Mortgage lending software for

modern originators

One platform for banks, credit unions, and independent mortgage banks, covering purchase,

refinance, home equity, HELOCs, jumbo, and construction lending end to end.

Book a demo

One platform across the full

mortgage lending lifecycle

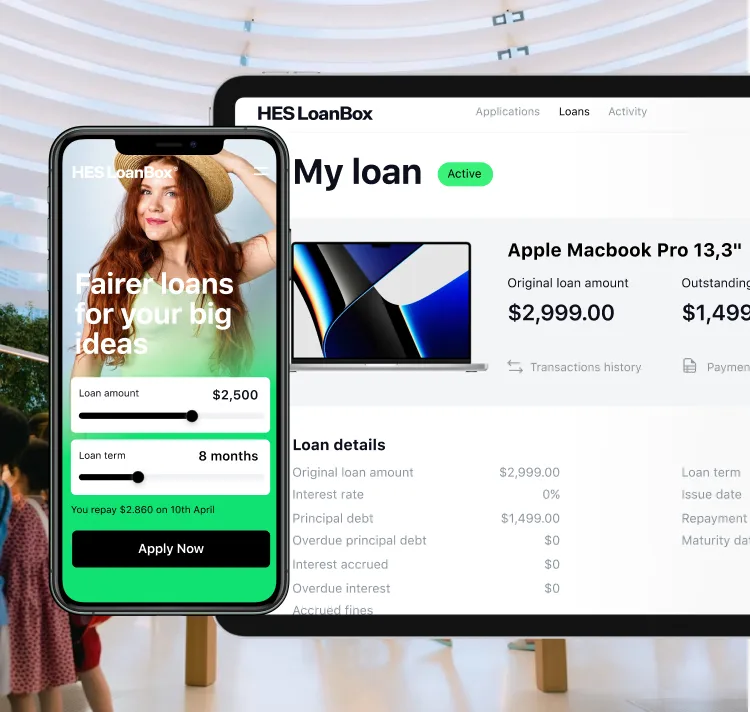

