The best trade finance software provider can change the way businesses manage international trade as well as help them optimize cash flow, reduce operational risk, and accelerate transaction processing.

Modern and sophisticated trade finance software also offers automation of compliance workflows, real-time visibility into payments and receivables, and integration with banking systems and ERP platforms. Notably, investment in trade finance technology platforms reached $6.3 billion in 2024, which is a 17% increase year-on-year.

In this guide, we review 10 trade finance software platforms for 2026, organized into two categories that reflect how these solutions actually differ in scope, scale, and intended use.

The first group covers end-to-end trade finance platforms: enterprise solutions with validated market recognition and broad instrument coverage. The second covers segment-specific platforms: purpose-built tools for defined use cases, such as guarantee management, documentary trade processing, or trade finance lending, where precision matters more than breadth.

The platforms in this guide were selected based on publicly available market data, vendor documentation, analyst assessments, and verified product capabilities as of 2026. Inclusion does not constitute an endorsement. Readers are encouraged to conduct their own due diligence based on their institution's specific requirements.

What Is Trade Finance Software?

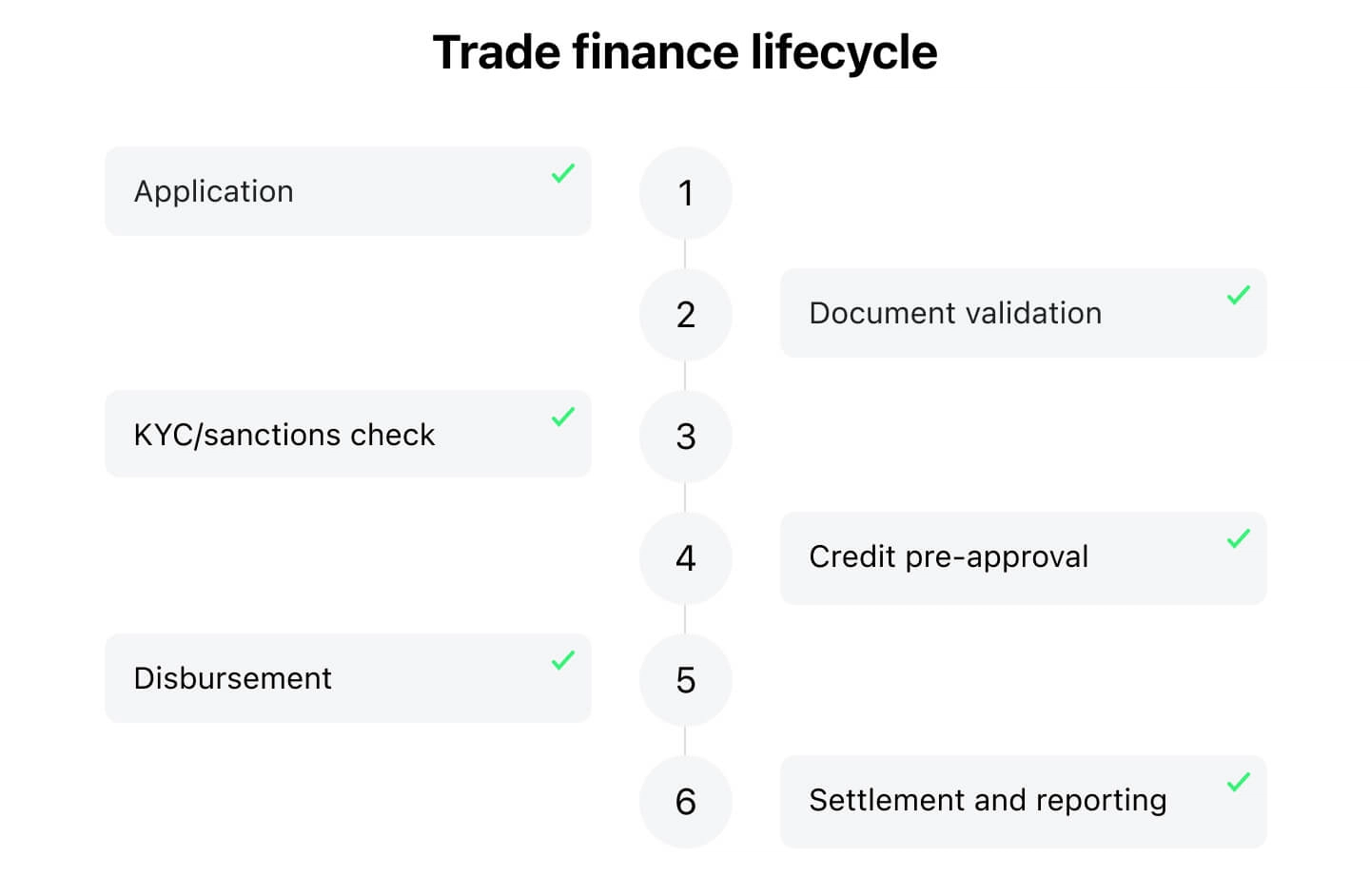

Trade finance software is a specialized platform that helps banks, financial institutions, and global businesses manage the full lifecycle of international trade transactions.

