Loan origination software (LOS) has become a core component of modern lending operations. However, in practice, it is rarely used as a standalone tool. Instead, it functions as part of a broader lending system that manages the entire borrower journey—from application intake to credit decisioning, disbursement, and ongoing borrower communication.

Modern lending platforms typically combine multiple capabilities within a unified environment:

- loan application systems for digital onboarding

- loan processing systems for document handling and approvals

- decisioning engines for credit scoring and risk assessment

- borrower communication tools for notifications and engagement

These systems are used by consumer lenders, SME lenders, banks, and fintech companies to automate workflows, improve decision accuracy, and scale lending operations efficiently.

The market is expected to reach $9.1 billion by 2030, increasing with a CAGR of 10.5% from 2024. The triggers that drive growth include personalization in lending, the spread of AI, the expansion of digital solutions, and other lending trends, including the rise of advanced loan origination systems.

Banks, credit unions, lenders, and other financial institutions use loan management solutions to cover their needs. They might need it to increase the processing speed, to eliminate human errors, or to adapt to the rising market demands. Before choosing a vendor, it is important to determine the "pains" you wish to cover with the software.

In this guide, we review some of the best loan origination software solutions available today, focusing not only on features but also on how these platforms fit different lending models and operational needs. The comparison is grounded in publicly accessible sources, external reviews, and the general positioning of each product on the market. Assessments of usability, flexibility, and overall fit are therefore indicative, not absolute. Keep in mind that actual performance and capabilities may vary depending on system configuration and the specific needs of each lender.

What Is Loan Origination Software?

Loan origination software is a specialized platform that centralizes and automates the full lending lifecycle, from the moment a borrower submits an application to the final disbursement of funds. At its core, it gives financial institutions structured control over credit assessment, document verification, compliance checks, and approval workflows, replacing fragmented manual processes with a single, auditable system. Depending on the implementation, LOS can function as a focused origination tool or scale into a comprehensive solution that spans both origination and ongoing loan servicing.

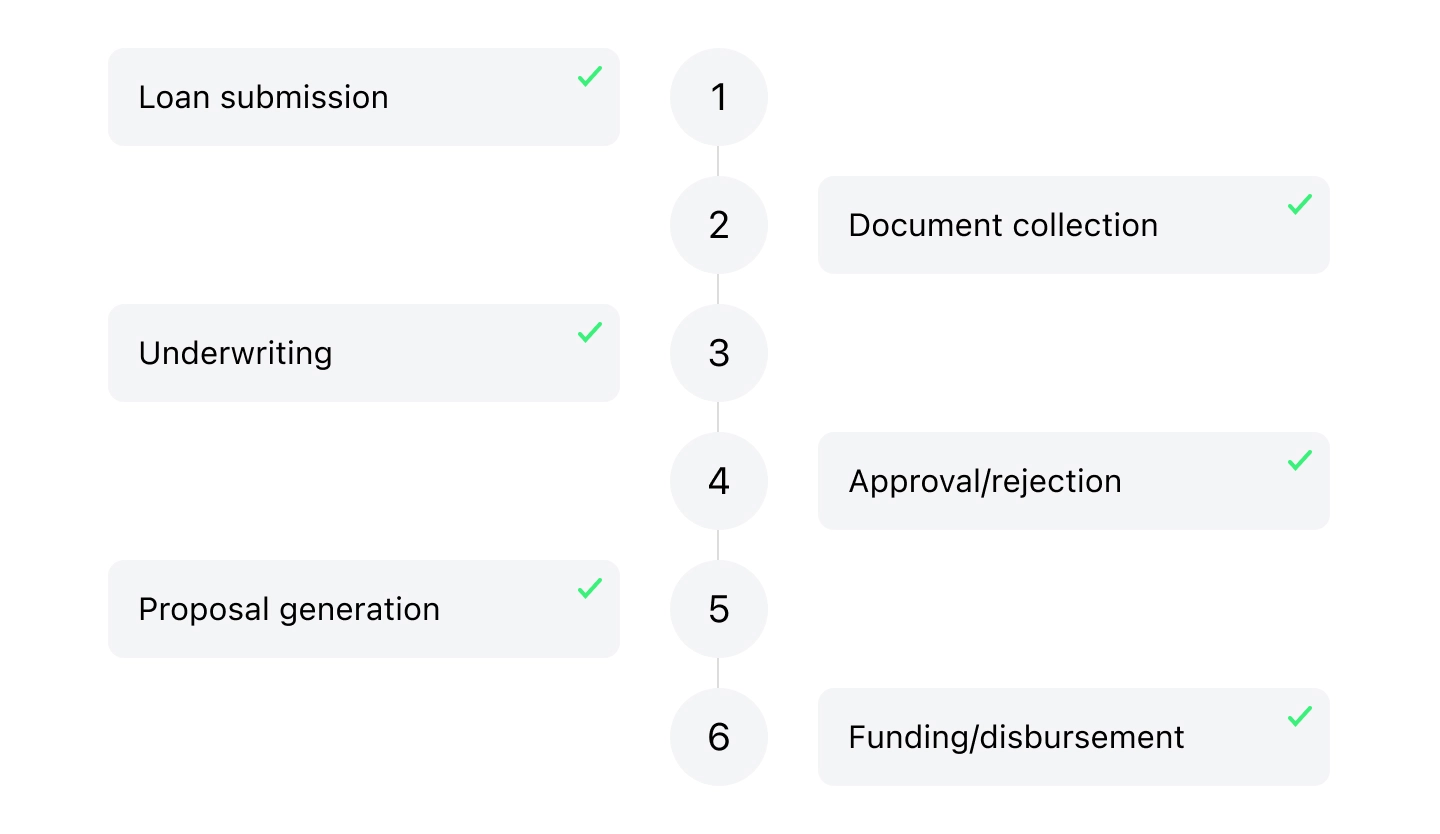

It covers some or all of the following stages: loan submission, document collection, underwriting, application approval / rejection, proposal generation, funding / disbursement

How We Built This Loan Origination System Comparison

This ranking reflects independent research updated by our analyst team in March 2026, making it one of the current overviews of loan origination software available on the market today.

To build it, we first gathered and cross-referenced information from multiple sources: vendor-provided materials and publicly available third-party reviews, including Capterra, G2, Gartner Peer Insights, Software Advice, and Gartner, official product websites and documentation, industry publications, expert reviews, and verified customer feedback. reflecting the state of information as of 2026. Customer reviews from credible platforms, carried significant weight in the final assessment.

Each platform was then assessed using our internal scoring framework. We chose key criteria that reflect what lenders typically care about in real-world implementation: functional depth, feature completeness, usability, and real-world client experience. These criteria were assigned a weight based on how much they impact efficiency, scalability, and long-term results. For example, strong lifecycle coverage and flexible workflows were weighted higher, as they directly reduce manual work and simplify operations.