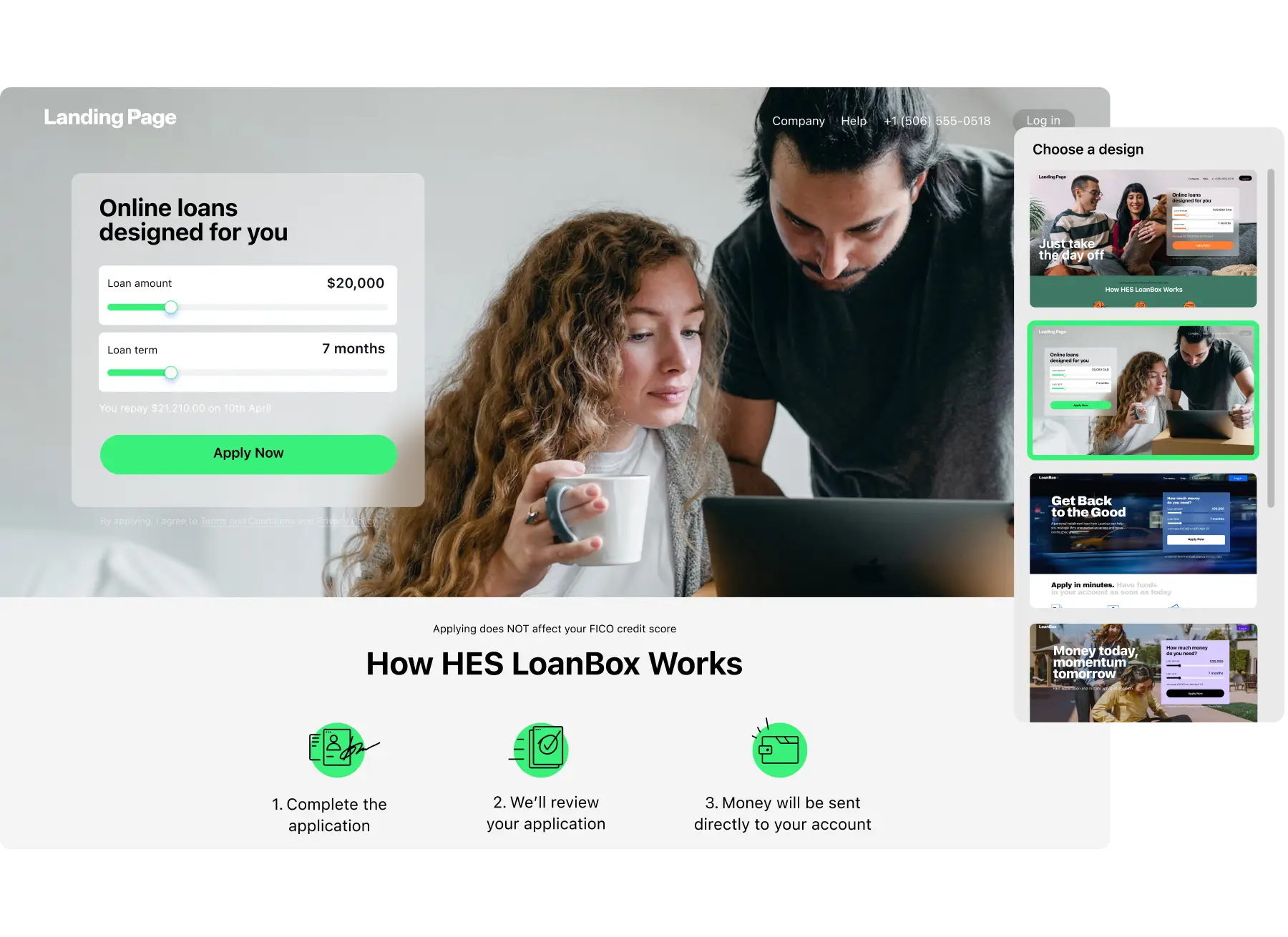

Digital application intake

The borrower meets a white-label portal that opens on any screen. From the first

application through the eligibility check to the final uploaded document, intake runs in

one unbroken sitting, and the identity and document checks happen out of sight.