The trade finance platforms do not belong in a single category. Some platforms are designed to manage the full lifecycle of trade finance operations—from documentary credits and guarantees through compliance, risk distribution, and settlement—across large institutions, multiple jurisdictions, and high transaction volumes. These are selected through structured procurement processes by tier-1 banks, global corporates, and institutions managing complex, multi-product trade portfolios.

Other platforms are purpose-built for a specific segment of the trade finance ecosystem: guarantee management for corporate treasury teams, documentary trade processing for regional banks, or supply chain liquidity for specific industries. They do their defined job well, but their scope, client base, and architecture are not designed for enterprise-wide deployment across a full-service trade finance operation.

The most advanced trade finance systems are capable of simplifying complex and document-heavy workflows by automatically retrieving client and transaction data, validating trade documents, performing KYC and sanctions checks, routing tasks to the appropriate teams, executing pre-approvals based on credit rules, and handling disbursements and payments.

What Benefits Can the Best Trade Finance Software Bring to Businesses?

The right platform reduces the operational drag that slows international trade down — and builds the controls that keep it compliant.

Specifically, it delivers:

- Faster transaction cycle: Automated document checks and standardized workflows reduce the back-and-forth that usually slows down letters of credit, guarantees, and other trade instruments, thus improving cash flow.

- Stronger risk control: Real-time monitoring and built-in safeguards help companies catch discrepancies, non-compliant documents, or unusual activity before they escalate.

- Leaner and more efficient operations: By removing repetitive manual tasks, teams are able to zero in on more important duties and dedicate more time and attention to strengthening customer and partner relationships.

- Full visibility across deals: Up-to-date information on documents, payments, and shipment stages makes it easier to coordinate with banks, partners, and counterparties, as well as internal teams.

- Consistent regulatory compliance: Embedded rules and automated validation help organizations better comply with global and local regulatory standards without relying solely on manual oversight.

- More informed decision-making: With clearer insights into receivables, payment timelines, and financing needs, companies can make more informed and accurate decisions as to when to release cash, how much financing to secure, which transactions to prioritize, and how to optimize their working capital cycle.

How We Selected the Best Trade Finance Software Providers

This comparison was compiled through independent research conducted in 2026, drawing on vendor documentation, product pages, analyst assessments, client case studies, and publicly available market data. The goal is not to rank platforms by a single metric but to give decision-makers at banks, financial institutions, and large corporates a structured way to evaluate which solution fits their operational reality.

We have evaluated all vendors using consistent criteria:

- Instrument coverage—what trade finance products the platform supports end-to-end (LCs, guarantees, collections, supply chain finance, etc.)

- Workflow automation and straight-through processing—the degree to which the platform reduces manual intervention across document handling, approvals, and compliance checks

- Integration depth—connectivity with core banking systems, ERP platforms, KYC/AML engines, SWIFT/EBICS, and open APIs

- Deployment flexibility—support for cloud, on-premise, or hybrid environments to accommodate varying regulatory and IT requirements

- Scalability and configurability—ability to handle multi-entity, multi-currency, and multi-jurisdiction operations, and to adapt to new products or regulatory changes without re-platforming

- Compliance posture—built-in support for AML/CFT, sanctions screening, ICC rules, and jurisdiction-specific frameworks

- Market validation—evidence of real-world adoption, independent analyst recognition, or verifiable client scale

Segment-Specific Trade Finance Platforms

Segment-specific platforms are solutions built for a defined use case, client segment, or instrument type. They may be the right choice for an organization whose trade finance requirements fall within that scope—regional banks running documentary trade, corporate treasury teams managing guarantees, or lenders looking to add trade finance as one product line within a broader lending platform. Their value is precision, not breadth.

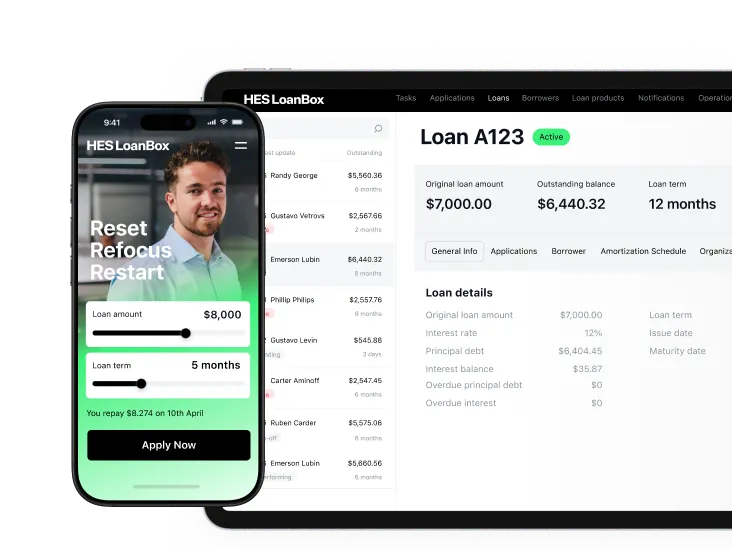

HES FinTech: Lending Platform with Trade Finance Financing Capabilities

HES FinTech is a configurable lending platform designed for banks, alternative lenders, and financial institutions that need to digitize and automate financing operations across multiple product types. Within its trade finance offering, the platform focuses on the financing layer of trade: invoice financing, supply chain lending, working capital facilities, and factoring—products where credit decisioning, borrower onboarding, and loan lifecycle management are the core operational requirements.

