The lending environment in 2026 requires lenders to manage risk across the full loan lifecycle, not only at approval. In the euro area, corporate borrowing costs have stopped declining steadily, while the EU AI Act timeline and the CFPB’s Section 1071 rule have both changed in 2026. Credit teams are also under pressure to manage increasingly complex portfolios without proportionate headcount growth.

In this article, we go over business lending strategies for 2026 that help reduce risk without slowing origination. Read on to stay informed!

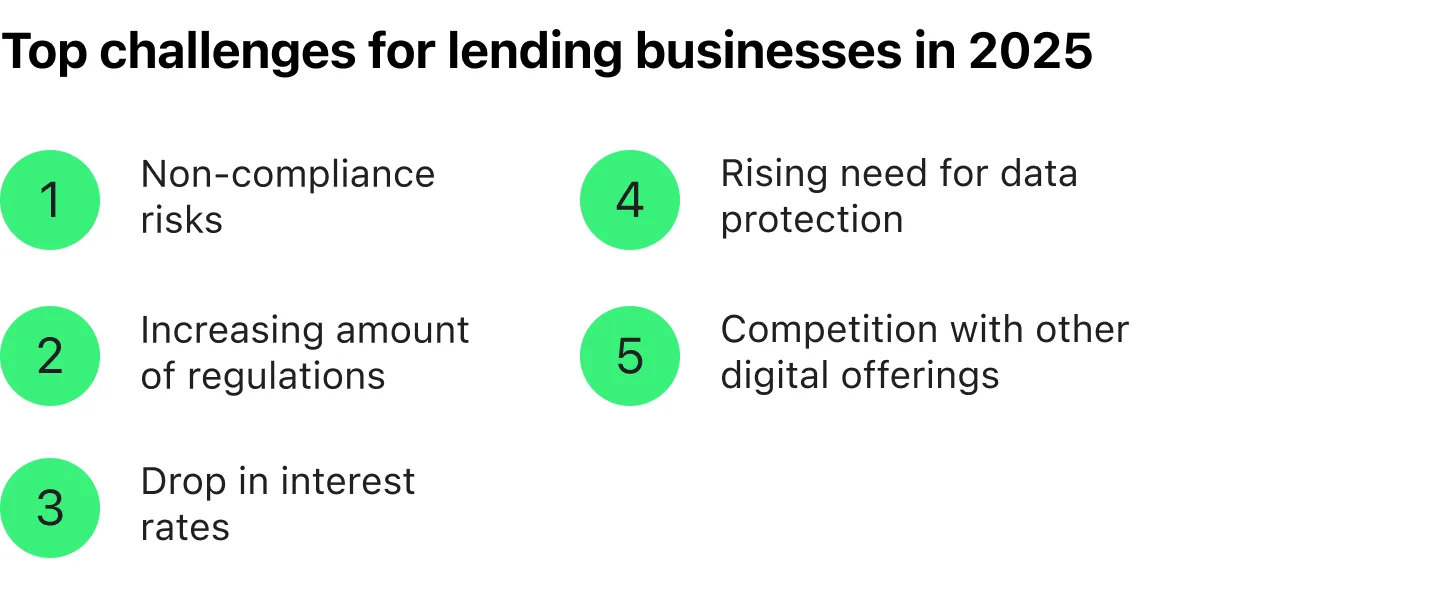

What Challenges and Changes Lending Business Owners Face Today

Running a lending business today comes with plenty of hurdles. With risks growing more complex and customer expectations higher than ever, staying competitive requires constant adjustment. Below, we highlight the most pressing challenges for lending business owners today.

High Risk of Non-Compliance with Modern Requirements

In recent years, almost all areas of human life have moved online, which has significantly affected business management. Today’s lenders have to work in constantly changing regulatory environments that include maintaining flexibility, transparency, product personalization, and data protection. Especially if a company utilizes artificial intelligence, the compliance of this domain is updated almost weekly, and credit teams have to follow it to avoid legal or reputational problems.