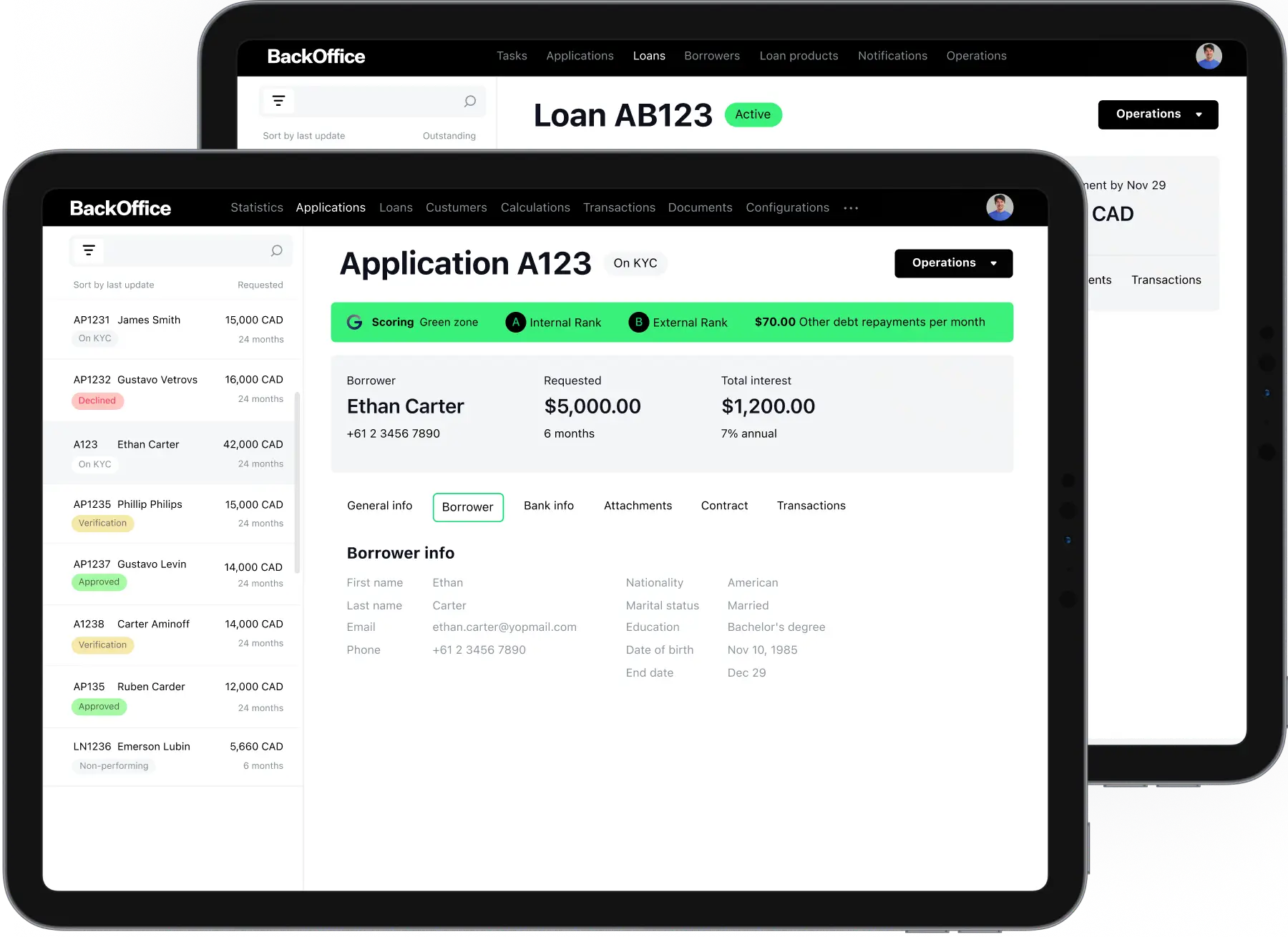

Underwriting and decisioning

Decisions land sooner once underwriting workflows are yours to shape, scoring leans on

AI, and bureau, income, and asset feeds arrive on their own. Purchase, refinance, and

home equity each carry their own eligibility rules, pricing logic, and risk frameworks,

matched to the way you lend.