The platform is built on a modular architecture with deployment options across cloud and on-premise environments. It supports configurable credit policies, automated pre-approval workflows, and AI-assisted scoring to help lenders manage risk across high-volume financing portfolios. Integration with credit bureaus, open banking frameworks, and fraud prevention services is available through its API layer.

Recognized among G2's Top 25 Best Financial Services Software Products in 2026, ISO 27001 certified, and SOC 2 compliant, HES FinTech is best evaluated by banks and alternative lenders looking to add structured trade finance lending products (particularly invoice financing and supply chain credit), rather than by institutions managing documentary trade instruments such as letters of credit, bank guarantees, or documentary collections at scale.

Key features:

- Core product types: invoice financing, supply chain lending, working capital facilities, and factoring

- Configurable loan and financing product engine with customizable interest rates, repayment schedules, and product terms

- AI-assisted credit scoring with automated pre-approval workflows and configurable decisioning rules

- Borrower onboarding with integrated KYC/AML verification via third-party providers

- Full lending lifecycle coverage: origination → underwriting → servicing → collections

- Role-based dashboards with customizable reporting on portfolio quality, non-performing loans, revenue, and financing volumes

- 100+ API integrations with credit bureaus, open banking platforms, fraud prevention services, and payment rails

- Modular architecture supporting cloud and on-premise deployment

- ISO 27001 certified; SOC 2 compliant

- Multi-currency and multi-jurisdiction support

Overall user rating: 4.9/5 on Capterra; 4.8/5 on G2

Pricing: starts from $39K/year, depending on business type (a fixed subscription model with no limits on users, products, or applications).

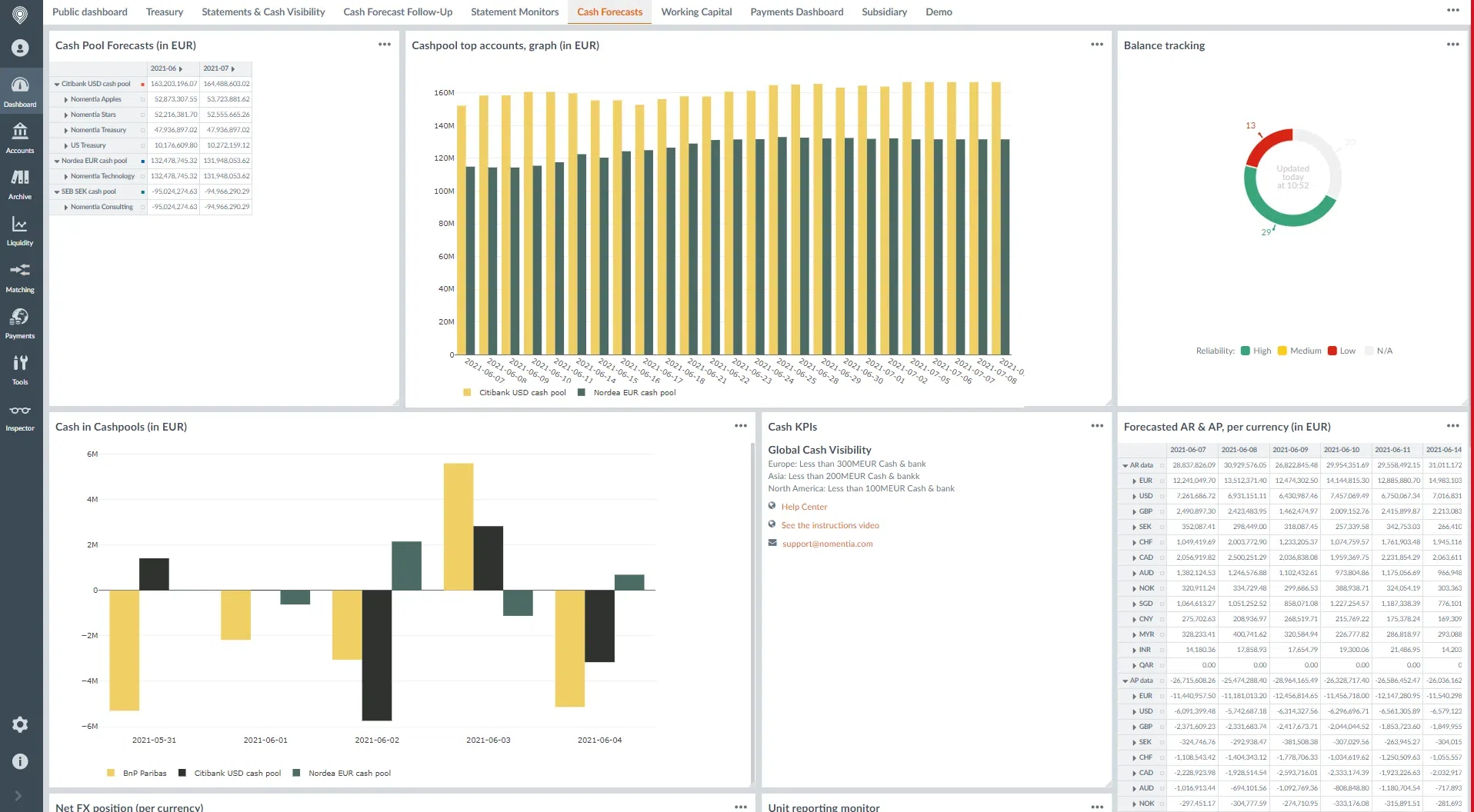

Nomentia: Treasury Management with Integrated Guarantee and LC Control

Nomentia’s platform is focused on guarantee management and letter of credit administration for corporates, all while centralizing all group-wide guarantees, LCs, and related instruments under one system.

