In-house financing has been steadily gaining traction as businesses worldwide are trying to adapt to changing purchasing behaviors, tighter access to traditional credit, and growing demand for more flexible payment options at the point of sale.

As more and more companies are looking to retain control over financing decisions and support customer purchasing power, alternative vendor-led financing models, including in-house financing, have become increasingly common, with the global vendor finance market expected to reach $312.4 billion by 2033.

In this article, we will examine the concept of in-house financing in greater detail, explain how it works, and outline some useful tips on how to start in house financing in your business.

Key takeaways

- In-house finance is a feasible solution to limited access to credit. Businesses that offer financing directly at the point of sale can reduce payment obstacles without relying on external lenders or disrupting the purchasing process.

- Technology and process design are as important as capital. Clear approval standards, automation, and service capabilities, rather than simply the ability to fund loans, are critical for successful in-house financing.

- Different models suit different stages of development. From direct balance-sheet lending to white-label platforms, businesses can select a method that combines speed, control, operational complexity, and scalability.

What Is In-House Financing?

In-house financing is a credit arrangement in which a business extends financing directly to its customers, without involving any external banks for assistance.

In this setup, the company that is selling the product or service assumes the role of the lender, establishes the financing terms, and manages approvals, repayment schedules, and account servicing internally.

Thanks to this, the business is able to apply its approval criteria, structure payment plans around its offerings, and, crucially, maintain direct oversight of the customer relationship throughout the financing period.

3 Main Drivers Behind the Growth of In-House Financing

1. Post-pandemic changes and economic constraints. As we continue to deal with the post-pandemic reality and ongoing economic challenges, including tighter credit conditions, regulatory limits such as credit caps in the US banking system, and stricter lending frameworks in traditional banking, businesses are forced to adapt to changing customer expectations and rethink how they support purchasing power. Within this environment, fintechs step in to help companies deliver innovative credit solutions that are smarter, more effective, and better suited to customer needs.

2. Growth of accessible credit as a fintech trend. Accessible credit has become one of the key fintech trends. Customers are no longer interested in just cards, wallets, and investment products. People want real financial tools that will empower them to handle their everyday needs and make purchasing decisions easier. The IMF Financial Access Survey 2025 also shows that fintech lending and alternative credit models, such as BNPL and marketplace lending, have been steadily growing as a share of total lending across multiple markets.

3. Structural flexibility of fintechs. Fintechs are closely tied to product context and system architecture, which makes them more flexible than traditional banks. They can adapt quickly, provide financing services around real customer needs, and embed credit solutions directly into the user journey.

Taken together, these factors have been driving faster adoption of more convenient and user-friendly financial services. And in-house financing stands out as a key strategy here, helping businesses enhance customer experience, reduce friction, and simplify transactions.

How Does In House Financing Work?