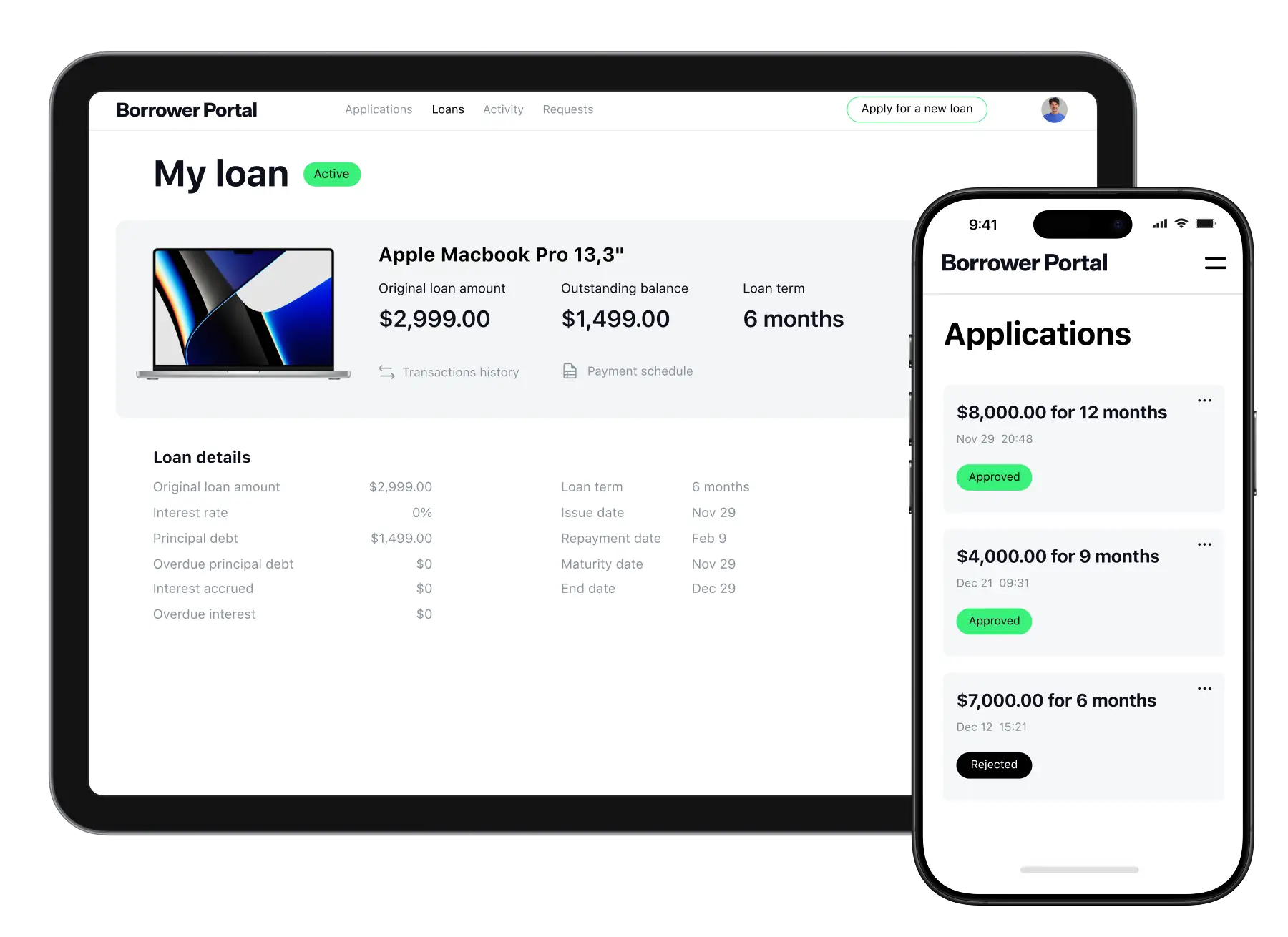

Servicing and escrow

Amortization, escrow, payoffs, and borrower messaging share one workspace instead of

four. Live portfolio visibility holds the servicing desk and homeowners on the same

page, from the first payment through final payoff.

Default and loss mitigation

Predictive analytics flag a delinquent mortgage early, and AI-guided outreach opens the

right loss mitigation path, a repayment plan, forbearance, or modification, fitted to

each homeowner rather than a script.

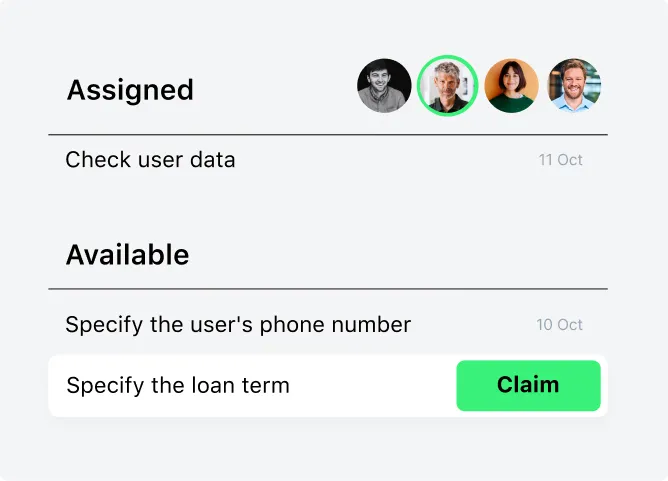

Keep mortgage files moving with smart task management

Nothing in the pipeline waits on a manual handoff. Files route themselves by role and

current workload, turn times and SLAs stay on screen as they tick, and processing,

underwriting, and closing all read from one live view of each loan.