Through a unified interface, users can request, amend, or return guarantees, track their status, and follow each instrument’s lifecycle. The platform digitizes information exchange between corporates and banks, using SWIFT-standard formats for communication, and supports H2H and EBICS protocols.

In addition, Nomentia supports configurable user and entity-based permissions and maintains a full audit trail. With this capability, users have visibility into guarantee histories, modifications, attachments, and status changes.

The platform also offers reporting and fee management capabilities. With them, corporates can generate reports, filter guarantees by multiple criteria such as type, beneficiary, due date, or currency, analyze fees and commissions, and combine this data with internal billing or settlement workflows.

Connectivity with external systems is part of the offering, too. Nomentia supports integration with ERP systems, treasury management systems, and major enterprise platforms like SAP R/3 and S4HANA.

Key features:

- End-to-end guarantee and LC lifecycle management (requesting, amending, returning, tracking status, and expiry management in a single platform)

- Bank communication digitized using SWIFT standard formats; H2H and EBICS connectivity; eliminates email-based guarantee management

- Trade limit monitoring by bank, facility, and counterparty

- Role- and entity-based permissions and audit trailRole- and entity-based permissions with full audit trail and timestamp logging for all actions, modifications, and status changes

- Automated internal billing and settlement integration

- Comprehensive fee reporting (filter guarantees by type, beneficiary, due date, guarantor, counterparty, or currency), analyze bank fees and identify overcharges

- SO 27001 and ISAE 3402 Type 2 certified

Overall user rating: There is only 1 review available on Capterra with a 5 grade.

Pricing: Modular pricing (payment per module selected); pricing is not disclosed publicly.

Comarch: Front-End Trade Finance Digitization for Regional Banks

Comarch Trade Finance is a front-end platform for banks and financial institutions that enables full digitization and automation of trade finance processes, right from application to settlement. It supports core trade finance products such as letters of credit, guarantees, and collections, enabling clients to apply for and manage these instruments entirely online. Moreover, built on a modular architecture, Comarch Trade Finance allows incremental rollout, meaning that a bank can start with a subset of trade products and gradually expand its digital offerings.

The platform supports full life-cycle management of trade finance processes, including product initiation (apply), amendments, processing, and closure. Noteworthy is that banks can also build their own product application forms and workflows depending on their specific needs.

For bank clients, Comarch also offers transparent status tracking. Thanks to this capability, users can see the full history of actions (who applied, when, who modified, who authorized) and check the status of their requests online.

The system is also compliant with relevant trade finance and messaging standards like ICC, helping banks integrate trade finance into their broader corporate banking stack while ensuring regulatory and operational compliance.

Key features:

- Online application and management of letters of credit, guarantees, and collections — entirely through a digital front-end without paper-based processes

- Full lifecycle management from product initiation and application through amendments, processing, and closure

- Modular architecture within the Comarch Corporate Banking suite, allowing trade finance to be deployed alongside cash management, loan origination, and factoring modules

- Customizable product application forms and approval workflows tailored to each bank's internal processes

- ICC rules compliance for documentary credits, collections, and guarantees

- DORA-compliant security and data management architecture

Overall user rating: no verified ratings available.

Pricing: Pricing is not disclosed publicly.