Within this structure, we also considered how well platforms support the full borrower journey, the flexibility of workflow configuration, and their ability to handle diverse lending products, the quality of analytics and reporting tools, deployment and hosting options, integration capabilities via APIs, and the robustness of document management and auditability.

The scoring was distributed as follows:

- End-to-end lifecycle support (25%)—how completely the platform covers the borrower journey.

- Configurability and workflow flexibility (20%)—how easily lenders can adapt the system to their processes without heavy development.

- Integration capabilities and API flexibility (15%)—availability and maturity of APIs, prebuilt integrations (e.g., CRMs, payment providers, credit bureaus), and their ability to operate within an existing tech ecosystem

- Feature depth and product coverage (15%)—the richness of core origination features, including document management, decisioning tools, scoring capabilities, and support for different loan types.

- Usability and user experience (10%)—includes both borrower-facing interfaces and internal tools for underwriters and operations teams.

- Deployment options and scalability (10%)—support for cloud, on-premise, or hybrid deployment, and how well they scale across different portfolio sizes and geographies.

- Analytics, reporting, and auditability (5%)—availability of dashboards, reporting tools, and audit trails, which are essential for monitoring performance and ensuring compliance.

This ranking does not reflect a single “best” solution for all lenders. Instead, it evaluates overall platform strength in areas that most impact implementation success, operational effectiveness, and long-term return on investment.

List of the Best Loan Origination Software Vendors in 2026

As “loan origination software” is not a single product category in practice, we first separated the list into two groups: full-spectrum LOS systems that function for a broad range of lending models and operational setups, and the ones where compliance, document handling, and workflow depth are optimized primarily for mortgage origination workflows. This separation makes it easier to compare vendors against the realities of a lender’s business model rather than against a generic feature list.

Further, you can find a more detailed overview of each software solution: the table contains key facts, while further details are covered in the overview below.

Loan Origination Platform Comparison Tables

Full-Spectrum LOS Platforms Table

| Platform | Positioning | Key strengths | Best for | Free trial | Price |

|---|---|---|---|---|---|

| Finastra (Loan IQ) | Enterprise-grade lending system for complex and corporate loans | Advanced handling of syndicated and structured loans, strong risk and compliance capabilities | Large banks handling complex corporate or syndicated lending | Not available | Upon request |

| HES LoanBox | Scalable, AI-powered modular lending platform for end-to-end loan origination | AI decisioning, full customization in deployment, products, and workflows, modular architecture, 100+ integrations | Lenders needing scalable, fully customizable, AI-driven origination and lending automation | Available | Upon request |

| TurnKey Lender | AI-driven lending automation platform | AI decisioning, configurable workflows, servicing, collections, global scalability | Lenders and credit unions needing scalable AI automation | Not available | Upon request |

| nCino | Enterprise cloud banking platform (Salesforce-based LOS) | Strong workflow automation, compliance tools, CRM-native architecture, robust reporting | Banks and large financial institutions already using Salesforce ecosystem | Not available | Upon request |

| MeridianLink Consumer | Consumer LOS for credit unions and community banks with shared data layer across origination, deposits, and collections | Multi-product consumer origination, indirect lending engine, one-pull cross-sell, deep core-banking integrations | Credit unions and community banks running multiple consumer loan products that want an established LOS with strong compliance support | Not available | Upon request |

Software for Mortgage LOS Leaders Table

| Platform | Positioning | Key strengths | Best for | Free trial | Price |

|---|---|---|---|---|---|

| Encompass | Enterprise mortgage loan origination system | Deep mortgage workflows, strong compliance (US), large integration ecosystem, industry-standard processes | Mid-to-large mortgage lenders needing a compliant, standardized LOS | Not available | Upon request |

| LendingPad | Cloud-based mortgage LOS for brokers and small lenders | Lightweight LOS, fast setup, user-friendly interface, cost-effective | Mortgage brokers and smaller lenders needing a simple LOS | Not available | Upon request |

| Blend | Borrower-facing front-end platform that sits in front of a back-office LOS | Source-connected data capture (payroll, banking, tax, identity), modern borrower UX, LOS connectors to Encompass and MeridianLink | Banks, credit unions, and mortgage lenders running an existing LOS that want to modernize the application experience | Not available | Upon request |