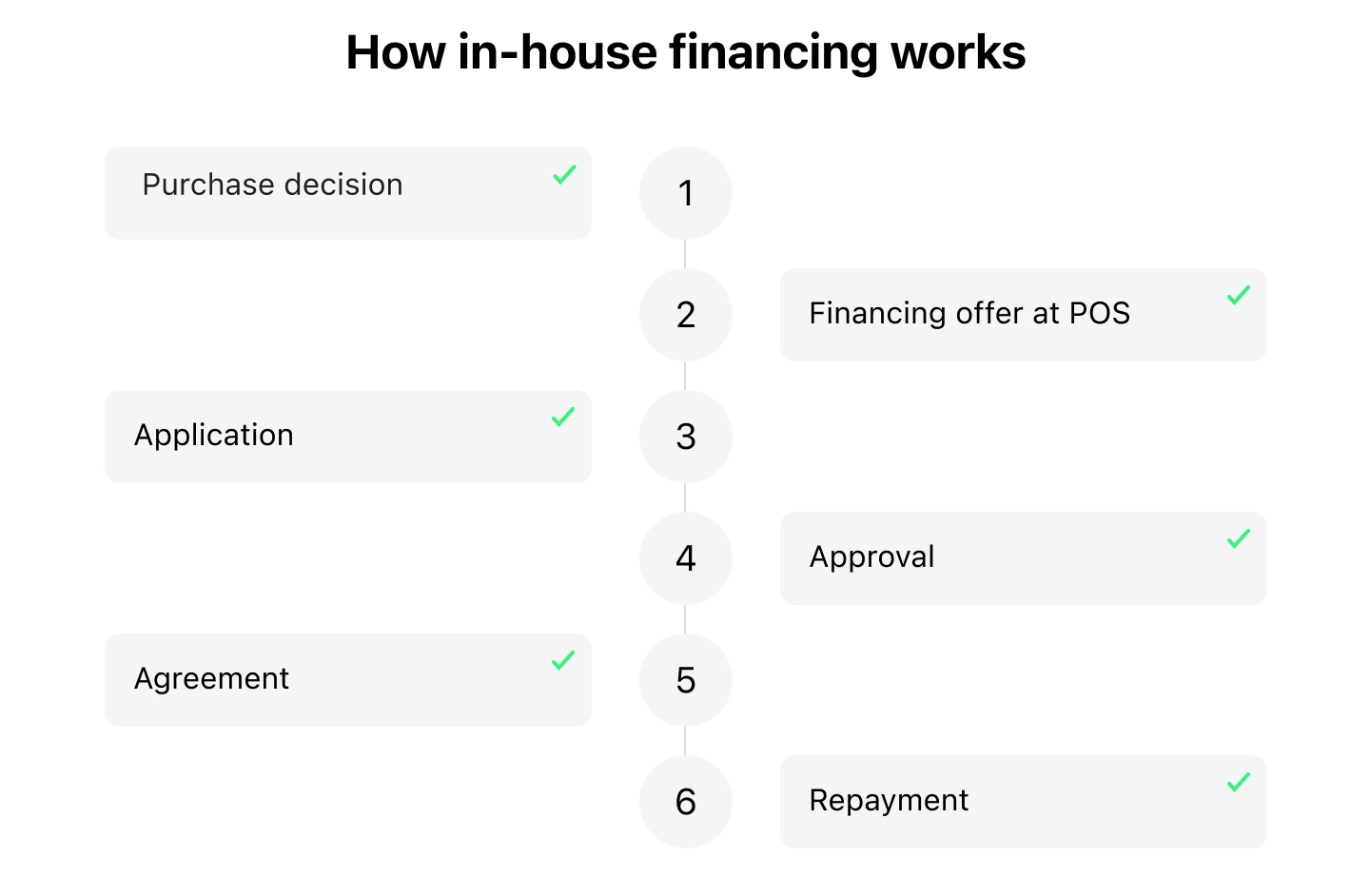

Now that we’ve delved into in house financing meaning, let’s take a look at the stages that businesses need to walk their customers through when offering this financing option.

1. The process begins when a potential customer explores your product or service and evaluates whether it meets their needs. The deciding factor here is whether the cost is manageable for them or not.

2. If paying the full amount at once is an obstacle for the customer, then you can offer them the inhouse financing option. This one will give the customer an alternative without requiring them to leave the sales process and/or seek external funding.

3. Once the customer applies, their information is captured through the internal systems. Many present-day in-house financing setups rely on sophisticated loan origination or point-of-sale financing software to securely collect customer data, assess basic creditworthiness, and achieve compliance with applicable consumer credit regulations.

4. Using predefined approval criteria and risk thresholds, the business reviews the application. During this step, companies can also resort to automated credit scoring and decisioning tools to determine eligibility and appropriate terms. Afterwards, customers receive either approval or a decline.

5. If approved, the customer receives the product or service, and a financing agreement is put in place outlining repayment obligations and timelines.

