Digital factoring is the way many corporate lenders go when expanding their market offerings. And it creates a win-win situation for all parties involved: businesses benefit from improved turnover and higher productivity, while lenders get their piece of cake due to this sophisticated yet very old financing tool.

Factoring appeared long before the first venture capital deals or equity investments and today it reveals new opportunities as it moved online.

Read also

For now, it is becoming more and more difficult for SMEs to secure funding with the help of loans. In times of economic instability, credit institutions are more cautious when granting loans and try to minimize the risk of default payments. As a result, businesses suffer from strict lending requirements. All that creates a fertile ground for the flourishing of factoring, and fintechs use this trend by providing it solely or combining factoring with other services.

Even though the FCI Global Factoring Statistical Report demonstrates a slight 4-percent decline in international factoring volume, everybody knows the reasons for that. Thus, the 2021-2024 predictions look significantly more optimistic and allow a lot of banks and financial companies to consider investing in factoring software development. This allows to increase the volume of factoring contracts processed and provides a lot of other advantages.

In this article, we are going to cover the key points of factoring automation for lenders, provide technical insights on factoring platform development and share our 10-year expertise.

Looking for unique factoring software?

Digital Factoring in Banks and Financial Institutions

The two tasks to be solved by a vendor in factoring software development are increasing the speed and decreasing costs.

Most often businesses ask about introducing the electronic document flow to minimize paperwork, rightsize the staff, and boost the turnover. However, it’s only a one-dimensional approach.

By switching to automated factoring banks, factors, investment funds, and securitization funds can get:

- An end-to-end digital tool for customer service and multichannel access to factoring and invoice financing

- Online transactions without in-person visits to the office

- Automated matching of payments and receivables for higher business efficiency

- Automated statistics and reports

- Fast and easy upload of receivables

- Adaptability to different products (invoice discounting, loan note, reverse factoring, etc.)

- User roles and models, various levels of access

- Custom interface and business processes (factoring contracts, supply contracts, payment requests, documentation, buyers, etc.)

And all of that can be packed inside a white-label invoice factoring platform that will help your financial business grow at a reasonable investment rate.

The implementation of a factoring module in a bank creates one serious question: should it be added to the existing core banking system or should it work as a stand-alone software module? Working with several software vendors is full of its advantages and drawbacks, yet the HES technical team is ready to elaborate the optimal solution - be it the entire digital infrastructure development or building a separate factoring module with its subsequent seamless integration with the core banking software.

Mobile Factoring and Omnichannel Factoring

According to recent research by Business Insider, 89% of American bank account holders use mobile banking to manage their accounts. For 70% of them, it is the most preferred method of doing that. No wonder mobile banking for businesses is gaining popularity as well. Mobile factoring has a lot of advantages, so we suggest considering them before you start:

- Current reliable information on the state of receivables - on the mobile device

- Opportunity to add new invoices on the go with automatic recognition of uploaded documents

- Bulk authorization of multiple invoices in a few clicks

Despite it is not a must-have for now, implementing mobile technologies has a decent chance to become a competitive advantage.

Automated Receivables Management

One of the most convenient features in digital factoring is automated receivables management. This is what HES business analytics pay close attention to when planning out a factoring platform. The key features usually include these five:

- Convenient bulk import of invoices

- Document storage type (internal or separate)

- Tracking status of receivables, automatic booking of invoice payments

- Notifications about major events (like payout, expiration date, and payback)

- Online counterparties management: adding, modifying, and removing them in real-time.

Factoring Advisory Services

Automation of factoring in banks and financial institutions can provide even more flexibility, time-saving features, and strategic opportunities. For example, via factoring advisory services, which include the following:

- Monitoring the financial performance of counterparties due to receivables overview

- Monitoring invoice settlement lifecycles and important events with the help of automatic notifications

- Reviewing factoring contracts within their lifecycle: setting up limits, profits, and margins

- Analytics: custom reports, AML, and fraud detection

- Risk scoring based on Artificial Intelligence and Machine Learning

- Accounting files preparation (can be integrated with ERP or external accounting software via API or other options)

- Less manual work = fewer operational errors.