Top Loan Origination Software With Full-Spectrum Functionality

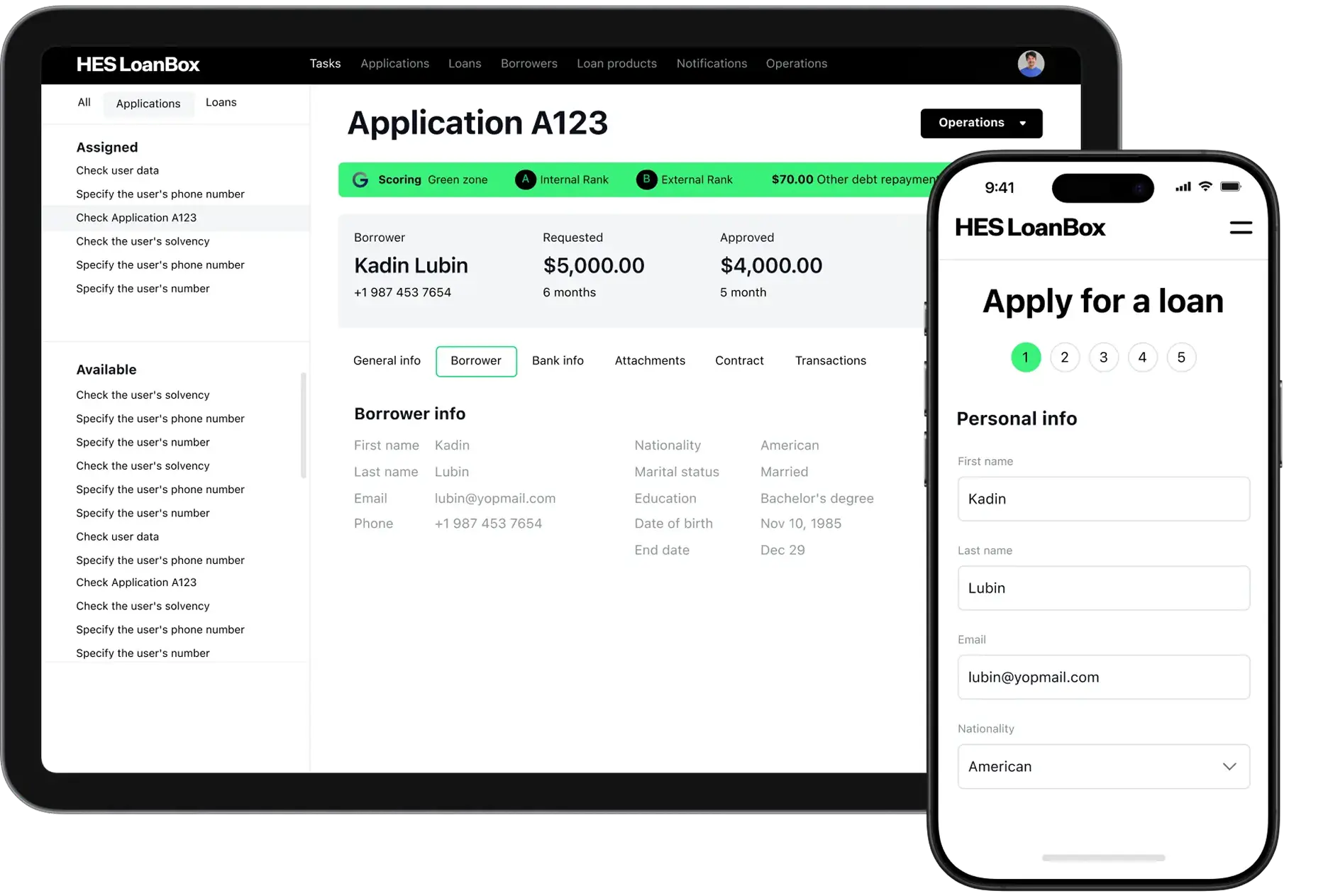

HES LoanBox - strong configurable loan origination platform for alternative lenders.

HES LoanBox is a modular loan origination platform built on open-source technologies — Java, Camunda, and others — which means institutions retain full access to the codebase and can purchase a developer license, avoiding vendor lock-in.

LoanBox is best for: lenders needing robust modular loan origination solution, customization, AI decisioning, and multi-product flexibility.

The architecture lets lenders deploy specific modules alongside existing infrastructure or implement the full end-to-end stack. The platform supports SME lending, BNPL, mortgage, auto lending, and other loan types, with workflows configured to match each institution's credit logic rather than a fixed template. Security is handled at the infrastructure level: HES LoanBox is ISO 27001 certified and hosted on AWS or Google Cloud with a Java LTS stack.

Key features

- End-to-end origination: application intake, document handling, credit scoring, approval, and disbursement in one flow.

- AI decisioning engine: real-time risk scores, stop-factor checks, in-built scorecards, and customizable AI models for credit limit calculation.

- Full loan lifecycle: servicing module covers repayments, rescheduling, delinquency tracking, and automated collections — including AI-driven recovery with region-specific compliance.

- Configurable product engine: launch any loan type with flexible terms, rates, and repayment schedules via a no-code interface.

- BPM workflow automation: no-code process builder with multi-workflow support, role-based access control, and full customization of scoring logic and UI.

- Multi-entity and multi-currency: manage multiple legal entities, currencies, and jurisdictions from a single instance.

- 100+ integrations: APIs, credit bureaus, CRMs, payment gateways, and internal systems.

- White-label suite: branded borrower portal, landing page, and back office.

- Security: ISO 27001 certified, KYC/KYB support, encryption, audit trails — cloud and on-premise.

- Real-time analytics: KPI dashboards, portfolio metrics, and BI integrations.

Users like: Modularity, full freedom of customization that supports any loan type, AI-powered predictive model that covers every stage of loan origination. Users on Capterra praise the platform's ease of configuration and integration, with one Head of Technology calling it «a real turnkey out-of-the-box solution» after 2+ years of use. G2 reviewers highlight flexibility in practice — multi-entity and multi-currency setups, connections with local banks and data vendors — noting the platform adapts to existing workflows rather than forcing teams to rebuild around it.

Users don't like: Complex initial setup that requires vendor involvement and multiple configuration rounds; no industry-specific templates for non-lending verticals (ex. green finance, leasing)

Rating: 4.9/5 on Capterra; 4.8/5 on G2

Price: upon request. Fixed subscription (no limits on users, products, or applications).

Notable clients: ID Finance (unicorn), Fintuinity, Wa'ed, Alraedah, etc.

Demo and trial period: free demo and trial available.

Link to the product: here

TurnKey Lender - strong AI-decisioning / automation-led alternative.

TurnKey Lender is a global, AI-powered lending automation platform that supports the full lending lifecycle—from origination and underwriting to servicing and collections. The company states that it serves clients in over 50 countries and integrates AI-driven decisioning, configurable workflows, document management, and collection strategies.

Best for: Global financial institutions, online lenders, and credit unions looking for a sophisticated, AI-driven platform that can scale internationally.

Key features

- AI-based decision engine using neural networks and alternative/conventional data

- Configurable loan application flows with document templates and custom fields

- Modular servicing and collection tools with configurable collection strategies

- APIs and integrations for credit bureaus, payment systems, verification services

- Interfaces for borrowers and back-office users with dynamic workflows

- Support for multi-product lending (consumer, commercial, embedded finance, auto lending, SME lending, MCA, etc.)

Users like: Powerful automation and configurability; broad international reach; robust decisioning and collection modules. Users on review platforms emphasize TurnKey Lender's flexibility in launching new credit products "very easily", strong API support, and responsive teams.

Users don't like: Customizations may incur higher cost; initial implementation can be complex ; UI and terminology may require additional localization for non-US markets; some users report reliability issues and inconsistencies between promised and delivered functionality. Some users report early-stage glitches and occasional limitations in document automation.

Rating: 4.7/5 on G2; 4.6/5 on Capterra

Price: upon request.

Demo and trial period: demo is available; trial period is provided case-by-case, but often restricted.

