The negative impact of fraud can hardly be underestimated. The Association of Certified Fraud Examiners (CFE) shares that businesses worldwide may lose around $4 trillion yearly because of fraudulent activities. SMEs with up to 100 employees tend to be most vulnerable as they lack anti-fraud technologies and established policies.

The pandemic increased the risk of fraud: anonymized event statistics by Kaspersky Fraud Prevention revealed that from January to December 2020, the percentage of account takeover frauds grew from 34% in 2019 to 54% in 2020. In addition, the fraudsters’ behavior has also changed.

Financial Service Consumers are at Risk

As for the financial institutions, the older generation used to be the main target for fraudulent activities in the financial industry before the pandemic, while fraud among younger generations has grown 4x in 2020-2021. No doubt, fraud will be moving forward as the trend of using digital experiences across the entire demographics is expanding.

Experts see the increase of frauds targeting consumers and companies directly. Google noticed a skyrocketing number of phishing sites imitating legitimate sites of banks and financial institutions. Banks, credit unions, and alternative lenders work hard to protect their customers from fraud and pay attention to customer education about their financial safety.

But what about the risks for the financial institutions, namely?

Fraud-related Risks in Digital Banking & Digital Lending

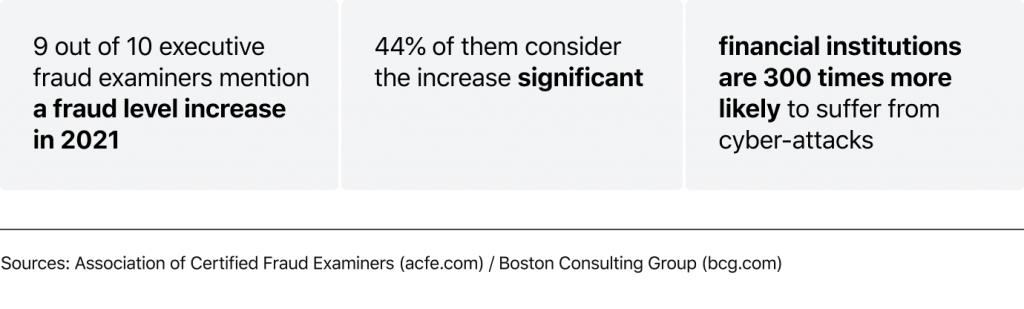

The banking and lending industry is 300 times more likely to face a cyber-attack than any other sector. Fraud is a significant risk factor for lost revenue in lending, and while the criminal schemes are becoming more sophisticated: the trend looks worrisome.

Why Does Fraud in Lending Need Attention?

The digital acceleration became the fertile ground for identity-based threats and fraud based on the digital system’s vulnerability. And it becomes a serious question: how lenders can estimate potential threats that endanger their financial and reputational success.

Fraud Detection and Prevention

With the current landscape and trends, what are the steps financial institutions need to take to detect and prevent fraud? According to the Financial Brand, the greatest challenge and the sweetest spot at the same time for banks and fintechs is a balance between well-planned risk management and customer experience.

One of the ways out is to update legacy software to make sure the resulting digital platform combines monitoring, prevention, recovery, and consulting features. For safer digital lending, banks and credit unions may consider AI-based tools that help institutions exchange information and allow secure and reliable KYC/AML, as well as credit scoring.

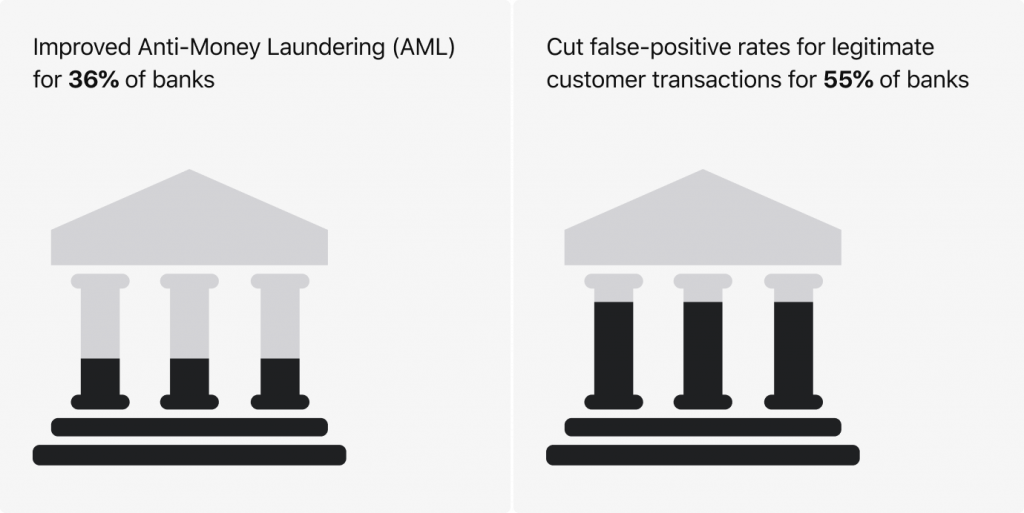

A study found that 35% of banks using AI said about improvements in their AML capabilities, while 55% agreed that their false-positive rates for legitimate customer transactions could be reduced with the help of AI:

Artificial Intelligence in Fraud Preventions

New Types of COVID-related Money Laundering Schemes

Financial service providers need to be prepared for new money laundering schemes that appeared during COVID-19, such as fraudulent action regarding medical or food supplies, bribes to officials that monitor movement of goods, business operations that are not complying with COVID-19 closure directives.

KYC and AML Processes or How Automation Improves Compliance in LendingThe advantage of AI software is its ability to quickly build protection from trending fraud types, helping banks, financial institutions, or their partners to remain proactive when identifying and combating fraud. Integration with credit bureaus, reliable KYC, and digital identity verification providers helps to connect the dots better than relying solely on their own authorization procedures.

Delinquency Management

In addition to that, financial organizations implement other risk management methods and tools, such as next-gen delinquency management software. Tech-empowered collection modules within the software product allow having a 360-degree view of this loan management aspect. To address the growing challenge of disputes, banks and fintechs can rely on third-party providers.

Customer Onboarding

Like with other social changes, consumer fraud is popular in lending. New government programs that appeared during the pandemic, such as the Small Business Administration (SBA) lending program in the U.S. and the Coronavirus Business Interruption Loan Scheme (CBILS) in the U.K. can be opportunities for fraudsters to apply for loans illegally.

Omnichannel customer onboarding in loan origination enables branded communication with the financial service provider (via text messages or emails), includes a tech-secured KYC/AML, and creates a safer digital lending environment in general.

For sure, digital lending will expand, and the major challenge for lenders is to pick the proper tools and technologies that allow them to stop fraudsters and, at the same time, to build trustful relationships with customers.

So, key takeaways for onboarding:

Make use of third-party data providers to collect and analyze the data required for a fast KYC. External and internal, structured and unstructured data help with onboarding, verification, and scoring and create the most accurate risk profile available via the digital channel.

Check out that the KYC is properly integrated with the compliance backend and case management functionality. The third-party data we mentioned above needs to be integrated into the activity dashboard so that employees could see the information in one place and could use it for their reports or onboarding process closeouts.

Banks and fintechs are seriously stressed these years, however investment in fraud detection and prevention can pay off in the future with higher agility and effectiveness. By accentuating security without interfering with the onboarding convenience, lenders successfully manage the fluctuating business conditions and navigate growth in the expanding digital economy.