, what does the

vendor's implementation track record look like for institutions at your scale, not their

largest or most prominent client? And fourth, what does data portability look like if you

decide to switch — because a platform that makes exit difficult is also a platform that has

less incentive to keep improving after you sign.

For a ranked list of the best loan origination software solutions in 2026 and a practical

framework for evaluating which platform fits your business model, see our

loan origination software rating.