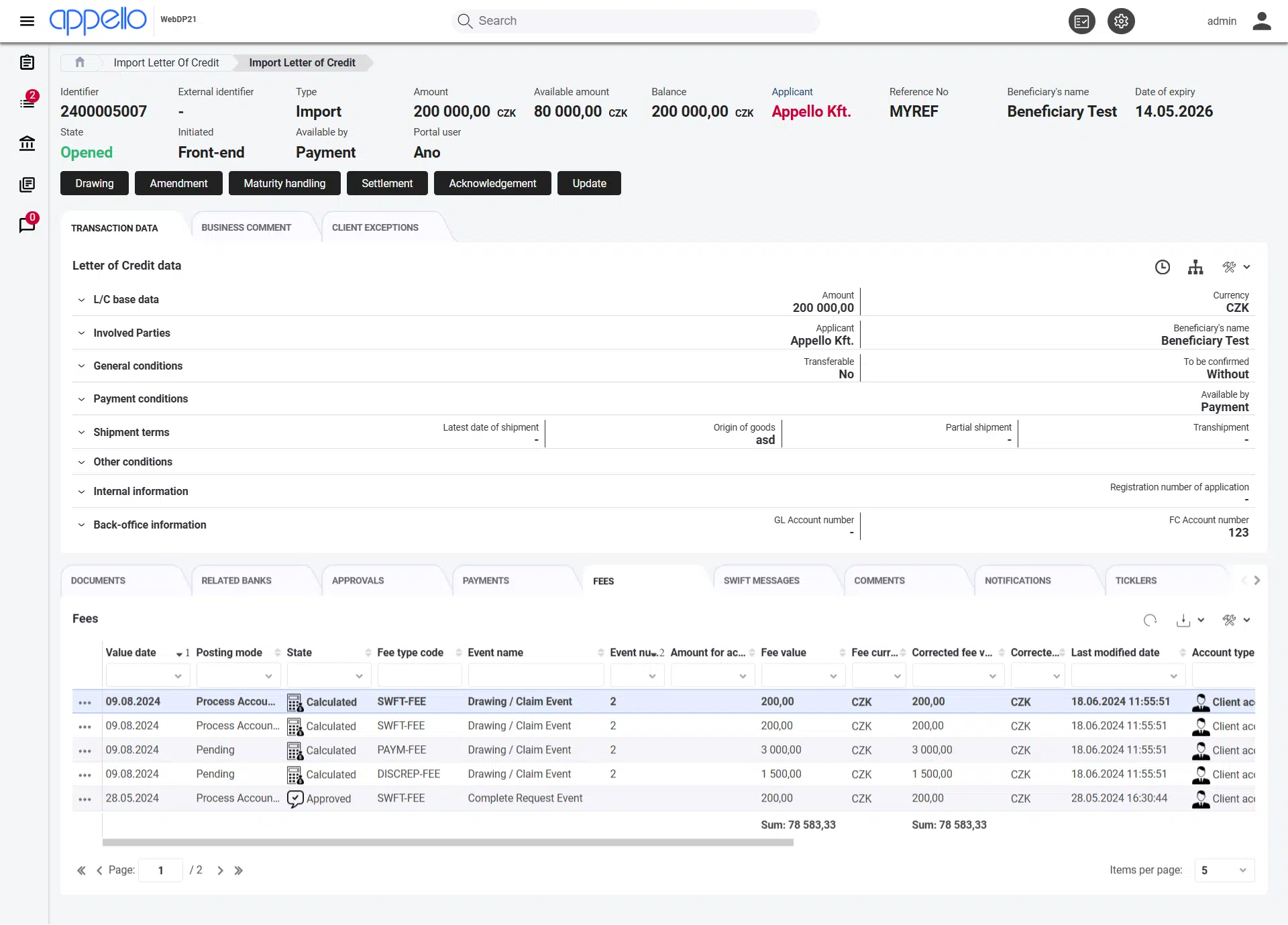

ApPello: Documentary Trade Processing Engine for Back-Office Operations

ApPello Trade Finance System is a configurable and low-code platform that helps better manage documentary trade finance processes in import and export operations. The solution supports core trade finance products such as letters of credit, bank guarantees, documentary collections, standby LCs, and their various subtypes, including features such as LC confirmation, transfers, shared guarantees, and counter-guarantees.

ApPello provides workflow-driven processing. Once a transaction is initiated, the system guides it through all required stages, including issuance, amendments, confirmations, collections, and settlements, applying the correct rules and message flows depending on document type, product type, or transaction nature.

What’s more, in ApPello, document and report generation is template-based. This means that users can create advice letters, reports, or other trade finance documents using templates and export or archive them in XLS or PDF format.

Importantly, ApPello includes a flexible fee module that allows institutions to define fee schedules based on transaction values or workflow parameters, giving banks or finance providers the ability to customize pricing strategies to their trade finance offerings.

Key features:

- Full processing of letters of credit, bank guarantees, standby LCs, and documentary collections including LC confirmation, transfer, shared guarantees, and counter-guarantees

- Workflow-driven transaction processing guiding each instrument through issuance, amendments, confirmations, collections, and settlement with correct rules applied per document type, product type, and transaction nature

- Built-in SWIFT engine fully automating messaging for LCs, guarantees, and collections

- Flexible fee module allowing institutions to define fee schedules based on transaction values or workflow parameters, with individual client pricelists and fee accrual for long-term transactions

- Customer portal for corporate clients to manage and track their trade finance instruments

Overall user rating: no verified ratings available.

Pricing: No pricing disclosed publicly.

Seabury TFX: Supply Chain Liquidity and Structured Trade Financing

Seabury TFX offers trade finance solutions that are primarily focused on supply chain operations. Specifically, its fintech platform called RAMP helps businesses improve cash flow, lower operational costs, and navigate trade finance with more dynamism.

Seabury TFX’s platform acts as a central data hub. It collects information from across the global trade network, including historical sales, shipping schedules, and payment records, and uses this aggregated data to deliver analytics, credit assessment, and customized financing solutions.

The platform also supports structured financing via a multi-stage funding approach: pre-shipment, in-transit, and post-shipment funding, thus giving suppliers and buyers flexibility to access liquidity at different stages of the transaction lifecycle.

What’s more, another Seabury’s solution called TrakFin helps digital businesses, including app developers and advertising companies, accelerate cash flow by providing faster access to revenues, dynamic credit lines, and streamlined onboarding. The platform makes use of multiple data sources to optimize accounts receivables and enables smarter financial management and quicker access to capital.

Key features:

- Central data hub for aggregating historical sales, shipping schedules, payment records, and supply chain performance data

- Multi-stage funding model: pre-shipment, in-transit, and post-shipment financing

- Proprietary credit and risk assessment tools incorporating both traditional credit data and alternative supply chain performance data

- Cloud-based platform providing a 24/7 transparent view of financing positions and transaction status

- Supply chain platform integration capability for connecting existing supplier–buyer ecosystems

- Accounts receivable optimization using multiple data sources for smarter financial management

Overall user rating: no verified ratings available.