6. After the sale, the customer makes scheduled payments directly to the business that is fully responsible for billing, payment tracking, reminders, and collections if needed. To alleviate the burden and make the process more efficient for all parties involved, many companies utilize dedicated loan servicing software to automate these tasks, better manage the administrative burden, and maintain clear records for reporting and compliance.

What Benefits Does In-House Financing Offer to Businesses?

When businesses decide to offer in house financing, both they and their customers stand to enjoy a lot of benefits.

Let’s take a closer look at some of the most important advantages that this model brings.

| Benefit | What it means in practice |

|---|---|

| Higher checkout conversion | More customers complete purchases as financing is available immediately at the point of sale |

| Increased sales value | Customers are more willing to spend more when payments are spread over time |

| Better customer experience | Financing feels simpler and more seamless for buyers, with fewer steps and delays |

| Greater operational efficiency | Internal processes get faster and clearer with fewer manual touchpoints |

| Control over financing strategy | Businesses can set their own rules instead of relying on external lenders |

| Stronger unit economics | Financing-related revenue stays in-house and is not paid out to third parties |

1. Stronger Conversion at the Point of Sale

One of the most important benefits of in house financing is its impact on completed purchases.

When customers can secure financing directly during the buying process, fewer deals fall through due to payment friction.

Supporting this, research shows that offering financing at checkout can lift conversion rates by approximately 20 to 30 percent, as customers are able to move forward without delays or external approvals.

2. Larger Basket Sizes and Higher Average Order Value

There’s a psychological factor at play with in house customer financing: spreading payments over time makes higher prices feel more manageable. This implies that when customers know that they can afford a purchase comfortably, they’re more confident saying yes and are ready to purchase even the most costly services or goods.

As a result, businesses enjoy higher average order values and more orders. Plus, as time goes by, customers can even be willing to opt for better models, upgrades, or additional items.

3. Better Customer Experience and Leaner Operations

Many companies that decide to implement integrated credit options report that these tools have helped both make the buying process easier for customers and optimize internal workflows.

In a recent industry survey, 8 in 10 retailers said that integrated financing options improve the overall customer experience. What’s more, in the same survey, 7 in 10 businesses reported better operational efficiency, namely faster approvals, fewer handoffs, and clearer ownership of customer interactions.

4. Greater Control Over Financing Strategy

Another aspect of inhouse financing that businesses really appreciate is that it allows them to define their own approval criteria, repayment terms, and risk thresholds.

With this capability, companies are able to customize financing to their individual products, price points, or customer segments, plus, they are not constrained by external lender policies.

5. Stronger Unit Economics

In-house financing requirements are strict and they do call for thoughtful setup and risk management. However, if the model has been implemented correctly and if default rates and funding costs are controlled, it can strengthen the economics of each sale.

This means that, depending on structure and regulation, businesses may generate additional revenue through interest or service fees. And what is really important is that, compared to third-party financing, the value stays with the business and is not shared with any external lenders.

