With the alternative lending market set to reach $1677.94 billion by 2035, more fintech teams are exploring how to start a lending business. The interest is easy to explain: demand for credit remains consistent across markets; there is still room to build something new, and modern infrastructure, including SaaS lending platforms, open banking, and capital marketplaces, has significantly lowered barriers to entry and accelerated go-to-market timelines.

At the same time, starting a money lending business comes with a very specific set of requirements. It involves navigating licensing frameworks, establishing robust KYC/KYB and AML processes, securing appropriate funding sources, and building the operational setup required to support the lending lifecycle end-to-end.

In this article, we’ll outline what it takes to start loan business in 2026, covering regulation, compliance, funding, technology, and core operational and risk requirements, to help you navigate the process end to end.

What Is a Lending Company and How Does It Operate?

A lending company is a financial entity that originates and services loans, with repayment scheduled over a defined period, usually including interest.

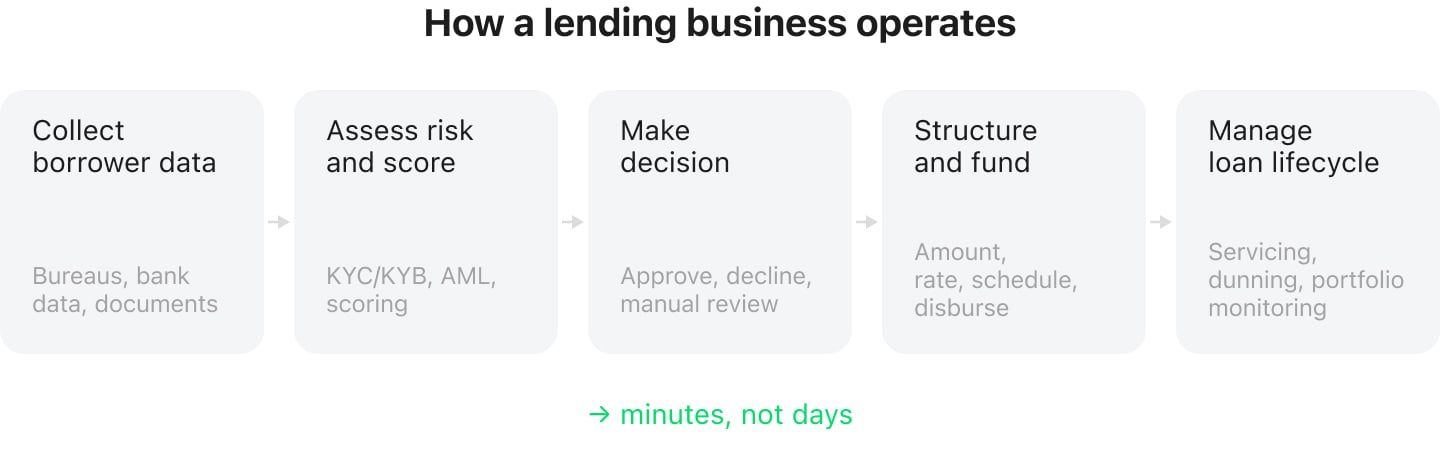

This business type follows a structured process that generally looks like this:

1. Collecting borrower data from multiple sources

Once a borrower submits an application, the company collects all the necessary information to understand who the borrower is and how they manage their money.

The lending business gathers data from credit bureaus, bank transaction history (where permitted and with borrower consent, often via open banking APIs), and documents provided directly by the borrower. After collection, this information is further processed and standardized so it can be used consistently across the system.

2. Assessing risk and borrower creditworthiness

At the next step, the company verifies the consistency of the data and checks it against internal policies and external requirements as well as conducts KYC / KYB and AML checks.

Then, the lender looks at income, cash flow stability, existing obligations, repayment history, and, where relevant, asset value and legal standing.

Many companies here leverage software that incorporates alternative data scoring and machine learning models to pick up signals that traditional credit checks might miss, especially when dealing with borrowers who have limited credit history.

3. Making the underwriting decision

All of this feeds into the final decision. Depending on the setup, the application may be approved, declined, or sent for manual review.

In more automated environments, a real time decisioning engine can handle this step almost instantly while still allowing human oversight when needed.

If approved, the process moves into structuring the loan, agreeing on the amount, interest rate, repayment schedule, and any collateral requirements and is then followed by documentation and disbursement of funds.

4. Managing the loan afterwards

Once a loan is disbursed, the focus shifts to ongoing servicing and portfolio monitoring, which includes tracking repayment schedules, interest and principal balances, and reconciling incoming payments to keep exposure accurately updated.