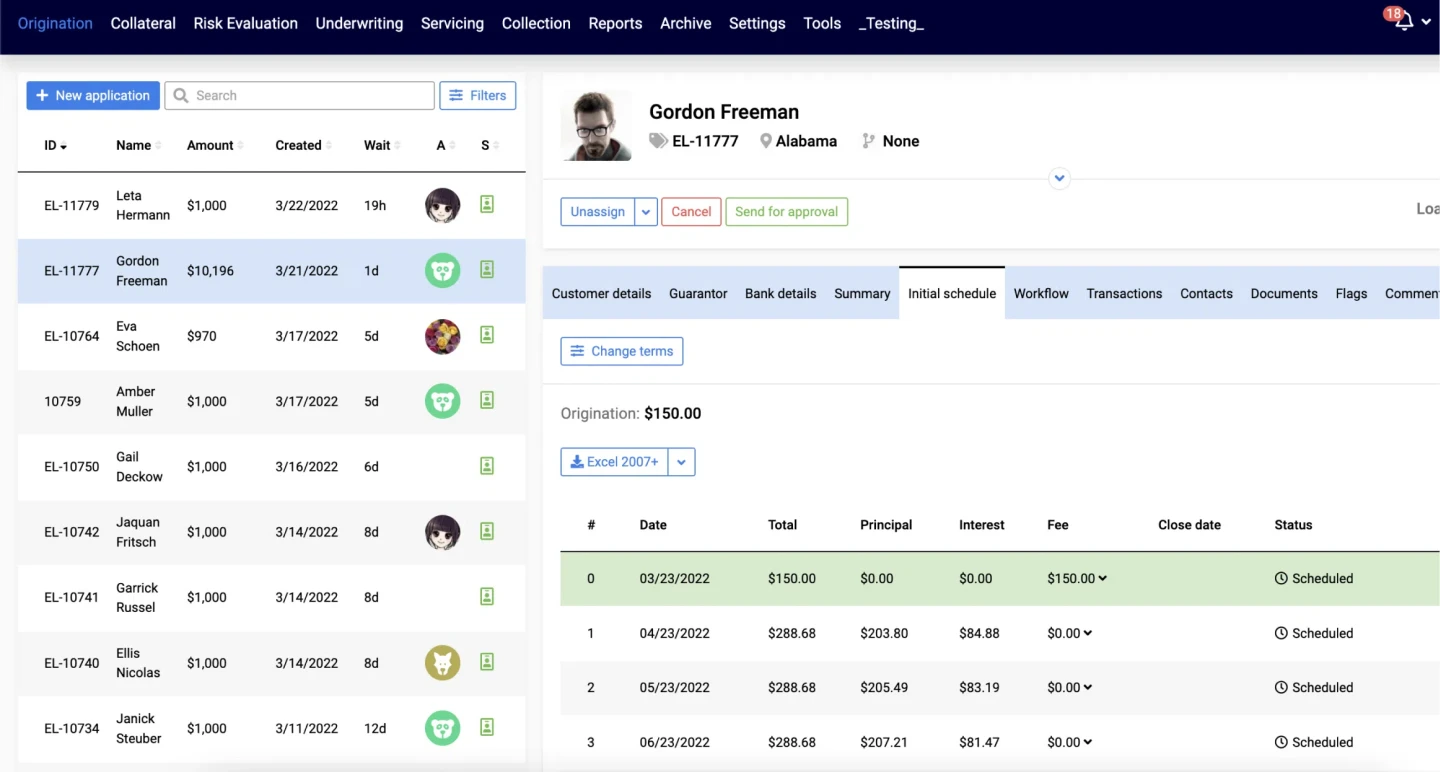

nCino - cloud-native LOS built on Salesforce and designed for banks

nCino is a cloud-based loan origination and banking platform built on top of Salesforce, which supports onboarding, application handling, underwriting, and loan approvals.

Best for: mid-sized and large banks, credit unions, and enterprise lenders working within the Salesforce ecosystem (or those planning to build around it), where oversight and strong compliance support are critical.

nCino works as part of a broad ecosystem: it helps connect the dots between lending processes, CRM data, and internal workflows, which enables teams across departments to keep everything centralized and accessible.

At the same time, the reliance on Salesforce means implementation can take longer and often requires more planning compared to lighter, standalone solutions. Overall, nCino is more about creating a consistent, well-governed lending environment that can scale across teams and regions.

Key features

- Salesforce-based foundation: as the platform is built directly on Salesforce, customer data, relationships, and lending processes are tightly connected.

- End-to-end origination: the system supports onboarding, applications, credit analysis, approvals, and document handling.

- Centralized data: borrower and loan data are kept in one place, which reduces duplication and improves visibility across teams.

- Workflow automation: configurable flows help standardize processes and reduce manual handoffs.

- Multi-product support for commercial, SME, retail, and mortgage lending.

- Compliance and audit tools: built-in tracking, documentation, and audit trails are aligned with regulatory requirements.

- Reporting and dashboards: Salesforce reporting tools providing pipeline visibility and performance tracking.

Users like: nCino's users appreaciate the cloud-based infrastructure of the platform, as customers can see the status in real time. Many users mention good coordination between sales and credit departments, along with stronger process control.

Users don't like: Implementation can be complex and require extensive customization. Several users suggest improvements in UX for help screens and technical issues in the approval process.

Rating: 4.2/5 on G2; 4.3/5 on Capterra

Price: upon request.

Demo and trial period: demo is available.