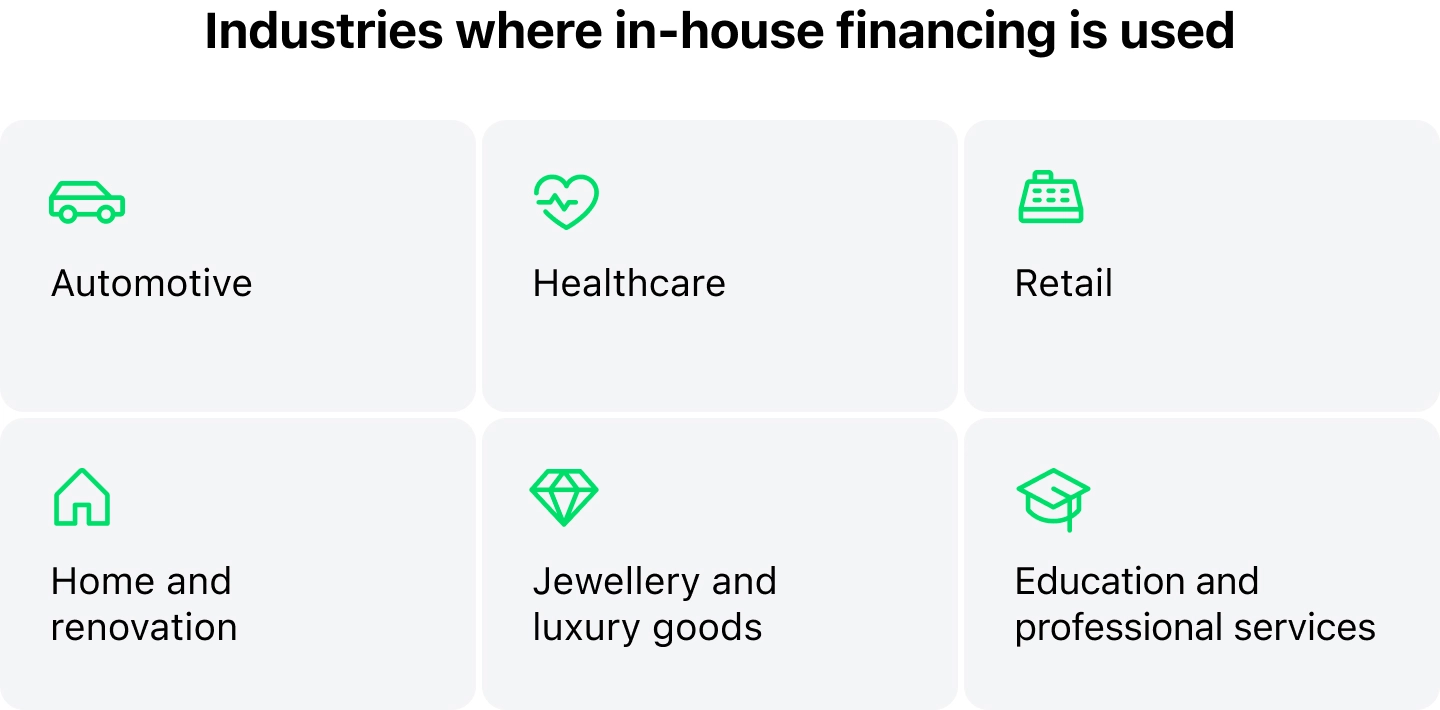

Which Businesses Can Make the Most of In-House Financing?

In-house financing is primarily suitable for businesses where high upfront costs can create hesitation and where providing direct payment flexibility can be the difference between closing a sale and losing it. Besides, to guarantee the successful implementation of this financing option, businesses also need predictable cash flow, a loyal or repeat customer base, and minimal regulatory exposure.

We’d like to stress that while the list below isn’t exhaustive, many other industries and business types can implement this financing model. We’ve highlighted the sectors where this payment option is most commonly used and comes in particularly handy.

1. Automotive Dealerships

By their nature, vehicle purchases are high-ticket transactions, and the obligation to pay the full price straight away can deter some potential buyers from buying a car.

Considering this point, automobile dealerships are increasingly integrating financing directly into the sales experience to help customers afford vehicles and close deals more efficiently. And there are stats that prove that this tactic is viable. According to the report, the integration of embedded finance features in car dealership websites has increased loan conversion rates by more than 30%.

2. Healthcare and Dental Providers

Many patients may delay needed care if they have to pay out of pocket. In this case, offering payment plans that are supported by simple financing and loan servicing tools helps practices to support patients’ needs and reduces the risk of lost revenue due to sticker shock.

3. Retailers and Durable Goods Sellers

Items like appliances, furniture, and high-end electronics are major purchases for many households. But sometimes their high upfront costs can be a barrier to completing the sale.

With in-house financing, though, retailers can make these purchases much more manageable, remove budget-related obstacles, and, as a result, boost their sales and reduce cart abandonment.