Within this step, lenders also manage borrower communication through automated reminders and structured dunning workflows to support timely repayments and reduce delinquency. If payments are delayed, accounts move into delinquency management, which can involve reminders, repayment rescheduling, or restructuring, depending on risk level and policy.

At the same time, lenders monitor portfolio health through key metrics such as delinquency and default rates, roll rates, and recoveries, which allows them to manage credit risk and overall portfolio performance.

What Types of Loans a Lending Business Can Offer

For teams evaluating how to start a lending company, one of the first strategic decisions they have to make is which loan types to offer and which segments to prioritize.

That decision is typically shaped by a combination of factors, including the target market, risk appetite, available capital, regulatory constraints, cost of capital, the chosen distribution model (direct vs. embedded), and the level of operational complexity that the business is prepared to manage.

Below are the most common lending segments, each with its own risk profile, operational requirements, and growth dynamics.

- Personal loans. These are the loans that individuals resort to when life throws expenses their way, like covering tuition, buying a car, or handling unexpected medical bills.

- Business loans. These loans include financing options such as working capital loans, project-based funding, and short-term solutions to manage cash flow gaps.

- Specialized and newer formats. Some lenders prefer to move beyond traditional products and explore more flexible structures such as installment-based payments for purchases, income-linked repayment models, or financing related to specific sectors like ESG or green finance lending.

Why Are Digital Lending Businesses Gaining Traction?

According to a report by Mordor Intelligence, several underlying trends have been driving the growth of digital lending and, as a result, prompting more companies to evaluate entry into this market and assess how to open a loan business that can scale and remain profitable over time.

Below, we’ll go through the main trends from the report and highlight a few additional ones that are equally important.

- Geographic expansion of mobile-first lending. Digital lending is seeing the strongest growth in regions such as Asia-Pacific and Africa, where mobile-first ecosystems and super-app platforms enable credit products to be embedded directly into everyday digital services and payment-driven user flows.

- Faster decision-making expectations. The spread of real-time underwriting has significantly shortened approval cycles, shifting user expectations and making slow credit decision processes obsolete.

- Improved access to financial data. Open banking/open finance frameworks (EU, UK, Australia), API-based data aggregation, and digital identity checks enable lenders to access richer financial data and assess borrowers more accurately based on actual financial behavior.

- Alternative-data credit scoring. Lenders now increasingly rely on digital data footprints, including behavioral patterns, transaction flows, and platform signals, to inform and enhance underwriting decisions.

- Growing demand from small businesses. A global $5.7 trillion SME funding gap and the need for rapid working-capital financing are driving the adoption of SME lending.

- Rise of embedded-finance lending. There is a shift from standalone SaaS lending platforms toward lending options that are directly embedded into user workflows via services and apps where credit becomes part of the product experience.

- AI-driven underwriting. Machine learning models are being increasingly used to refine risk assessment, automate credit decisioning, and improve portfolio performance through more granular and dynamic risk evaluation.

Another trend beyond the Mordor report that is noticeable is regulatory pressure on banks. Stricter capital and compliance requirements are limiting traditional banks’ flexibility, thus creating more room for neobanks and non-bank lenders. Amid high interest rates and tightened lending from traditional banks, the private credit market grew to nearly $2 trillion in AUM in 2024.

Why It’s Worth Starting a Loan Business

If you’ve been thinking about how to start a loan business online, you’re looking at a direction that can open up some tangible opportunities.

| Opportunity | What it means |

|---|---|

| Recurring revenue | Steady income from repayments, fees, renewals over time |

| Fast market entry | Ready-made loan software lets you start operations quickly |

| Flexible lending formats | Experiment with loan types and formats to match demand |

| Consistent demand | Loan demand stays steady—a resilient market to serve |

Let’s have a look at the most notable reasons and benefits.

1. Recurring Revenue Model

Revenue in lending is generated through interest, origination, and servicing fees that are tied to the lifecycle of each loan.

Once a borrower enters the system, the business creates a structured flow of repayments, potential renewals, and in some cases additional product offerings, which together form a continuous income stream over time.

However, it must be noted that this revenue structure is inherently risk-sensitive. Actual cash flows are highly dependent on portfolio performance dynamics, including portfolio risk, repayment volatility, delinquency behavior, non-performing loans (NPLs), default rates, prepayment patterns, and recovery outcomes. As a result, realized returns and the timing of cash inflows can materially deviate from initial expectations.

For this reason, maintaining revenue stability requires a strong credit risk framework, spanning underwriting precision, risk-based pricing, continuous portfolio monitoring, and effective collections and recovery processes.