Price your mortgage

product in just

3 minutes

STEP:

/

Online onboarding

Mortgage lending software that

takes applications to a yes

Rate shoppers turn into closed loans when nothing in the path snags. Borrowers move through

a fully digital mortgage; the team behind them leans on automation to push far more files on

a fraction of the manual load.

Hook applicants from the first click

Faster approvals, no shortcuts

Open broker and correspondent channels

Loan origination

Cut mortgage

origination time

with AI and

automation

A closing slips the moment reviews drag and conditions slip through, and the borrower signs

with whoever is faster. Put verification and automated underwriting together, and every

mortgage application turns into a quick, well-papered decision that holds up.

A full borrower picture in minutes

Underwriting that flexes per file

AI decisions that widen the funnel

GiniMachine scoring that keeps learning

A paper-free path to closing

and much more

Any mortgage product, configured

Fixed and adjustable rate loans, jumbo, home equity, HELOCs, construction financing,

whatever your market asks for, ship from the same builder. Rates, fees,

amortization, and eligibility rules bend per product or borrower segment, and none

of it waits on a developer.

Documents and disclosures on demand

Loan documents and disclosures roll off dynamic templates with merge fields in

seconds. Fewer drafting slips, an earlier closing, and paperwork that tracks the

regulatory expectations of each state on your map.

Notifications that adapt

Dynamic fields drive personalized SMS, email, and push templates that span every

borrower touchpoint, application status, conditional approval updates, payment

reminders, and escrow notices alike.

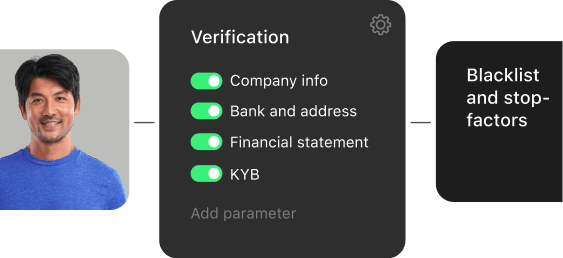

Granular access control

Borrower data stays guarded by fine-grained role permissions, configurable password

policies, and two-factor sign-in. Every action your team takes is logged in full, so

the file is ready whenever an auditor asks.

Outreach on every channel

Rule-based triggers tied to file status and borrower activity fire outreach across

SMS, email, and in-app channels. Homeowners stay in the loop at each stage, and the

routine load lifts off your servicing and support teams.

Workflows without code

Mortgage workflows take shape visually, no engineering hours spent. Lay out

application flows, wire approval logic, branch conditional decision trees, and put a

new process live in days instead of quarters.

Configurable mortgage lending workflows

Mortgage loan servicing

Mortgage loan servicing software that runs the whole book

Margins bleed when a servicing team hops between systems and reconciles by hand. Once the

whole book lives on one platform, the daily grind turns fast and clean: live data,

configurable terms, escrow, and payments all run in the same place.

From funding to payoff, automated

One workspace, every product

A complete view of each homeowner

Payments and reconciliation, handled

Stronger mortgage portfolio performance

through AI risk insight

Clear, explainable scoring

Carry predictive scoring through the whole mortgage journey, from filtering

applications on day one to forecasting defaults later, and keep every output

transparent, explainable, and ready for review.

Sharper credit precision

Tighten mortgage credit decisions with built-in AI that reaches up to 3x the

accuracy of conventional scoring.

Risk controls you set

Dial in your own risk thresholds, catch likely defaults ahead of time, and reprice

as needed so the mortgage book stays profitable across any rate cycle.