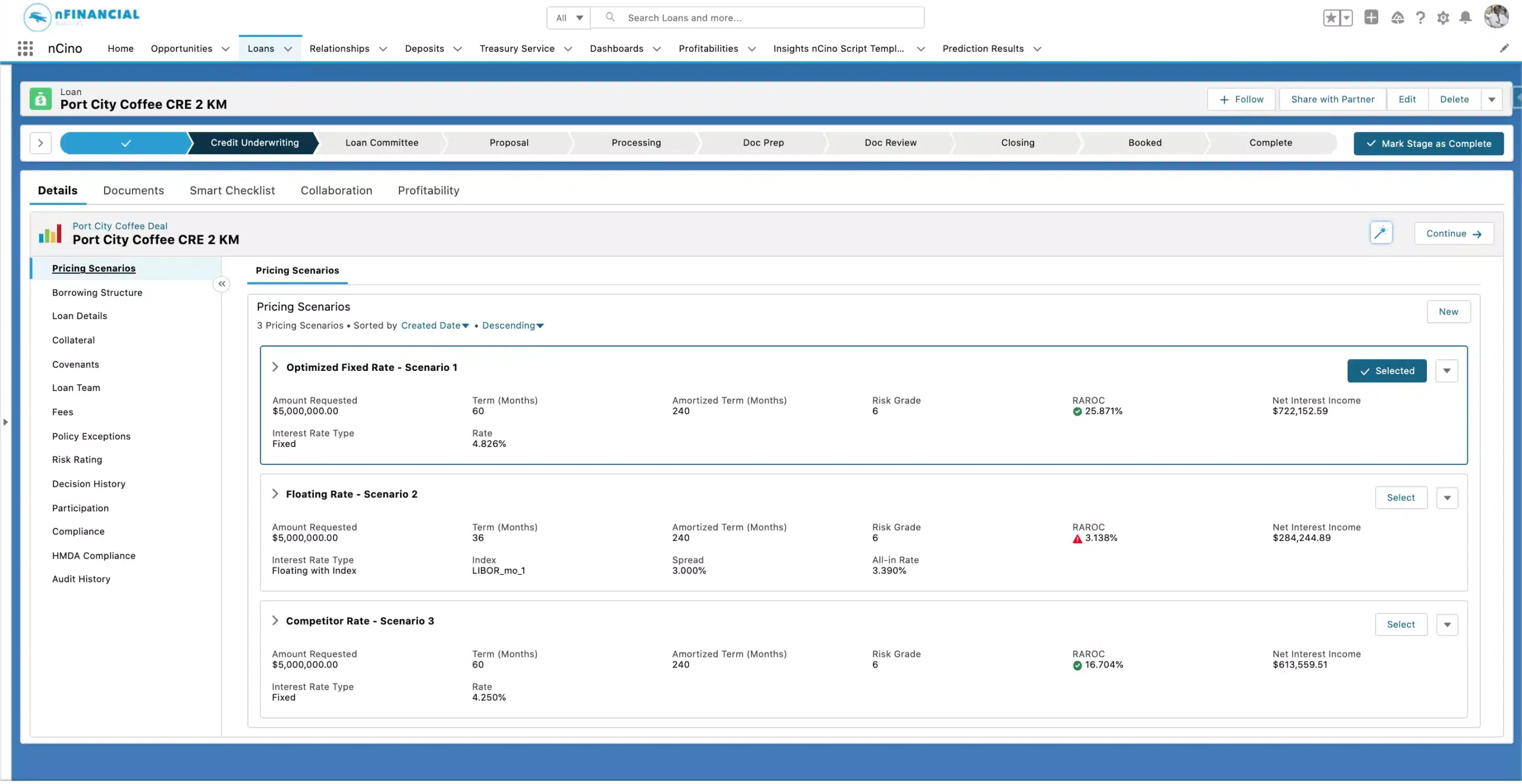

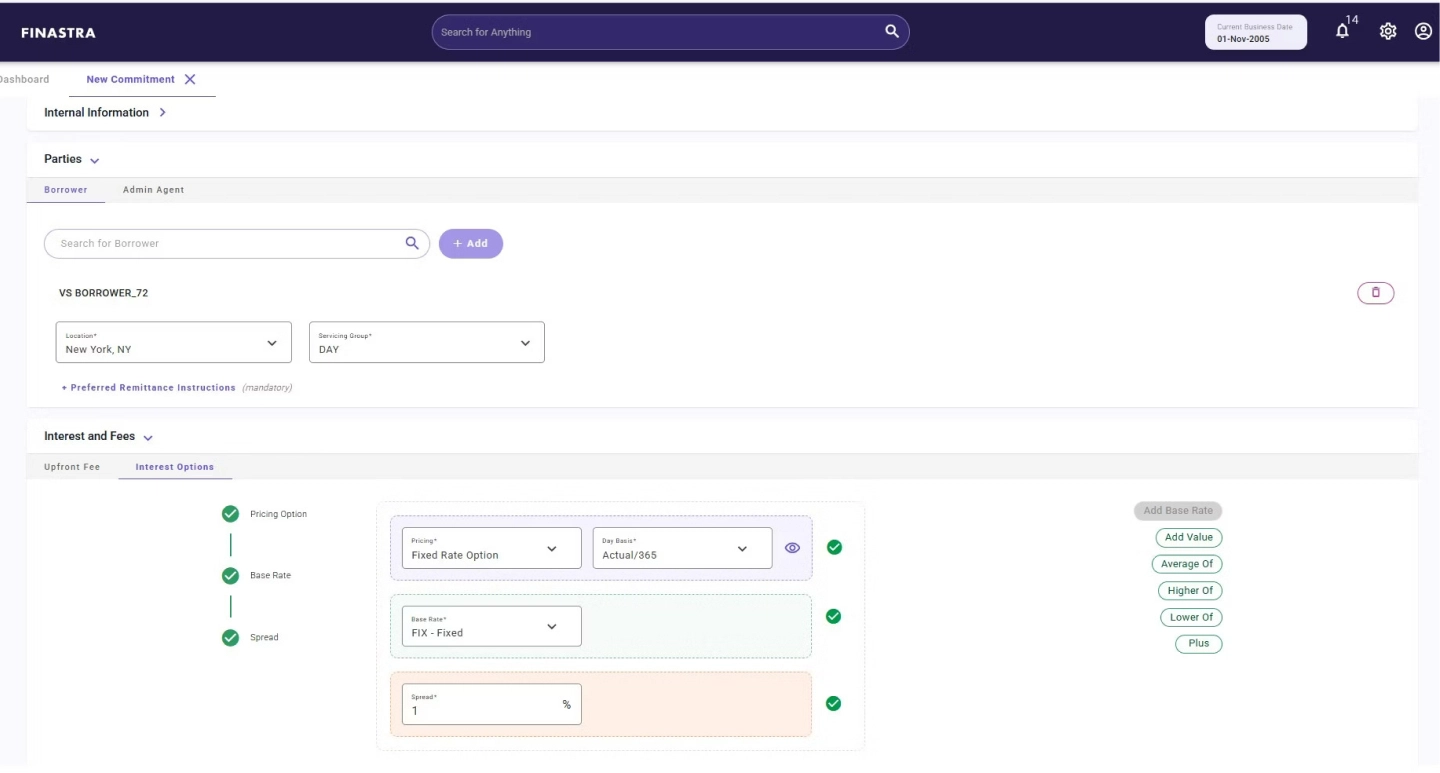

Finastra (Loan IQ) - enterprise-grade platform focused on complex commercial and syndicated lending

Finastra Loan IQ is a commercial loan servicing platform designed to help financial institutions manage the full lifecycle of lending, from origination intake through servicing, trading, settlement, and closure within one system.

Best for: large banks and financial institutions handling syndicated, commercial, and corporate lending, where complex deal structures, servicing depth, and regulatory control are key priorities.

Key features:

- End-to-end commercial lending lifecycle: supports the full process within one system.

- Syndicated and complex deal management: handles multi-lender structures, structured finance, and advanced pricing models, including multi-tranche and multi-currency facilities.

- Centralized loan portfolio management: supports multiple lending products and business lines within a single platform.

- Integration-ready architecture: connects with upstream origination systems, accounting platforms, CRM tools, and external market infrastructure.

- Reporting and dashboards: provides visibility into portfolio performance, risk exposure, and operational metrics through configurable dashboards.

Users like: In official testimonials, reviewers often highlight the platform's ability to handle multi-lender deals, detailed loan structures, and large portfolios with high accuracy.

Users don't like: At the same time, feedback often points to the system’s complexity. Implementation might take long and may require specialized expertise and significant integration work.

Rating: 3.3/5 on Gartner.

Price: upon request.

MeridianLink Consumer - Consumer Loan Origination for Community Banks

MeridianLink Consumer, rebranded from LoansPQ, is a U.S. consumer LOS used predominantly by credit unions and community banks. It sits inside MeridianLink's broader product family, where origination connects to credit reporting, account opening, mortgage, and collections through a shared data layer the vendor calls Access. Whether that shared layer translates into a real operational advantage depends heavily on which of the surrounding products an institution already runs — for lenders using only origination, the architectural benefit is limited.

Ideal for: Credit unions and community banks running multiple consumer loan products — auto, credit card, personal, HELOC — that want an established LOS with deep core-banking ties.