Adapting both systems to upgrades and regulations to existing laws at the same time can be very tough, but neglecting this procedure may lead to challenges in risk assessment, lending practices, and compliance.

Interest Rates That Stopped Falling

According to ECB bank interest rate statistics, the composite cost of borrowing on new loans to euro area corporations stood at 3.59% in March 2026, about 1.7 percentage points below its October 2023 peak. The indicator had edged up from 3.51% in February and then leveled off, so it is no longer falling in a straight line. Lenders can no longer assume borrowing costs will keep declining, which means pricing and affordability models should be tested against a more stable rate environment rather than a downward trend.

Shifting interest rates influence both lenders and borrowers. The first ones change their ambitions, while the second ones, the sum they can afford. Experienced lenders should know how to balance healthy margins with competitive interest rates.

Increasing Amount of Regulations

Modern lenders have to face vast amounts of regulations. For example, American lenders have to consider at least three serious social acts in their practice and implement improvements in staff training and systems according to them: Fair Credit Reporting Act (FCRA), the Truth in Lending Act (TILA), and Dodd-Frank Act).

Under the revised CFPB Section 1071 rule finalized on May 1, 2026, a financial institution that originated at least 1,000 covered credit transactions for small businesses in each of 2026 and 2027 must begin collecting the required Section 1071 data for covered applications on January 1, 2028. Its first annual filing would generally be due by June 1, 2029.

Additionally, the American government works a lot on AI compliance rules—Equal Employment Opportunity Commission, National Artificial Intelligence Initiative Act—to make AI development safe and fair.

Besides all these rules, modern lenders have to work with environmental, social, and governance (ESG) factors. Credit teams should assess a big list of risks and keep up with all new laws, which is why adding extra criteria may be problematic.

The Protection of Data from Hackers

Securely protected customer data is undoubtedly one of the key factors of a business's proficiency. The Global Security Outlook (GSO) survey shows that 72% of responders noticed the growth of cyberattacks because of new, AI-enhanced tactics, such as phishing, vishing and deepfake.

As hackers are constantly changing their strategies, and supporting robust security measures is getting harder and more important, lenders must constantly adapt to this process to protect their data at the highest level.

The Development of Online Service

The size and growth of the digital lending market is increasing worldwide, especially in the consumer borrowers segment, and is projected to expand at an annual rate of 18.2%. This mostly happens due to the spread of embedded lending inside SaaS platforms and AI-driven origination software that reduce decision time to minutes.

For lenders, it signals the necessity to be aware of all the latest digital trends and invest in technologies to offer a sufficient amount and variety of digital offerings. Otherwise, their business will become outdated and won’t attract new customers.

New Rules Taking Effect in 2026

Two regulatory timelines changed in 2026, and both matter for lending teams planning system upgrades.

In the EU, certain AI Act transparency requirements take effect on August 2, 2026. Providers of AI systems designed to interact directly with people must ensure those individuals are informed that they are interacting with AI, subject to specific exceptions. For lenders, this is most relevant to applicant-facing chatbots and AI assistants rather than every internal model used in the lending workflow.

Separately, the EU AI Omnibus received final Council approval on June 29, 2026, completing the legislative process. Once published in the Official Journal and in force, it will move the application date for stand-alone high-risk AI systems to December 2, 2027. This category includes AI intended to evaluate the creditworthiness of natural persons or establish their credit score, so it is most relevant to consumer and sole-trader lending. The requirements cover risk management, technical documentation, traceability, human oversight, accuracy, robustness, and cybersecurity controls.

In the US, the CFPB finalized its revised Section 1071 rule in May 2026. The threshold rose from 100 to 1,000 covered originations per year, the small business definition narrowed to companies with $1 million or less in annual gross revenue, and merchant cash advances dropped out of scope. The practical takeaway: institutions near the 1,000-transaction threshold should decide now whether their loan management systems can produce HMDA-grade reporting, because bolting it on close to the compliance date will be expensive.