Mortgage loan collections

Recover more on delinquent mortgages

with automated collections

Working recovery by hand runs slow, costs too much, and strains the borrower tie. Let AI

carry outreach, scoring, and fee handling, forecasting who repays, choosing the channel that

connects, and holding every delinquent mortgage file audit-ready.

Run recovery from one queue

Move borrowers into the right workout

Head off missed payments

Fees and penalties, kept in line

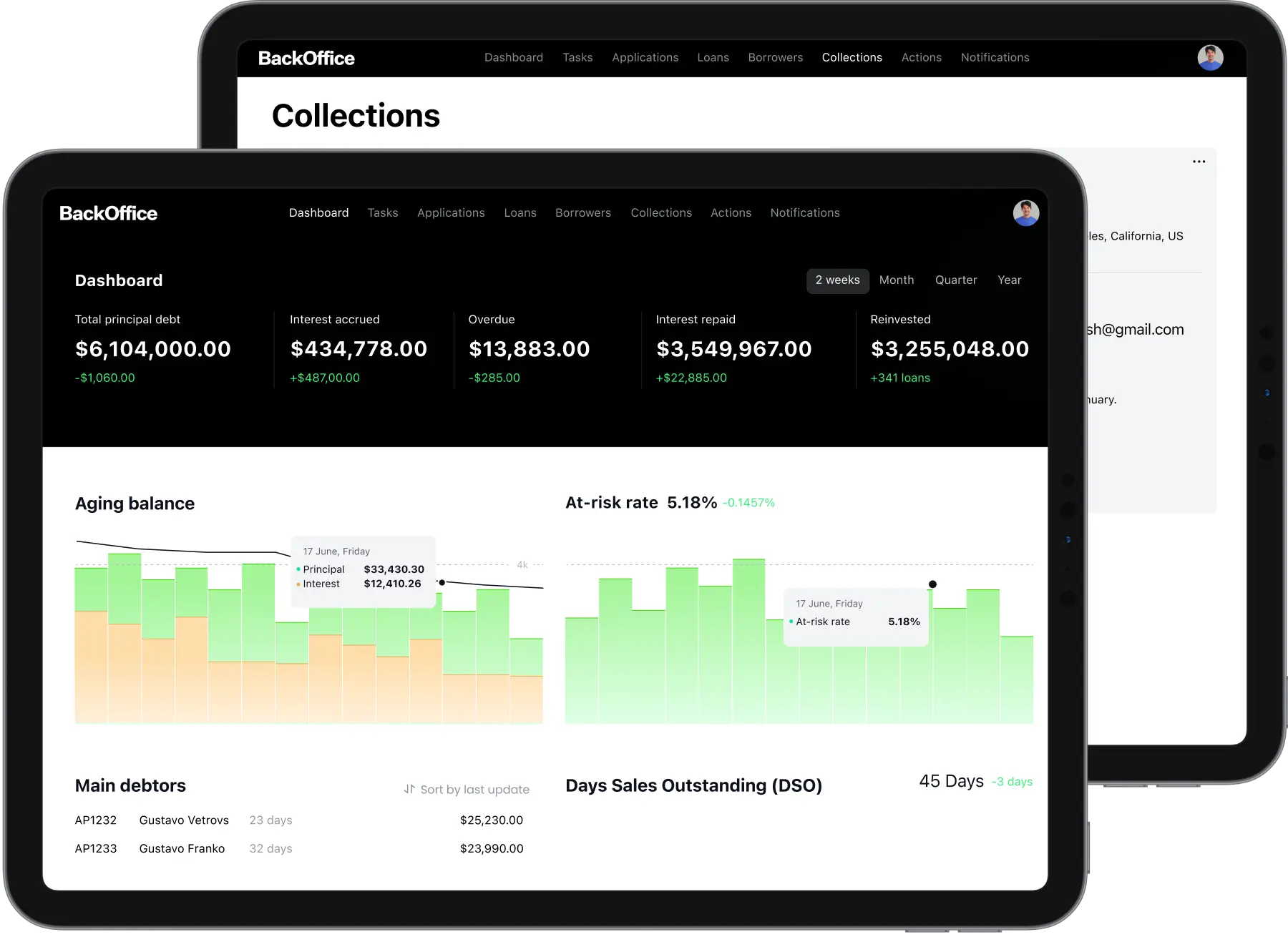

Reporting and analytics for your mortgage book

Interactive dashboards in HES LoanBox center on the mortgage KPIs your team watches,