Cross-sell is a frequent point of discussion in product reviews: a member applying for an auto loan can be screened against other products on the same credit pull, governed by rules the institution defines. The platform unifies direct, branch, and indirect channels into one underwriting queue. Day-to-day configuration is done by business users through guided screens, but anything outside the standard rule engine typically routes through MeridianLink's professional services team.

Key features

- Multi-product consumer origination: unified application flow across auto, personal, credit card, HELOC, and unsecured lending.

- Indirect lending engine: dealer portals, decision automation, and funding flows for dealer-channel acquisition.

- One-pull cross-sell logic: evaluate multiple product offers against a single credit bureau request.

- MeridianLink Access: shared data layer connecting origination with the vendor's deposit, mortgage, and collections products.

- Rule-driven decisioning with override paths: auto-decisions with manual review trails.

- Built-in compliance handling: Reg B adverse action processing, ECOA notices, disclosure templates aligned with NCUA and FFIEC guidance.

- Pre-built integrations: Experian, Equifax, TransUnion; cores including Symitar, Corelation, and DNA.

- Member-facing intake: branded online application with save-and-resume, conditional logic, mobile support.

- Reporting suite: funnel analytics, decision-consistency reports, fair lending dashboards.

Users like: Reviewers point to platform stability across high application volumes and the breadth of pre-built connections to cores and bureaus. Credit unions specifically mention that the workflow assumptions match how their lending teams actually operate, with one G2 reviewer calling out that automated decisioning let them auto-approve roughly 50% of standard loans.

Users don't like: The interface looks dated — one Capterra review describes the back office as "dated and can be a little confusing to navigate… still clunky," and similar language appears across reviews on Software Advice and GetApp. Configuration past the standard rule engine usually routes through vendor services — multiple reviewers note they cannot rename fields or change required/optional logic without contacting MeridianLink Support. Self-hosted institutions report friction coordinating update windows. Earlier feedback also flagged the decision engine as the weakest part of the product, though the vendor has been iterating on it.

Rating: 4.1/5 on G2 (across the MeridianLink product family); Capterra reviews trend in a similar range.

Price: upon request. Base platform fee plus per-module licensing.

Notable clients: Published case studies on the MeridianLink website include A+ Federal Credit Union (Central Texas), Rogue Credit Union (Oregon and western Idaho), APL Federal Credit Union (Maryland) etc.

Demo and trial period: Demo available via sales contact; no open trial.

Software for Mortgage LOS Leaders

Encompass by ICE Mortgage Technology - strong enterprise U.S. mortgage specialist

Encompass is one of the most widely adopted mortgage loan origination systems (LOS) in the U.S., developed by ICE Mortgage Technology (formerly Ellie Mae). It provides a comprehensive platform for managing the full mortgage lifecycle—from initial borrower application and underwriting to closing and post-closing investor delivery. The system integrates seamlessly with the ICE ecosystem, including product and pricing engines, document management tools, and eClose solutions. Encompass is recognized for its strong compliance coverage, extensive partner network, and enterprise-level scalability, making it a cornerstone solution for many banks and credit unions.

Best for: Mid- to large-size lenders, banks, and credit unions needing a unified, compliant, and scalable LOS

Key features:

- End-to-end workflow automation: Centralized loan management from origination to investor delivery.

- ICE Partner network: 500+ verified integrations with credit, appraisal, and title vendors.

- ICE PPE: Real-time rate quoting and best-execution pricing analysis.

- eClose functionality: Full digital closing with eSign, eNote, and MERS eRegistry support.

- Compliance engine: TRID, HMDA, and RESPA checks with real-time updates.

- Borrower portal: Online applications, document upload, and secure messaging.

- Document management: Intelligent document recognition and data extraction.

- Pipeline and analytics tools: Dashboards for loan tracking, profitability, and pipeline health.

Users like: Industry-leading LOS with robust compliance, extensive integrations, and high scalability. Reviewers on Capterra and G2 describe Encompass as a solid, all-in-one tool for mortgage origination. Users appreciate the extensive functionality and integrations but mention the "antiquated interface" and "steep learning curve."

Users don't like: Expensive and complex to implement; potential vendor lock-in; users report dated UI and slower performance under heavy loads.

Rating: Capterra: 4.0/5

Demo and trial: Demo is available; free trial is not available

Price: upon request

LendingPad - strong modern mortgage LOS challenger

LendingPad is a cloud-native mortgage LOS developed in 2015 to modernize lending workflows through real-time collaboration and accessibility. The platform supports retail, wholesale, and correspondent lending, allowing multiple users to work simultaneously on the same loan file. LendingPad offers an integrated CRM, automated compliance tracking, and seamless integrations with credit bureaus, appraisal services, and title companies. It is known for its affordability and modern design compared to legacy systems like Calyx Point.

Best for: Mortgage lenders and brokers seeking a collaborative, cloud-based LOS with lower total cost of ownership.

Key features

- Real-time collaboration: Multiple users editing the same loan simultaneously.

- Cloud architecture: 100% web-based platform accessible from any device.

- Integrated CRM: Built-in lead and campaign management.

- Compliance tracking: Automated QM and disclosure management.

- Third-party integrations: Credit, appraisal, and title connectivity.

- Document management: Secure cloud storage and e-signature support.

- Live pipeline dashboard: Real-time loan updates and notifications.

Users like: Modern, user-friendly interface; strong collaboration tools; cost-effective pricing; built-in CRM. Users on G2 and Capterra describe LendingPad as "intuitive, easy to use, and affordable." Many highlight its responsive support team and say it "modernized our workflow overnight."

Users don't like: Disclosure automation less straightforward than some users expect — requires manual setup; limited support options available; POS functionality requires a separate third-party tool with additional subscriptions.

Rating: Capterra: 4.4/5; G2: 4.7/5

Demo and trial: Demo is available; free trial is not available

Price: upon request

Blend - Front-End Origination Platform for Banks

Blend is a borrower-facing application and document-collection platform that sits in front of a back-office LOS rather than replacing it. The product originated in mortgage and has expanded into consumer lending, deposits, and home equity, though mortgage remains its primary install base. Lenders using Encompass, MeridianLink, or other systems can run Blend at the top of the funnel and pass a completed file into their existing underwriting system. The tradeoff is that the LOS stays in place — and on the budget — alongside Blend.

Ideal for: Banks, credit unions, and mortgage lenders that already operate a back-office LOS and are willing to add a separate front-end platform to modernize the borrower experience.

The product's distinguishing technical choice is automated data capture in place of document upload. Income, asset, tax, and identity data can be pulled from sources like Argyle, The Work Number, Plaid, Finicity, and the IRS, with the borrower authorizing each connection inside the flow. For straightforward files the application can be completed in under an hour, though files with non-standard income sources, manual exceptions, or borrower drop-off mid-flow often still require traditional document handling.