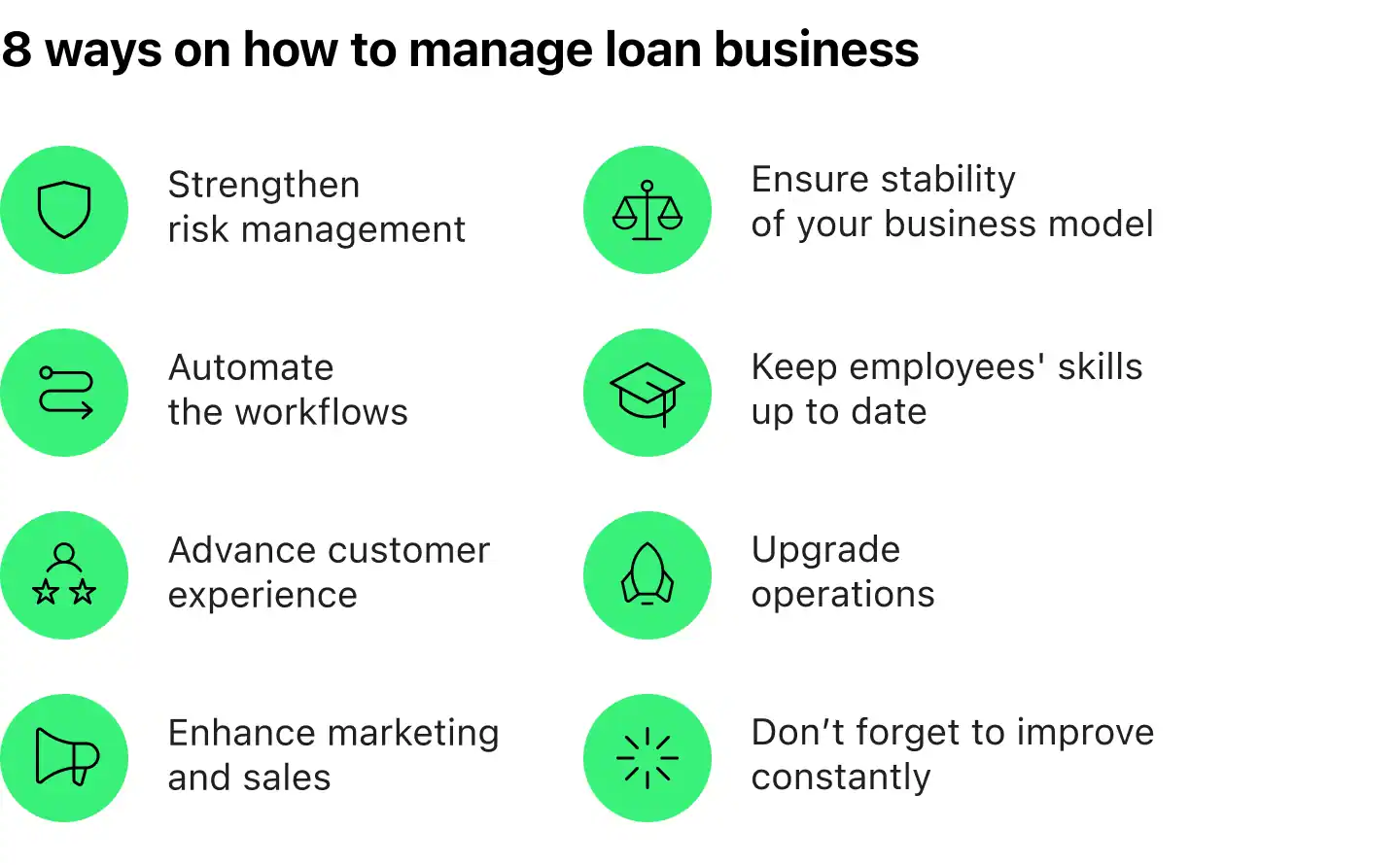

How to Manage Loan Business Effectively

Sometimes, credit teams are so swamped with their daily workflow that they don’t have enough time to consider how to add value to their lending relationships. However, by doing so, they can elaborate a strategy that will help them to make their business more profitable. Here are some lending tips for adding value.