Pricing: No pricing disclosed publicly.

End-to-End Trade Finance Platforms

End-to-end trade finance platforms are solutions with validated enterprise scale, broad instrument coverage, and independent market recognition. They are consistently cited by industry analysts—including IDC, Euromoney, and Aite Group—and serve large banks and global corporates managing high volumes across multiple jurisdictions and product lines. These platforms are evaluated when the requirement is to run a full-service trade finance operation, not to address a single workflow.

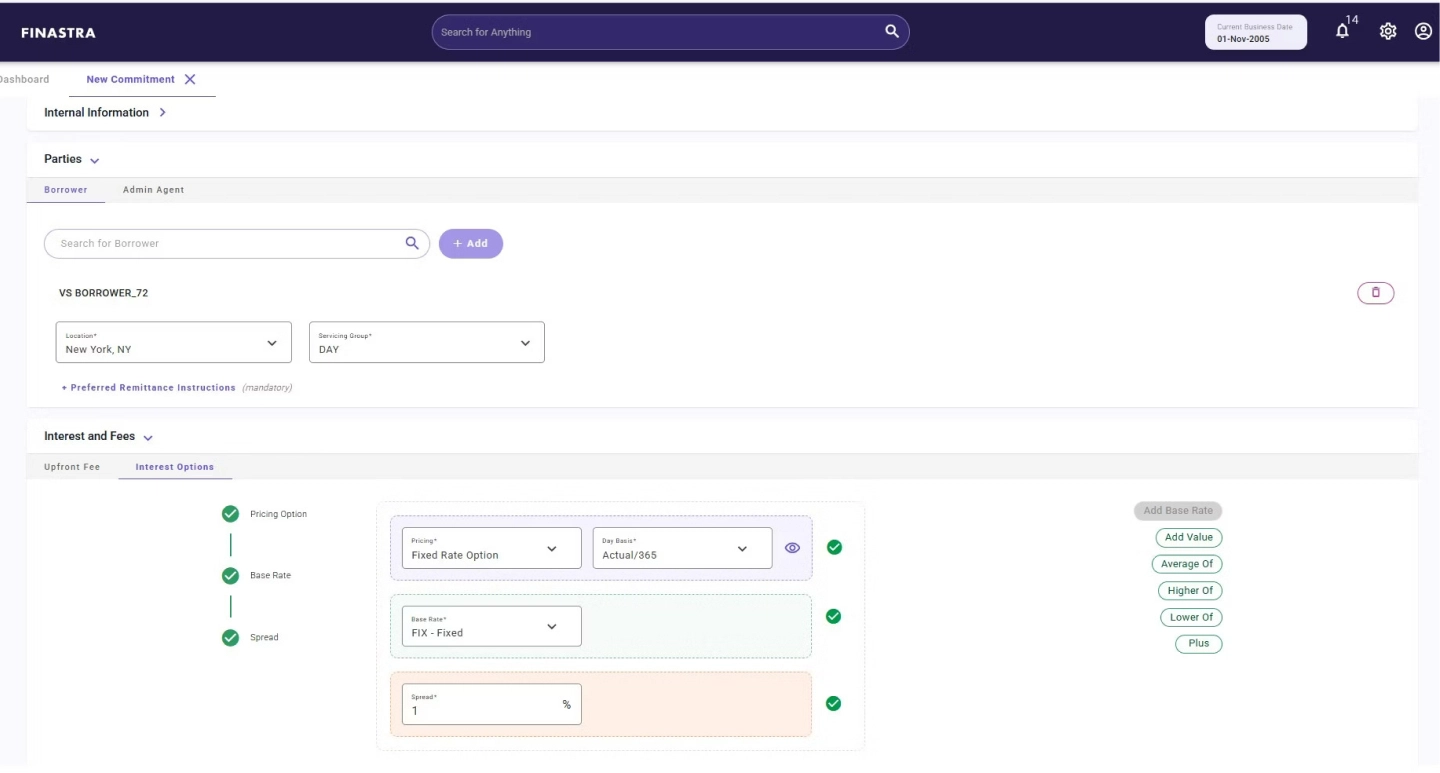

Finastra: Full-Lifecycle Trade Finance for Global Banks

Finastra is a front-to-back trade and supply chain finance platform that enables banks and financial institutions to manage the full lifecycle of trade and working capital finance instruments within one unified system. The solution supports a broad range of trade capabilities, including buyer and seller loans, letters of credit, collections, and supply chain finance.

A core element of Finastra is its Assist.AI, an AI-powered assistant built on Microsoft Azure and the capabilities of Microsoft Copilot. It provides prompt-based guidance and lets users query trade finance processes or rules and receive context-aware answers.

Trade Innovation supports end-to-end digital trade finance operations through straight-through processing, automated workflows, compliance screening, and digital document management. The platform enables the use of electronic bills of lading (eBLs) and other digital trade instruments while facilitating seamless collaboration between banks, corporates, and trade ecosystem participants.

On top of this, Trade Innovation by Finastra strengthens risk management through real-time integration with credit limit systems, flexible limit structure configuration, and a Risk Distribution module that supports both funded and unfunded distribution across trade and supply chain finance assets.