2. Lower Entry Barriers Through Modular and Ready-to-Use Technology

If you’re figuring out how to start a loan company, you don’t necessarily need to build the entire lending infrastructure from scratch.

Today, a range of specialized platforms, including white-label loan management platforms such as HES LoanBox, cover most of the operational side of lending. These systems are built around an API-first approach, run on cloud-native architecture, and comply with standards like ISO 27001 / SOC2, which helps address security and compliance expectations.

What’s more, this software comes equipped with features such as configurable loan products, flexible servicing options, automated underwriting, and built-in scoring capabilities, while remaining customizable and scalable as the business grows.

Thanks to these built-in functionalities, you can focus on shaping your product and building relationships with borrowers, rather than spending months assembling core infrastructure from scratch.

3. Room for Portfolio and Risk Diversification

Lending today is no longer limited to a single rigid structure. In practice, it is a portfolio of loans made up of different formats that can be combined, adjusted, and rebalanced over time. This allows you to adapt without having to rebuild the business each time, gradually optimizing for what performs best under your market conditions and risk appetite.

For instance, you might start with BNPL or embedded financing and at the same time explore working capital loans for merchants. Some approaches might not deliver the results you expect, and that is part of the process, while others may prove more sustainable and worth scaling further.

4. Consistent Demand for Loans

Demand for loans is poised to grow. For example, the personal loans market alone is expected to grow by around $946.61 billion by 2030, which points to a continued need for accessible financing.

In periods when (or if) traditional banks tighten their approval criteria, alternative lenders may see an increase in applications, especially from borrowers who fall outside standard profiles or are underserved by conventional institutions.