Advantages of Custom Factoring Software

Working with stand-alone fintech factoring businesses may seem easier and cheaper in the short-term perspective, but in the long run, it may significantly slow down your business growth. The situation is similar to using out-of-the-box software: if you need any changes, expanded functionality, or slight customization, the task is hardly possible.

Own factoring software is tailored to your business processes and the local legislation is scalable and flexible. Custom factoring modules consider various types of contracts, additional documents, insurance details, accounting data, and other aspects applicable to your business geography.

In addition, customization allows getting a better understanding of goals and facts due to AI-based credit scoring, custom reports, and dashboards. It allows smooth API integration and end-to-end support after the project goes live.

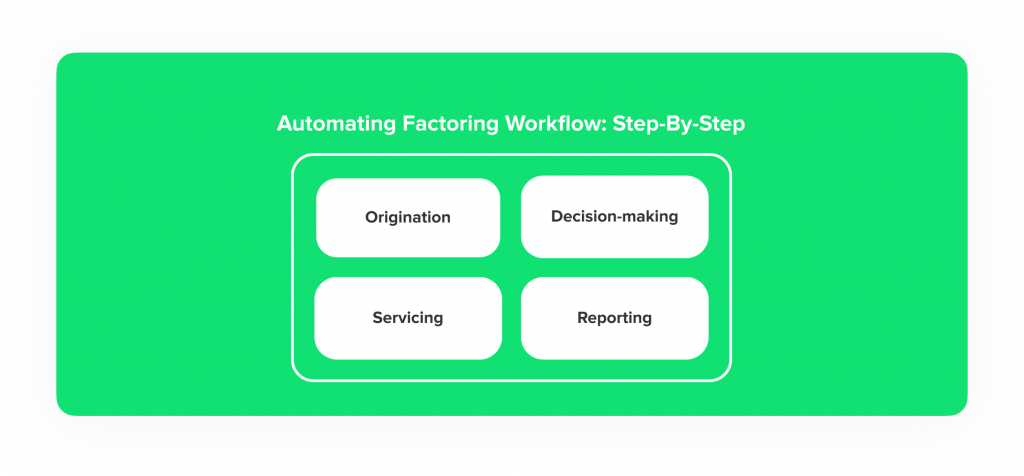

Automating Factoring Workflow: Step-By-Step

1. Origination

From submitting the application, underwriting, and scoring to approval, electronic signature on the document, calculations, and repayment - all of that can be automated and tailored to your needs.

At this stage, HES Factoring software automates:

- Registration, application, and authorization flows

- Underwriting | AI/ML-based scoring | KYC

- Electronic document management

- Due diligence

2. Decision-making

Automation provides an opportunity to assess default risk, improve your capital adequacy ratio and financing, and also make loan decisions faster.

You can introduce your own risk assessment algorithms, leverage predictive analytics by GiniMachine, or integrate with third-party scoring providers.

3. Servicing

Smooth workflow from disbursement to the loan closure can be insured by a highly customizable platform. In addition to servicing the preset deals, you can use a product engine with payment calculation and payment date change to quickly bring new products to market or improve the existing ones.

4. Reporting

Factoring requires careful monitoring, so top-notch interactive dashboards can simplify the task for employees and extract precise facts using easy-to-use tools. An in-built reporting engine by HES will help to create reports of any type based on the uploaded info. Users can export reports in necessary formats and make data-driven decisions.

Psss... Wanna start lending within 90 days?

Read also

Why HES Factoring Software?

- 3-4 months time-to-market. You release your brand-new invoice factoring software while your competitors are still working on it.

- Available source code. No vendor lock-in. You buy it - you own it. Host the solution.

- Open-source tech stack. HES implements free technologies for easy use and easy enhancement. No charges per user, your growth is your income.

- Flexibility. Later on, you can add new modules and features without downtime. New financial products can be launched on the same platform.

Contact us to boost your factoring lending technology today.