Moreover, thanks to its microservices architecture hosted on Microsoft Azure and open-API model, the solution boasts a high degree of scalability and can integrate with various external services and fintech partners.

Key features:

- Front-to-back processing of letters of credit, standby LCs, guarantees, documentary collections, buyer and seller loans, and supply chain finance

- AI-powered operational assistant (Assist.AI), providing secure real-time support across documentation, compliance, and transaction workflows

- Risk Distribution module supporting funded and unfunded distribution across trade and supply chain finance assets

- Automated compliance screening and document validation workflows

- Configurable dashboards, role-based reporting, and real-time transaction and exposure visibility

- Cloud-based, API-driven, and scalable infrastructure

Overall user rating: 4.1/5 (on Gartner).

Pricing: Enterprise negotiated contract.

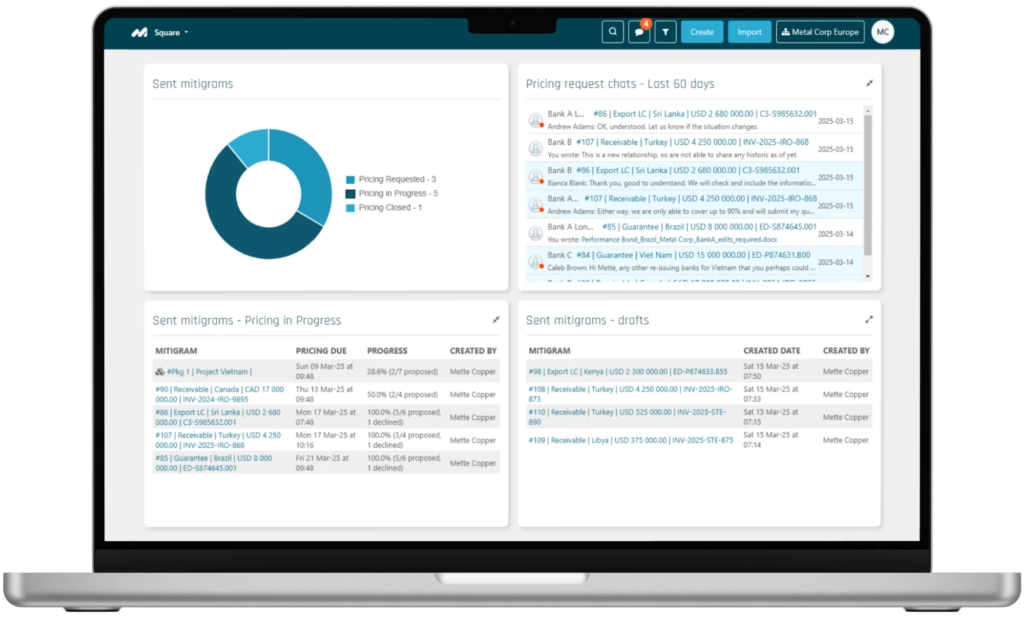

Mitigram: Trade Finance Risk Distribution and Market Intelligence Platform

Mitigram provides a suite of tools that make it possible to manage export and import LCs, bank guarantees, SBLCs, and receivables in one platform, covering the full lifecycle from planning and applications to amendments, document presentation, discrepancy resolution, and payment reconciliation. Plus, it leverages AI-powered OCR and machine learning algorithms to interpret and structure trade data.

For banks and financial institutions, Mitigram provides streamlined, API-based connectivity with counterparties across multiple channels, including web portals, email, SWIFT, EBICS, or other partner systems, thereby allowing secure and compliant trade finance operations globally, even when the connected banks do not directly use the Mitigram platform.

Besides, Mitigram provides data-driven risk and market intelligence. With over a decade of historical market data such as LC confirmation pricing trends, bank appetite and capacity by country, counterparty response patterns, and other benchmarkable transaction insights, institutions can benchmark their performance, analyze pricing and risk trends, and make informed decisions when entering new markets or structuring trade finance deals.

Finally, Mitigram integrates industry-standard MIS tools directly within the platform, which enables the creation of fully customizable reports while enriching clients’ internal data with industry benchmarks for in-depth analysis and performance comparison.

Key features:

- End-to-end management of export and import LCs, bank guarantees, SBLCs, and receivables

- AI-powered OCR and machine learning for automated interpretation and structuring of trade documents

- Centralized transaction and pricing management

- DORA and ISO 27001 compliance; SWIFT Compatible Application Trade Finance for Corporates certification

- Multi-channel bank connectivity: SWIFT, EBICS, API, web portal

- Centralized RFQ management with drag-and-drop transaction creation and multi-bank quote comparison in a single view

- Benchmarkable transaction analytics enabling performance comparison against industry data

Overall user rating: no verified ratings available.

Pricing: Custom quote per organization.