pull-through, cycle time, delinquency, escrow. Pull the raw data, define your own metrics,

and cut the portfolio whichever way the business needs.

Connect your mortgage stack

with 100+ integrations

Flexible connection options and full customization give HES LoanBox a wide reach, linking

mortgage operations across onboarding, scoring, payments, communication, analytics, and core

banking.

Why lenders pick

our mortgage lending software

Bend it to fit

Mold it to your shop, reworking modules, adding features, reshaping screens, and

hooking up whatever services you run, payment rails through credit bureaus.

Pricing you can read

HES keeps the bill plain, one license fee, with custom work billed only on request.

Internal users and borrowers are never metered.

Live in three months

Go live in as little as 3 months on a ready-to-deploy mortgage platform, so both

lending and ROI arrive sooner.

Lending expertise

Our business analysts bring 14+ years in lending spanning the US, EU, and emerging

markets. Built by lenders, for lenders.

Security that stands

ISO 27001 and SOC 2 certified, running on AWS or Google Cloud over a secure Java LTS

stack kept current with regular updates.

Support that sticks

A dedicated support team sits one message away for fast, expert help.

HES FinTech has been our reliable technology partner since 2012. I believe much of our success is due to the well-architected HES LoanBox solution.

HES FinTech offers comprehensive front-to-back solutions with integrations. Our machine learning platform will allow clients best-in-class investment advice.

In just 6 months, we went from storing all our data in Excel to a fast, reliable, and user-friendly platform that caters to our specific needs.

HES FinTech developed our lending software and predictive analytics. Their expertise delivered automation, clear UI/UX and customer portal.

The LMS provided flexible repayment options, automated restructuring and branch-level management, enhancing efficiency and risk mitigation.

The 2026 reality of

mortgage lending

$11,094

to produce a single loan

Producing one mortgage cost lenders an average of

$11,094

in 2025, close to a record high (MBA, 2025). With pull-through slipping and wages

climbing, automation is the realistic way back to healthy per-loan economics.

1.87%

single-family mortgage delinquency

The delinquency rate on single-family residential mortgages climbed to

1.87% by the end of 2025

(Federal Reserve, 2025). As defaults edge up, servicing and loss mitigation can no

longer ride on spreadsheets and manual reconciliation.

1 in 118

applications carry fraud risk

An estimated

1 in 118 mortgage applications

carried fraud risk in late 2025, with far higher rates on investment and multi-unit

loans (Cotality, 2026). Identity and income verification cannot stay a manual step.

$2.2T

2026 origination forecast

Single-family origination volume is projected to rise about 8% to

$2.2 trillion in 2026, much of it arriving in sudden refinance waves (MBA, 2025). Adding capacity

without adding headcount is the whole contest.

Security

Deployment

Tech stack

Enterprise-grade

security

ISO 27001 and SOC 2 certification, paired with a secure SDLC, hold

protection steady across operations, with full data encryption,

role-based access control, and hardened hosting underneath.

Learn more

Built on cloud

technologies

Run HES FinTech mortgage software on-premises or in the cloud of

whichever provider you prefer.

Open-source

backend stack

The build rests on free, open-source tooling, Java LTS, BPMN 2.0,

Camunda, and the Form.io modeler, so extra licensing fees never

enter the picture and cost stays limited to the platform's source

code.

Start lending

in just 3 months

You drive the growth; HES FinTech runs the platform behind it.