We live on tick and that’s OK. Almost everyone takes out loans to, basically, enjoy life today. But this causes enormous competition in the lending market that only omnichannel banking companies are able to withstand. So there come several questions for lenders — isn’t a multi money lending software enough anymore, what’s the odds between omni vs multi channel, and how to drive omni channel customer engagement to outperform each competitor?

In this article, we decided to focus on two main things attracting modern borrowers and turning them into loyal users — multi channel customer experience and omnichannel customer engagement. We’ll tell the difference between multichannel and omnichannel, show how to use the approaches to grow your loan portfolio, and explain why omni channel banking benefits are a must for digital business.

After a critical decline in demand for loans in 2020 due to the Covid crisis, this year promises to be very successful. Many experts including the Mortgage Bankers Association already predict impressive growth in demand for various loans.

- Only US mortgage volumes are expected to top $2.75 trillion in 2021. While other experts including Chris Whalen of Whalen Global Advisors believe that it’s possible to do $3 to $4 trillion this year.

- Considering car loans, consumers are expected to loan up to $7.40 million in comparison to $6.46 million in Q2 2020.

- Lenders expect to gain $4.22 million on personal loans in Q2 2021 against $2.60 million the last year.

To take a churn out of the huge income expected this year, lenders need to adapt to their users. Modern customers don’t choose a provider only for low rates or its location. Their preferences directly depend on their age, social experience, and job position. For example, boomers largely prefer in-person banking where they can communicate with specialists and sign paper documents. Millennials, in contrast, are more likely to apply for a loan via a website or mobile application. So, a key strategy to expand the customer base for lenders is to provide multiple lending channels when each borrower can enjoy the needed service using the most preferable channel. To put it simply, transform your company into a multichannel lending business.

Read also

Why Multichannel Lending?

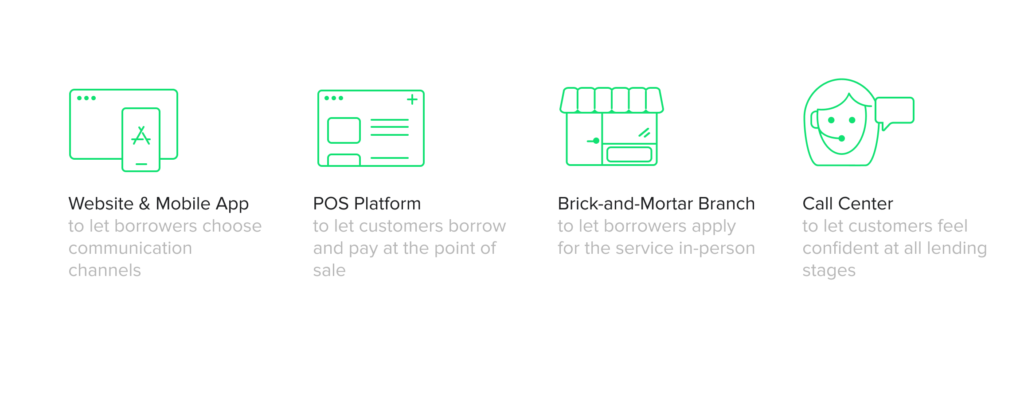

Multi lender platform is a traditional approach when a business owner focuses on separate transactions. With separated processes, banks and lenders offer customers to gain experience via various channels that can exist on their own. Let’s consider how to drive multi channel customer experience and expand your client base.

Website with responsive design

No matter how old are you, we all search for information on every kind of service on the internet. If your lending business doesn’t have a website, the majority of people won’t even know about you. However, a website is not only a marketing unit. It’s also a great alternative to physical lending.

The majority of banks and lenders use a website for demonstration. When borrowers click on a button to apply for a loan, the website redirects them to the contact page to book a call. But what if customers don’t want to communicate in person? Lots of potential borrowers would like to fill out an application form online and wait for approval without unnecessary communications. Moreover, allow customers to choose the communication channel — add a field where they can indicate their phone number, email, or leave messages in their personal account on the website.

To improve their experience, we recommend developing a mobile-responsive website. It allows customers to apply for services from any device, whether it’s a desktop or a smartphone.

Moreover, a mobile multi channel application is also not superfluous. It’s about delivering lending convenience to customers. Imagine that instead of searching for and loading your website, customers just can open a mobile app, check their loan details and debt, the amount of money they borrowed, and their payment deadlines. Using channel automation, you can let customers receive notifications of payments or mail reminders to ensure they won’t miss deadlines.

What to do: Develop a responsive website and multi channel application.

Point of sale platform

Many people decide they need a loan when they're at a store and want to buy something here and now. They don't have time to visit a bank's department, fill out a long application and wait for an approvement. If you offer multi channel POS loans, you win out such customers.