1. Strengthen Risk Management

To ensure sound lending practices that enable informed decision-making and help mitigate potential risks, begin with an accurate assessment of the customer's creditworthiness. To create a more comprehensive risk profile, lenders need to rely on robust credit scoring models. Validating and cross-checking the module is part of the approach, ensuring the repayment risks are neither overestimated, nor underestimated.

2. Ensure Stability of Your Business Model

Diversifying the loan portfolio by avoiding overexposure to specific sectors or loan types further strengthens risk management. Safeguard against default can be provided by setting maximum loan limits based on a customer’s payment capability and the value of any collateral. Continuous monitoring of a client’s activity not only allows for noticing the first signs of financial distress but also enables timely support.

3. Automate the Workflows

Enhanced underwriting can improve consistency, decision speed, and risk management considerably. Automated loan origination can boost customer satisfaction and mitigate the risk of human error. Overall, digitalization allows lenders to use the time saved on routine tasks to create more complex and effective business strategies.

To get contemporary lending solutions to automate your business, consider working with FinTech vendors who already at the forefront of technologies and successfully implement them on a b2b basis.

4. Keep employees’ skills up to date

Make sure that your credit teams meet the requirements of the modern market. To do so, organize regular training on customer service and compliance best practices. Also, foster a strong customer service and ethical lending culture. These practices will help your business to stay effective and attract new clients.

5. Advance Customer Experience

To attract customers’ attention and loyalty with an advanced customer experience, consider adding a few practices:

- Provide an effective, user-friendly loan application process, making sure it’s easy to comprehend and contains minimal paperwork.

- Customize loan offers based on clients’ needs by scrutinizing their behavior and preferences with the use of data analytics.

- Use a variety of communication channels—calls, messaging, and emails—to provide customer support on a high level.

6. Upgrade Operations

Automate routine tasks such as document authentication, application processing, and loan approval to increase your business effectiveness and reduce errors.

Learn more about customer behavior, market dynamics, and repayment trends. This information will be useful in developing a mobile app or online portal for making payments or submitting loan applications. All these practices will eventually enhance customer experience and loyalty.

7. Enhance Marketing and Sales

To extend your customer base, encourage current clients to recommend your services to potential ones by leveraging referral programs. Also, target your marketing efforts on client groups that align best with the value of your financial products (for instance, flexible credit lines to seasonal retailers). A well-matched audience not only improves conversion but also helps reduce defaults.

8. Don’t Forget to Improve Constantly

Keep your customer experience at the top level by gathering user opinions. Also, constantly gather feedback about your lending processes, technology, and user satisfaction levels. Don’t forget that your lending strategy should always be based on your unique aims, business landscape, and customer needs.

All these lending tips are complementary and, applied step-by-step, can lead to impressive results in managing risk, increasing profits, boosting customer experience, and optimizing operations if you do them right and carefully check the performance metrics to see how well these advancements are working.