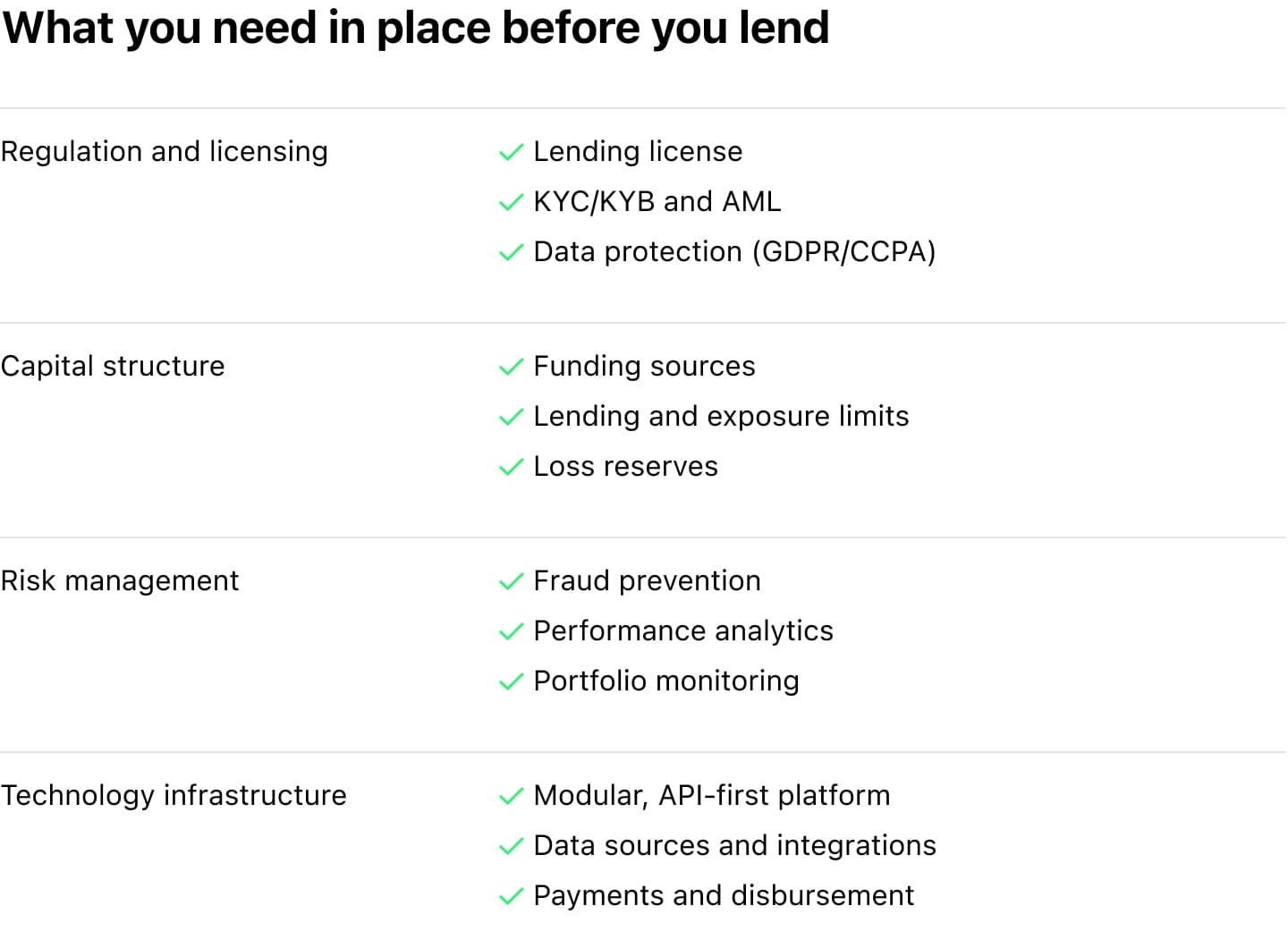

Key Lending Business Requirements to Consider

Before setting up a loan company, you have to get the core operational areas right, including regulation and licensing, capital structure, risk management, and technology infrastructure.

Let’s go through them.

1. Regulatory Setup and Licensing

To operate legally, you’ll need to obtain a lending license and understand the specific rules that apply in your jurisdiction, from how loans are issued to how interest and disclosures are handled.

As you’ll be working with sensitive financial and personal information, you need to establish compliance with data protection laws such as GDPR / CCPA (or other geographically specific regulations, depending on the region you are operating in).

If the loan management software that your lending business uses relies on AI, it’s also important for you to consider requirements introduced by the local jurisdiction, especially around transparency and risk classification (for example, the EU AI Act).

In some markets, like the UK, entering through a regulatory sandbox can be a practical way to test your model in a controlled environment before scaling.

2. Identity Verification and Compliance Processes

Before issuing any loan, you need to set up robust identity verification and compliance workflows to confirm your borrower’s identity and ensure that they meet regulatory standards. This usually involves integrating with reliable digital identity providers and setting up processes for KYC / KYB checks.

Done properly, it reduces fraud risk and builds a more consistent onboarding flow.

3. Access to Capital and Funding Structure

Some lenders start with their own funds, others rely on external sources such as a debt facility or investor backing. Regardless of the source, it’s important to define in advance how much capital is available, establish clear lending and exposure limits, and maintain sufficient reserves to cover potential losses.

Several other critical factors need to be taken into account, including cost of capital, liquidity management, loss provisioning, and underwriting limits. Together, they influence how quickly the business can scale, how much risk it can responsibly take on, and how resilient it remains when market conditions change.

4. Technology and System Architecture

The technology you choose will determine how efficiently your business can scale and adapt.

Modern lending platforms are built on modular, API-driven software that operates on cloud architecture, which makes it easier to scale, integrate new tools, or replace parts of the system without disrupting the entire operation. Choosing the right platform also impacts the speed of deployment, integration flexibility, and long-term maintainability.

5. Data Sources and Integrations

To assess borrowers properly, you need access to reliable and diverse data. This often means integrating with reliable credit bureaus and open banking aggregators (where available), which are used to assess borrowers’ financial behavior and possible delinquency risks.

6. Fraud Prevention and Security

Lending platforms are naturally exposed to fraud and misuse, so loan disbursement and repayment workflows must be traceable and resilient. Consider implementing fraud detection systems, such as velocity checks on application frequency, device fingerprinting to flag account takeover attempts, and behavioral biometrics to catch anomalies in how borrowers interact with the system. Complement these with encrypted data storage, role-based access controls, multi-factor authentication, and scheduled security audits to maintain a defensible perimeter as volume scales. Together, these controls reduce manual review overhead, keep repayment flows clean, and protect the borrower experience from interruption.

7. Payments and Operational Flow

Loan disbursement and repayment processes should work without friction, which usually means integrating stable payment gateways and setting up logic to handle delays, retries, and edge cases. Well-designed payment flows reduce operational overhead and improve the overall borrower experience.

8. Analytics and Performance Monitoring

To understand how your money lending business is doing, you need clear visibility into portfolio performance and unit economics.

Tracking key metrics like customer acquisition cost, portfolio performance, approval rates, and rates of non-performing loans will empower you to explore what contributes to business growth and where risks are building up.