4. Home Improvement and Renovation Services

In-house financing lets contractors and service providers in sectors such as renovations, roofing, HVAC, and even renewable energy, like solar installations, deliver structured payment plans that make projects affordable. In addition, this allows businesses to protect their margins and encourages clients to take on bigger projects.

5. Jewelry and Luxury Goods

Back in the day, they used to say an engagement ring should cost three times the salary of the person giving it. Today, couples are spending anywhere from $5,000 to $10,000 on their rings, so it’s clearly a significant expense for many people.

Yet, offering smart in-house financing lets people spread payments over time, making it easier to afford a high-value purchase while still getting a piece of jewelry they’re happy with.

6. Education and Professional Services

Tuition, training programs, and certification courses can be expensive and sometimes fall outside typical student loan or employer reimbursement options.

Because of this, smaller educational providers, bootcamps, and professional services firms are increasingly turning to in-house financing to make their offerings more accessible and, consequently, make education available to more people.

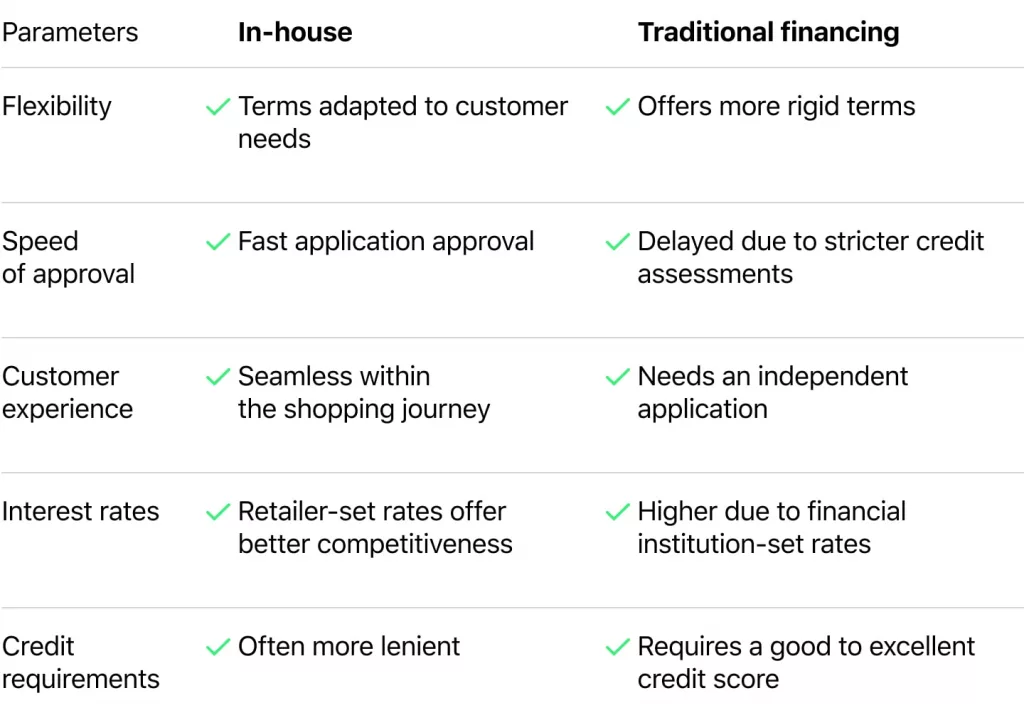

In-House Financing vs Traditional Financing Options

Before embracing in-house financing, it helps to carefully examine how it compares with more traditional financing options so as to better understand which model fits best.

Flexibility

- Traditional financing: Often has rigid terms that may not suit every customer.

- In-house financing: Offers more flexible terms tailored to the customer's needs.

Speed of approval

- In-house financing: Quick approval process, often instant or within a day.

- Traditional financing: May take longer due to more stringent credit checks and approval processes.