According to McKinsey & Company, POS lending is growing much faster than other similar alternatives — its outstanding balance is expected to reach $160 billion in 2021. The channel accounts for up to 10% of all unsecured lending and will keep growing at unprecedented rates.

Point of sale (POS) lending is a type of personal loan that is usually obtained to pay for purchases, such as smartphones, PC, furniture, kitchen stuff, etc. So, the lender provides finance only to consumers when they're at the point of sale and buy a single product. Such loans are provided via online channel software and platforms almost instantaneously with no application.

What to do: Enter the multi channel POS lending.

Brick and mortar branch

Many users believe that brick and mortar banking is a dying breed. Indeed why do we need to visit a physical bank when everything is available online? Well, such beliefs might cut off your value and reduce your customer base. Surveys show that people trust lenders with physical offices more than fully digital ones. The presence of an office where you can come and discuss any issue leaves borrowers with a feeling of confidence and security. According to Forbes’ research, 39% of users think their money is safer in brick-and-mortar than digital banks. Even Generation Z representatives who practically live online are more willing to apply for their first loan offline.

Trying to expand the customer base, brick-and-mortar is also great to attract baby boomers — the richest and the most interested in lending services generation to date. According to the latest survey, boomers hold $2.6 trillion in buying power. They had more time to build their wealth and are still making more money even if some are retired than other generations. Being non-digital, boomers still use brick and mortar and prefer not to trust online services. Even if the Covid-19 shifted their attitude towards online lending, boomers will continue visiting banks although less often than they used to.

What to do: Don’t give up brick and mortar lending.

Call center

The uselessness of call centers in banks is another myth. Lenders might believe that it’s better to use digital assistants only to speed up lending processes. For one thing, it’s true and customers prefer to wait up to several minutes for a response. However, the majority would like to communicate with a real assistant to find out all the credit granting details instead of a robotic one.

According to Brain & Company, call centers are in demand among all generations and millennials surprisingly call their banks more often than others — 1.4 times on average in a three-month period. It’s almost three times often than older customers (0.5 rate). Besides, 60% of millennials were calling back a call center at least once per three last months, compared with 42% of boomers.

The importance of call centers for millennials and younger generations can be explained by the lack of financial experience. While they understand how digital lending works, they need a specialist to guide them and explain all stages of transactions. Moreover, in case of misunderstanding, people are more willing to call a specialist and solve an issue in real-time rather than waiting for a response by email.

What to do: Establish a call center.

Multichannel lending is great but only the beginning of customer base growth. The approach focused on separated channels is a little bit outdated. If you have time to manage all your channels and customers apart, build reports, and understand your target audience this way, you’re a unique business owner. However, the next step of your multichannel journey is the omni channel customer engagement — something that unites all your channels and simplifies the work.

Omni vs Multi Channel: How to Evolve Lending Approach

Considering the difference between multichannel and omnichannel, the second one connects all your systems by a single online lending platform. Omni channel technology allows catering users throughout the lending journey, from onboarding to debt collection. It creates opportunities to interact with customers on each stage following the most favorable channels, such as a mobile phone, phone calls, emails, or in-person communication in the brick and mortar branch.

Customers opt for a flexible digital experience

Omni channel optimization is for choosing the preferable connection links, and customers appreciate this. Studies show that up to 60% of customers are comfortable with a completely online platform and interaction. And around 30% of respondents prefer a combined approach — online lending application with online and in-person support.

Seamless experience across all your channels

In addition to loan application collection from both online and offline channels, omni channel optimization allows your consumers to start your cooperation on any convenient channel and continue or finish on a different one, preferable by a customer. The software saves the result, so customers can complete their applications without interrupting results. It leads to a high appreciation of your company by customers, increases in completion rates, and drives omni channel customer engagement.

Put your borrowers at the center

Omni channel technology is developed to streamline the lending and focus on customer experience. The dedicated platform allows you to support and guide customers’ digital experience. Whether issues and misunderstandings appear on their way, they can rely on your recommendations or apply for in-person support directly from the platform.

Read also

Wrapping it Up: Omni Channel Software to Expand Customer Base

Considering omnichannel vs multichannel, there’s no great difference between the approaches. Yet omnichannel banking is an updated version of its predecessor that allows uniting all your communication channels into a single platform. We hope that the article gave you some ideas on how to empower your lending, even if you’ve been using multichannel before. If so, omni channel banking benefits might have interested you.

Want to enjoy omnichannel banking? All you need is a cutting-edge digital platform developed by a dedicated team like HES FinTech. Our software can give you more opportunities to provide memorable experiences. Having been over 8 years in digital lending, we understand what your customers need and how to increase your approval rates with only one yet unique multi lender platform. Let us hear your wishes and grow your customer base together.

Need omnichannel customer engagement? Get in touch with our team to start channel automation.