Key features

- Digital mortgage application: 1003 with conditional questions, save-and-resume, device parity.

- Source-connected data capture: payroll, banking, tax, and asset verification pulled from third-party providers.

- Consumer lending module: same model applied to personal, credit card, auto, and home equity products.

- Loan officer workspace: pipeline status, borrower messaging, and document review in one interface.

- LOS connectors: integrations with Encompass, MeridianLink, and others.

- Automated income analysis: calculation logic for W-2, self-employed, and rental income with audit trail.

- Disclosure and eSign handling: initial and closing disclosures managed in-platform with regulatory timing.

- Audit log: borrower interactions, data sources, and timestamps captured for examiner review.

- Embeddable flow: white-labeled application that drops into a marketing site or member portal.

Users like: Reviewers point to the platform's customizability as its main strength — teams report being able to shape the borrower-facing interface to match their workflows while presenting a clean, modern experience to applicants. Integrations with adjacent tools like DocuSign and back-office LOSs such as Encompass are frequently mentioned as smooth and reliable.

Users don't like: The platform doesn't remove the LOS line item — it adds a new one, which makes total stack cost rise rather than fall. Multiple Capterra reviews note that heavy customizability can create training delays and confusion for large user bases. Some reviewers — including borrowers, not just lender-side users — report frustration with the eSign flow and document portal not working as expected; one Capterra review by a Truist customer is particularly blunt about the borrower experience. Configuration of non-standard question logic typically routes through Blend's professional services rather than self-service tools. Several reviewers have also noted slower release velocity in recent years.

Rating: Capterra reviews vary widely; G2 maintains a separate Blend Mortgage Suite profile.

Price: upon request. Most contracts run per-application or per-funded-loan with a minimum annual commitment.

Notable clients: Published case studies and announcements on Blend's site confirm partnerships with Langley Federal Credit Union, University of Wisconsin Credit Union, Baxter Credit Union (BCU), Landmark Credit Union, Randolph-Brooks Federal Credit Union, and others.

Demo and trial period: Demo available; no open trial.

What Are the Top Loan Origination Software Features?

Loan origination software streamlines the workflow and reduces the risks of errors. And it does so due to the following functionality:

Application processing: LOS provides a possibility to store and process loan applications. The digital onboarding version of the software allows borrowers to submit applications online, eliminating the necessity to manually fill in paper forms. As a modern loan processing software, it saves time and reduces mistakes.

Document management: LOS allows lenders and borrowers to store their documents digitally. Therefore, authorized stakeholders can access any files instantly from anywhere. Possibilities like the generation of promissory notes, deeds of trust, and eSign increase customer satisfaction.

Credit decisioning: At this stage, the documents provided by the borrower are saved, and the lender makes a decision regarding their creditworthiness. Modern systems go beyond traditional credit bureau data by incorporating alternative data scoring. This technology analyzes non-traditional points, such as utility payments and transaction history, to build accurate risk profiles for borrowers with limited credit histories. Automated algorithms and AI smart scoring solutions replace legacy manual methods, ensuring fast analysis and relevant decision-making.

Compliance with regulations: There are multiple regulations that govern the lending industry. An LOS system is designed to support compliance with regional regulations governing security, accountability, and transparency. Key examples include TILA and RESPA in the United States, and the Consumer Credit Directive (CCD) and GDPR in the European Union. Enterprise-grade platforms also maintain SOC2 Type II compliance, ensuring that strict internal controls for data protection, availability, and confidentiality are consistently met. These controls lower the threat of financial penalties and legal challenges.

Reporting and analytics: The software provides lenders with valuable insights regarding application trends and metrics such as pull-through rates, loan volume, abandonment rate, etc. These KPIs help to make data-driven decisions regarding pricing and credit policy, resource allocation, etc.

Integration capabilities: Powerful and modern LOS systems provide integration possibilities. The easier the connection is, the better and more convenient the software is for the lender. Possible integrations might include core banking systems, CRMs, credit bureaus, and document verification services via APIs. It results in fast information exchange and convenient operations.

Credit product management: Modern LOS allows for configuring the lender's entire portfolio of credit products. Administrators may create new loan types, define their specific parameters, such as interest rates (fixed or variable), fee structures, repayment terms, and eligibility criteria, and scale these rules across different channels. This results in rapid product launches and precise targeting of customer segments.

Workflow configuration: This functionality allows lenders to create, customize, and scale the exact journey a loan application follows. Lenders can build workflows by defining rules for tasks like credit scoring, document collection, verification, approval, and funding. The result is a faster, more efficient process that reduces manual handling and shortens turnaround times.

Pricing and terms engine: The feature defines and assigns interest rates, fees, repayment schedules, and other loan conditions for each product. This allows for flexible pricing strategies based on risk and customer profile.

How to Choose the Best Loan Origination System?

The loan origination systems mentioned on our list differ in size, experience, scope of functionality, and pricing. Before plunging into any digital transformation, it is recommended to develop a roadmap that will navigate the choice of an appropriate solution.

- Determine the scope of need. Do you need a system for the entire mortgage process, or do you need to solve specific tasks, such as document generation or compliance?

- Develop a structured implementation roadmap. Establish a defined deployment plan with milestones. What are the owners, reasonable deadlines, specified dependencies, and quantifiable acceptance criteria at every phase?

- Choose the deployment model. Do you require easy accessibility and updates of a cloud-based platform, or does your enterprise have specific security and control requirements that demand on-premise servers?

- Consider the implementation time and customization capabilities. Do you need to reduce time-to-market and allow for easy tailoring without extensive developer resources? Low-code/no-code platforms might be a solution. Another option is implementing white-label tools that offer brands a seamless customer experience at a relatively low cost.

- Assess the scalability potential. Can the system grow with your loan volume and adapt to new products?

- Examine the integration possibilities. Does the new software connect with your existing systems (core banking, CRM, etc.)?

- Check the regulatory compliance and security measures. Does it have built-in compliance checks and robust data encryption to protect client data and eliminate breaches?

- Evaluate Total Cost of Ownership (TCO). What are direct costs (those for customization, third-party integrations, implementation services), recurring expenses (like hosting, maintenance, and support), and hidden costs (such as data migration, employee training, and any costs related to a postponed go-live)?

Here's the thing most vendors won't tell you: the "best" LOS isn't always the most feature-rich or the most expensive one. It's the one that actually fits how your team works.