Customer experience

- In-house financing: Streamlined and integrated into the shopping experience, making it more convenient.

- Traditional financing: Usually requires a separate application process, which can be cumbersome.

Interest rates

- In-house financing: Rates can be more competitive as they are set by the retailer.

- Traditional financing: Rates are usually set by financial institutions and may be higher.

Credit requirements

- In-house financing: Often more lenient, allowing customers with less-than-perfect credit to finance purchases.

- Traditional financing: Generally requires a good to excellent credit score.

Risk and control

In-house financing: Businesses retain control over terms but take on the risk of defaults.

Traditional financing: Risk is transferred to external lenders but businesses lose control over customer interactions.

In summary, the choice between traditional financing and in-house financing hinges on various factors, including customer needs, business objectives, and operational efficiency. While traditional methods remain a viable option for some, the agility and customer focus offered by in-house financing make it an increasingly attractive alternative for modern businesses. As the landscape of consumer finance continues to evolve, in-house financing stands as a compelling strategy for those aiming to simplify the purchase process and foster long-term customer relationships.

Get a digital strategy for your in-house finance business

Want to get a personalized strategy for your in-house finance business? Take a 5-minute quiz. Select the option that most accurately represents your situation. Once you complete the quiz, you will receive a finance digital transformation strategy tailored specifically for your lending company. Your answers are totally confidential.

How to Offer In House Financing: Model Overview

If you’ve been wondering how to do in house financing, there are some viable implementation models to consider. Each of them assumes different levels of operational maturity, risk tolerance, and long-term growth ambitions.

| Criteria | Direct in-house lending | Dedicated financing entity | White-label lending platform |

|---|---|---|---|

| Who provides the capital | The business itself (on balance sheet) | Separate internal financing unit | Business or funding partner |

| Risk ownership | Fully retained by the business | Retained but isolated in a separate entity | Configurable (business retains control) |

| Control over terms & pricing | Very high | High | High (rules-based) |

| Operational complexity | High | Medium–high | Low |

| Time to launch | Long | Medium | Short |

| Technology requirements | Internal build or custom systems | Dedicated systems and reporting | Ready-made platform |

| Regulatory burden | High | Medium–high | Lower (platform-assisted) |

| Scalability | Limited by internal resources | Moderate | High |

| Best suited for | Large enterprises with lending expertise | Growing companies formalizing financing | Mid-market businesses launching fast |

| Key trade-off | Maximum control, maximum responsibility | Better governance, higher overhead | Speed and efficiency over full ownership |

Now, let’s take a closer look at the most common approaches.

1. Direct In-House Lending (On-Balance-Sheet)

In this model, the business finances customer purchases from its own balance sheet, defines credit terms, approves applications, and manages repayments internally.

The option guarantees full control over pricing and customer relationships but also requires solid risk management, internal processes, and regulatory awareness.

2. Dedicated Financing Entity

Some companies are eager to separate financing activities into a dedicated internal unit or legal structure that is solely focused on customer lending. Such a setup has its own benefits. So, for example, it allows businesses to formalize lending operations, introduce enhanced governance, and better manage financial exposure.

Yet, there is a downside here as setting up and maintaining such an entity can entail a certain degree of legal, operational, and administrative complexity, thus making it a resource-intensive option.

3. White-Label Lending Platforms

White-label lending platforms make it possible to launch and scale in-house financing without having to create lending infrastructure from the ground up. They enable businesses to operate financing programs under their own brand as well as automate main lending processes end-to-end.

Solutions such as HES LoanBox provide a unified technology foundation that covers loan origination, servicing, and repayment management. With such tools in their arsenal, businesses can configure credit rules, approval logic, and loan products with ease. They can also make use of built-in workflows to better handle applications, documentation, and ongoing servicing.