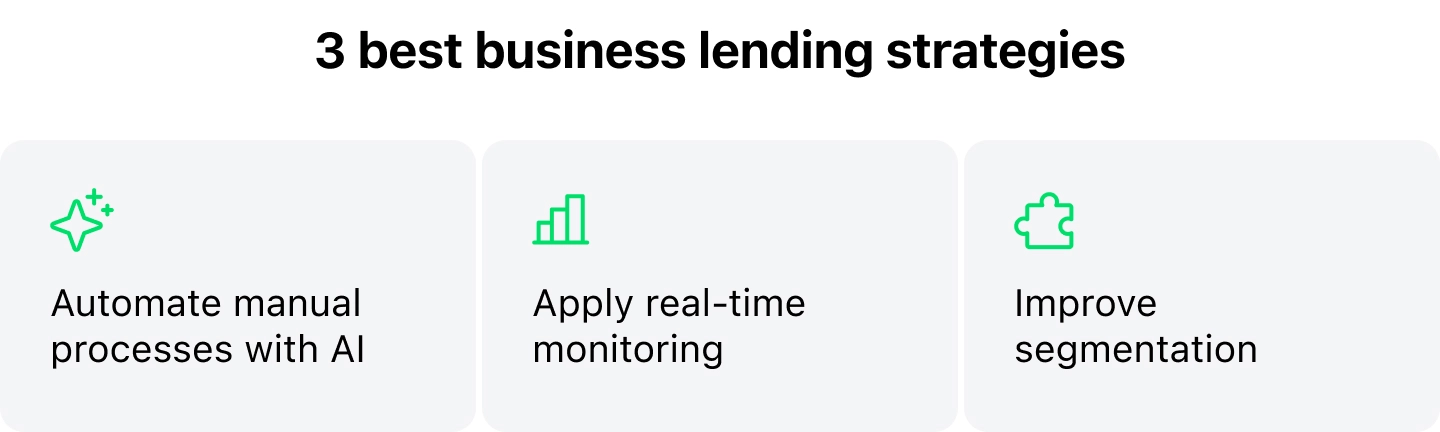

Best Business Lending Strategies

There are a lot of lending tips that can help business owners cut out the risks? Yet, the results can be even more impressive if you use the following business lending strategies:

Automate Manual Processes with AI

Manual loan processing may seem convenient, as it has been effective for decades. However, if your company still utilizes it, there is a high probability that it is slowing down your work process. There are a lot of reasons why switching to automated loan processing opens up new options for your business, but the biggest one is that it saves your most valuable resource—time. Manual loan processing requires considerable amounts of time. As a result, credit teams don’t have enough resources for making more informed decisions to improve their work.

What automation looks like in practice matters more than the label. The lenders who get the most out of it tend to consolidate the loan lifecycle, onboarding, origination, servicing, and collections, into one configurable environment instead of stitching together separate point tools, so risk and servicing data stay connected and manual handoffs drop. Platforms such as HES LoanBox are built around that model, with no-code workflows credit teams can adjust as policy and products change.

Apply Real-Time Monitoring

Traditional credit scoring methods are based on historical data. It means that a customer’s creditworthiness is checked only by their past payment behavior. In the modern market, this information is not enough, and it can be outdated, which leads to a higher risk of errors.

Also, this process is very time-consuming, as it is usually done manually. To mitigate risks and save time, it’s better to apply real-time monitoring to your workflow.

Portfolio monitoring models can combine recent cash-flow and behavioral signals with historical financial statements to flag changes that annual or quarterly data may not yet show. The actual improvement in prediction quality, alert timing, and fairness should be validated against the lender’s own portfolio and monitoring thresholds.

Improve Segmentation

A more accurate segmentation can also reduce loan processing risks, enabling businesses to make more informed, tailored decisions. It also helps to design loan products by matching them to the particular requirements and repayment capabilities of each group. Segmentation allows personalized interaction and collection efforts with customers. All these practices together improve business workflow, customer experience, and recovery rates.

Conclusion

Loan processing is a hard task that requires deep expertise and accuracy, as well as the seasoned specialists Still, this might not be enough to achieve good results. Today’s market is highly competitive and unstable, and that is why any business owner should have sound business lending strategies that will help cut out their risks.

You can significantly drop your risks if you decide to automate your routine tasks with AI, improve segmentation, and add real-time monitoring. These processes are interconnected, and together, these measures can not only mitigate risks but also give a significant rise to the overall business efficiency and customer service.

HES LoanBox supports automated origination, portfolio visibility, and collection workflows in one configurable platform. Book a demo, and we will map the platform to how your lending business works.