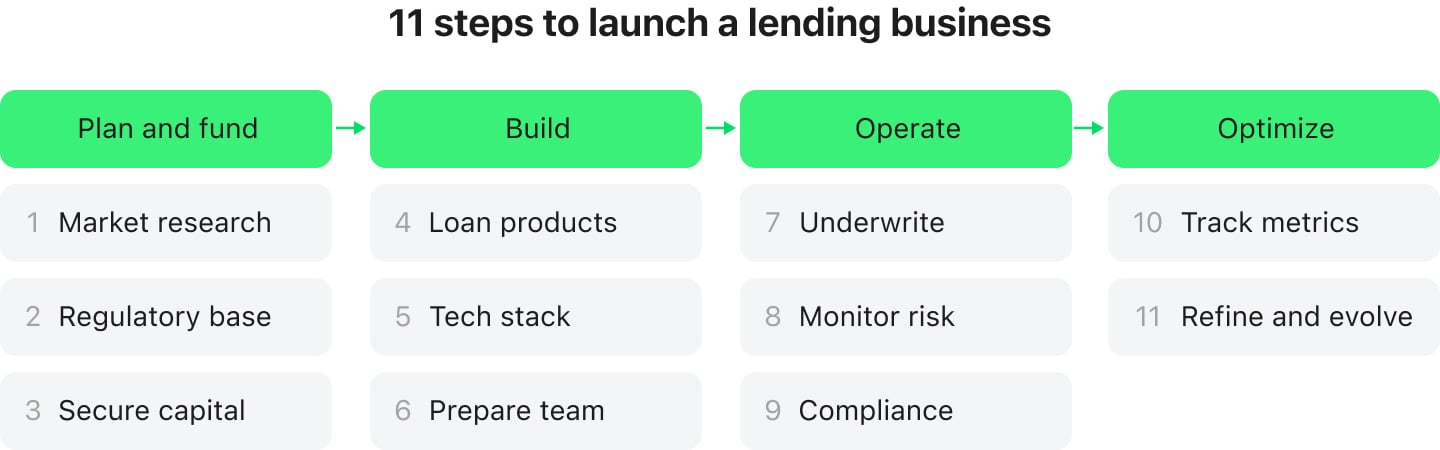

How to Start a Lending Business: Key Steps

The steps below are structured and action-oriented, taking you from early planning and setup through to the operational execution required to launch and run a lending business in 2026 and beyond.

- Conduct market research. Take the time to understand who your borrowers are, what problems they are trying to solve, and how existing lenders are serving them. The research might also help you guide your entire money lending business strategy and spot gaps or underserved niches that are worth focusing on from the outset.

- Establish the regulatory foundation. Incorporate a legal entity, obtain a lending license or the authorizations your model requires, and stand up the compliance framework you will operate under: KYC/KYB and AML controls and data protection measures aligned to the jurisdictions you serve.

- Secure capital and set your funding approach Confirm your funding sources, whether own balance sheet or external. Define exposure limits by borrower, segment, and product, and hold loss reserves sized to absorb expected defaults without destabilizing the business.

- Design your loan products. Set loan types, repayment structures, and pricing, and confirm each aligns with your target segment and risk tolerance.

- Build the technology stack. Deploy an API platform to process applications, approvals, and servicing; connect the data integrations that feed underwriting and verification; and enable payments for disbursement and collection.

- Prepare your team. Before scaling, ensure everyone involved understands the lending process, how risk is assessed, and how borrowers are handled consistently and responsibly.

- Onboard and underwrite borrowers. Run the KYC/KYB checks established in step 2, screen applications through fraud prevention, and assess creditworthiness with analytics-driven decisioning so every applicant passes through the same transparent review.

- Monitor and manage portfolio risk. Maintain a balanced portfolio, use collateral or guarantees where warranted, and track repayment behavior through portfolio monitoring so early-warning signals are not missed.

- Sustain compliance and transparency. Keep accurate records, produce regulatory reporting on schedule, and ensure operations remain compliant as the business grows.

- Track performance and key metrics. Analyze loan performance regularly and confirm the model is profitable and sustainable.

- Refine and evolve. Review results, improve processes, and adapt products as you learn what works and what does not.

Conclusion

Starting a lending company means solving several problems at once. The challenge here is how long it takes to build the right solution, which is a practical argument for starting with a platform rather than an assembly of point solutions.

HES LoanBox covers the operational spine described in the steps above: digital onboarding, loan origination, AI-driven credit decisioning, servicing, collections, and portfolio monitoring within a single, configurable system. It deploys in the cloud or on-premise to meet data residency requirements; includes built-in audit logs and compliance workflows; and connects via open API to the credit bureaus, payment providers, and KYC tools your underwriting process depends on. For most standard lending products, it's production-ready in three months.

If you start loan company and the operational build is your next decision, book a demo to see how our solution fits your lending model.