Apart from this, modern white-label platforms come with a set of sophisticated capabilities and functionalities, namely:

- Decision engines and rule builders to automate credit checks and approvals

- Integrated KYC, e-Signature, and payment processing for secure and compliant operations

- Centralized back-office tools for monitoring portfolios, repayments, and performance

- Security features, such as role-based data access, encryption, real-time monitoring

Besides, the most advanced platforms leverage AI-driven capabilities such as rules-based and ML-assisted credit scoring models that help predict default risk, portfolio analytics that surface performance trends, and automated debt collection tools.

Legal Considerations for In-House Financing to Keep in Mind

As with any form of lending, in-house financing comes with important legal responsibilities that should be addressed before introducing it to customers.

Here are some core considerations that are worth reviewing in advance.

- Compliance with consumer protection laws. When offering financing directly, businesses must comply with consumer protection regulations that require transparent disclosure of loan terms, APRs, and fees.

- Fair lending practices. Make sure that your lending process is non-discriminatory. This implies that all customers, without exception, must be treated equally, regardless of their race, gender, age, or other protected characteristics.

- Data privacy and security. Your business must handle personal and financial data responsibly and in line with applicable data protection regulations in each jurisdiction. Plus, remember that you need to provide secure collection, storage, and processing of personal information, as well as give customers clear rights and transparency over how their data is used.

- Interest rates and fees. Be aware of usury laws, which limit the amount of interest that can be charged on loans. Charging above the legal limit can result in legal actions or financial penalties. Besides, remember that any late fees or penalties must also comply with local regulations.

- Collections and default management. Handling customer defaults requires a very careful approach. Therefore, you will need to follow applicable local laws when pursuing collections to avoid illegal practices. In case you’re outsourcing collections, then double-check if third-party agencies follow the same rules.

- Contractual clarity. Your financing agreements should be detailed, precise, and legally sound. Plus, you will be better off if you work with legal experts to guarantee that the contracts are enforceable.

Tips on How to Successfully Integrate In-House Financing into Your Business

For in-house financing to work well and deliver the results you want, it helps to follow a few proven best practices.

Below, we will share practical tips to guide you through the process.

1. Analyze Your Current Processes and Sales

First and foremost, analyze your sales data and customer behavior, and check where deals tend to stall because of high price or upfront cost. These insights are needed to help you fathom out if in-house financing can make a difference or not, and which products or services to prioritize first.

2. Choose the Right Partner

If you’ve decided to go with a white-label platform for inhouse financing, you’ll have to find a vendor that will be a good fit for your brand.

Dig into their reviews and case studies to see if they’ve solved problems for businesses like yours. And once you’ve narrowed it down, don’t hesitate to request a demo or a trial period to see how the software feels in practice.

3. Define Financing and Risk Parameters

Make sure to work out detailed internal rules for eligibility, payment plans, limits, and acceptable risk levels so as to keep decisions consistent, protect your margins, and guarantee that financing remains manageable both for the business and your customers.

4. Address Legal and Compliance Requirements

To avoid or at least better deal with any compliance issues, you should get acquainted with local lending regulations early on. Plus, remember to find out if you need a special license, what customer disclosures are required, and how to regulate interest rates and/or fees.

5. Prepare your team and monitor performance

To get the best results, your sales and support teams should feel confident explaining financing options and working with the new software. Thus, introduce proper training and hands-on guidance so the staff can walk customers through every step with ease.

Chiefly, once the in-house financing system is up and running, keep tracking metrics like approval rates, repayment patterns, and sales performance to see where improvements or changes can make a difference.

Conclusion

In-house financing can deliver substantial benefits to businesses, including higher sales, stronger customer relationships, more efficient and flexible operations, improved margins, and greater control over financing strategy.

To make it work, businesses should focus on analyzing their processes, setting clear rules, staying compliant, and educating their teams.If you want to find out how HES LoanBox can simplify in-house financing and fit into your operations, reach out to our team. We’d be delighted to show you how it works and how it can benefit both your sales and your customers.