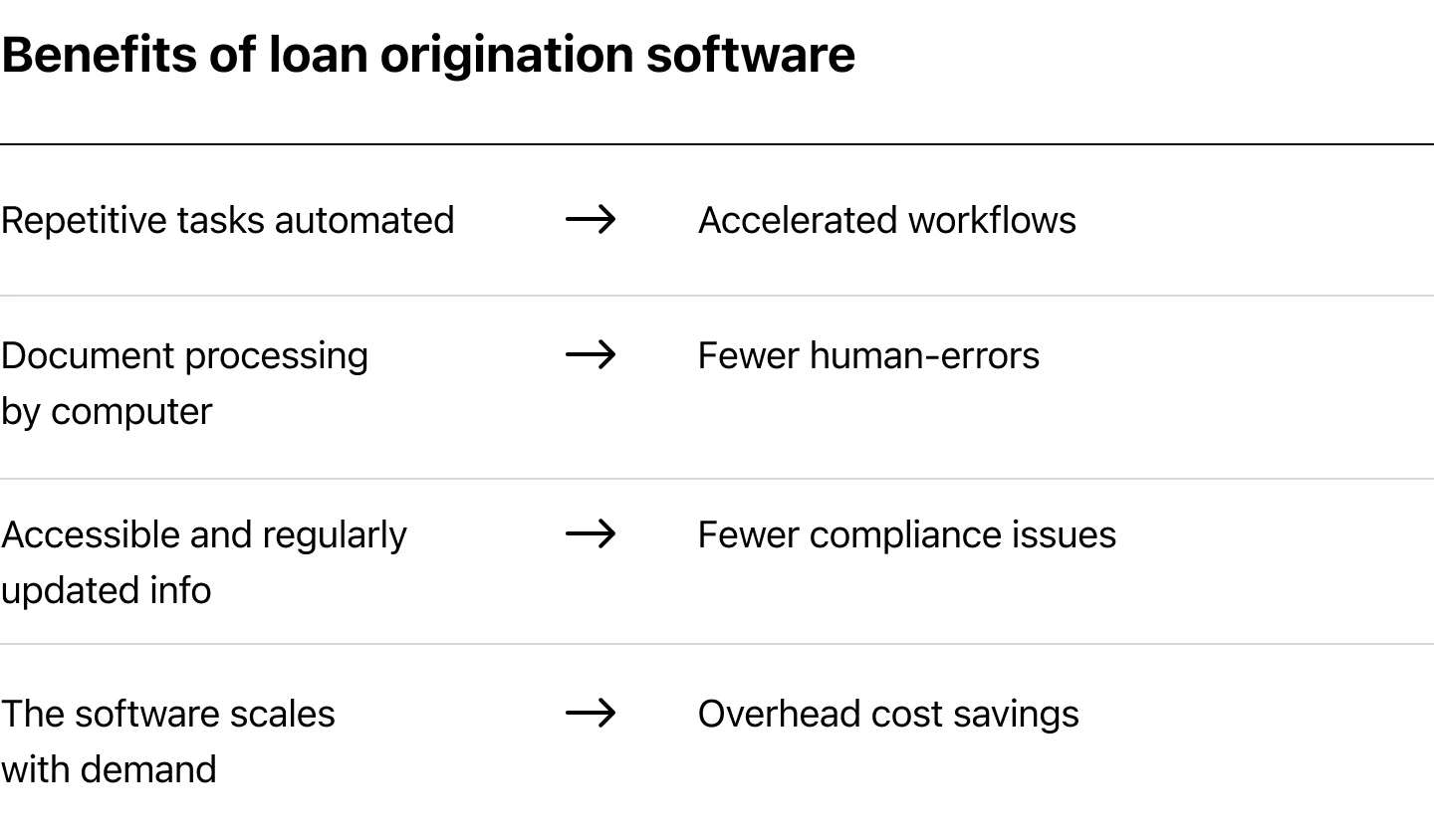

What Are the Key Benefits of Using Loan Origination Software?

Lenders that implement modern loan processing systems mention the following key improvements in their lending operations:

- Repetitive tasks are performed automatically, which results in accelerated workflows.

- A computer program deals with document processing, eliminating the human factor and reducing errors.

- All the information is easily accessible and regularly updated, which minimizes the risk of compliance issues.

- The software scales in accordance with the market demands, saving overhead costs.

How Do You Know It's the Best Loan Origination Platform for YOUR Company?

Run this quick test before making a decision:

The 30-day reality check.

Ask yourself: can your team realistically go live in 30-60-90 days? If the vendor is talking about 6-month implementations for a standard setup, that's a red flag. Modern platforms should get you up and running fast.

Now, let's be realistic here—if you're running a complex, multi-country operation with dozens of custom loan products and legacy system integrations, yes, you're looking at 6+ months of customization work. That's just the nature of enterprise complexity. But we're talking about standard lending needs here: basic loan origination, underwriting workflows, and servicing. For those core functions, a modern platform shouldn't need half a year to go live. If a vendor needs 6 months to set up a basic consumer lending flow, they're either over-engineering it or their platform isn't as flexible as they claim.

The Monday morning test. Imagine it's Monday. Your loan officer just got back from vacation and needs to process an application. If they need to open 5 different systems or call IT for help, the platform fails. Good LOS should feel intuitive, not like rocket science.

The growth test. You're processing 500 loans a month now. What happens when that becomes 5,000? Ask vendors point-blank: "What breaks first when volume spikes?" Their answer tells you everything about scalability.

The real cost test. Add up everything: licensing, implementation, training, maintenance, and those "small" customization fees that pop up later. Then divide by your monthly loan volume. If the math doesn't make sense, walk away.

The support test. Something breaks at 9 PM on a Friday (because of course it does). Can you actually reach someone who can help, or are you stuck until Monday? Test their support response during the sales process—it only gets worse after you sign.

The exit test. I know, you're just getting started. But ask anyway: "How easy is it to export our data if we leave?" If they get uncomfortable or vague, you're looking at vendor lock-in. Your data should always be portable.

Look, here's what I've seen work: Stop chasing features you'll never use. Instead, write down the 3 biggest pain points in your current process. Then ask each vendor: "Show me exactly how your platform solves THIS." If they start showing generic demos instead of addressing your specific problems, move on.

The right loan origination platform should feel like it was built for how you actually work, not how some product manager thought lending should work.

Conclusion

A fintech lender choosing the best loan origination software is like a head chef choosing a knife set. The right choice is an extension of their skill and directly determines the quality of their services. The wrong choice, however, leads to wasted effort, complicated processes, and ultimately, higher costs.

An appropriate LOS increases efficiency and ROI, saves operational time, and customizes workflows. The loan origination software comparison allows businesses to evaluate a diverse range of solutions, from full-scale, end-to-end platforms to customizable tools for specific tasks.

Key differentiators in 2026 include the rise of low-code customization, AI-powered underwriting, and the importance of seamless integration. By carefully assessing their specific needs against the features, pros, and cons of top providers, lenders can implement a system that not only streamlines operations but also drives growth, mitigates risk, and ensures long-term competitiveness in the financial landscape.

Looking for a configurable solution rather than a comparison? See how HES loan origination software handles the full origination cycle.