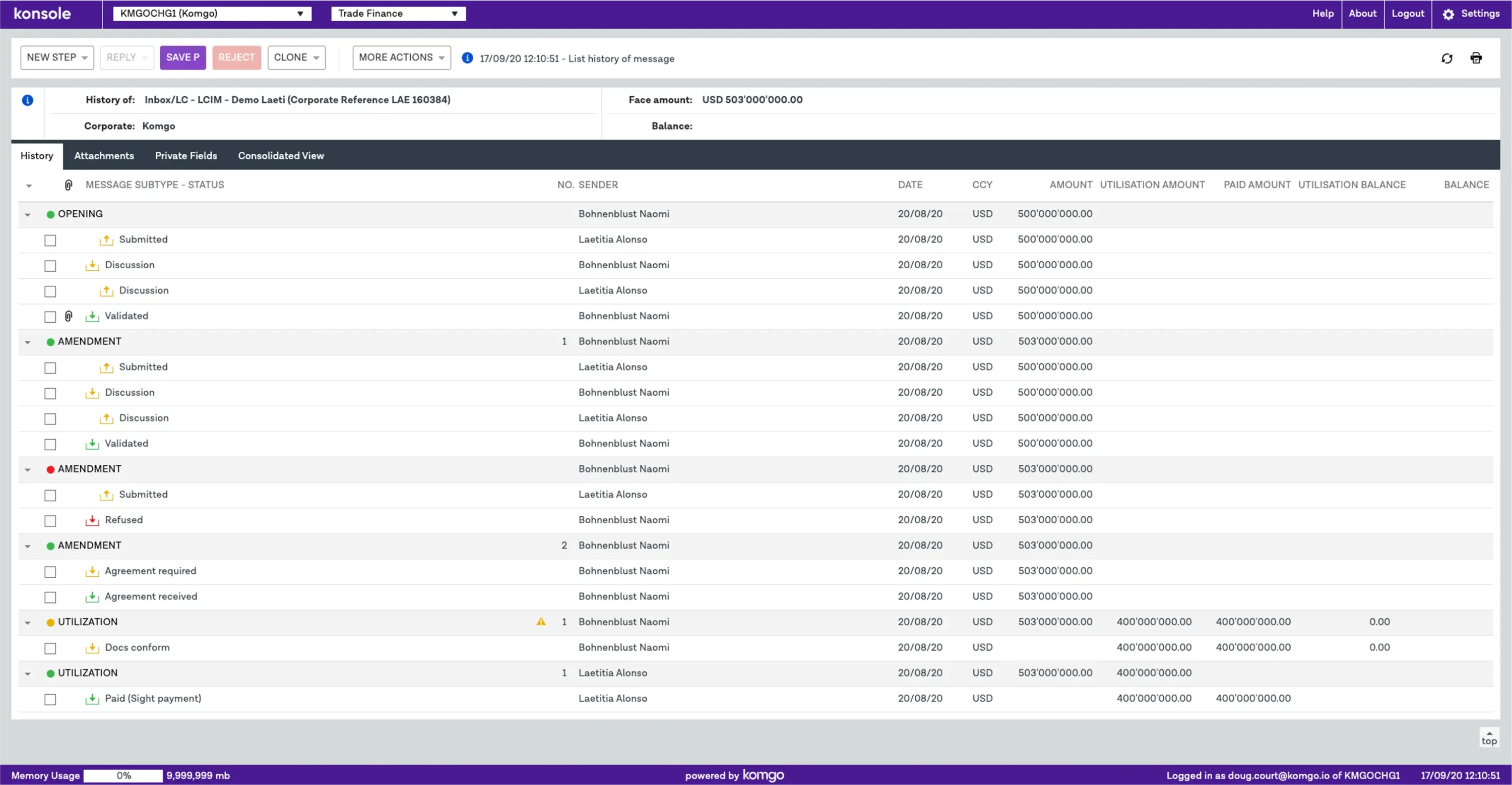

Komgo: Multi-Bank Trade Finance Channel for Corporates and Institutions

Komgo is a trade finance technology firm whose solutions support treasury, credit, and trade finance teams at corporates and banks worldwide.

Specifically, their corporate-facing product, called Konsole, establishes an authenticated and structured digital channel connecting corporates with either one or many banks. Through this channel, all stages of a trade finance instrument, including opening, issuance, amendments, document presentation, and final settlement, can be handled within a unified interface.

Konsole supports a broad range of trade finance instruments and workflows such as letters of credit, standby LCs, documentary collections, guarantees, letters of indemnity, release-of-goods instructions, financing requests, and more.

One of the core features of Konsole is data standardization. Thanks to it, all parties are able to see the same data fields and the most current version of any given trade instrument. Plus, open APIs let clients integrate Konsole with their own back office, ERP, or finance treasury systems.

In addition, Konsole centralizes all trade finance messaging, documents, and data in a single repository. It threads all messages related to a particular instrument or transaction together, which allows users to follow the full history of communications, amendments, and document exchanges. The system also supports secure attachments (up to 30 MB) and customizable signing rules and workflow routing, enabling organizations to enforce internal controls while collaborating externally.

Key features:

- Full lifecycle management of LCs, SBLCs, documentary collections, guarantees, letters of indemnity, release-of-goods instructions, and financing requests within a single authenticated channel

- Standardized data fields across all participants, enabling real-time view of a transaction's current status and version history

- Permissioned, encrypted messaging, recognized by leading banks as a valid instruction channel

- Centralized repository for all transaction documents and communication

- Customizable signing rules and internal routing enabling organizations to enforce internal controls while collaborating externally

- Open APIs for integration with back-office systems, ERP, and treasury platforms

Overall user rating: no verified ratings available.

Pricing: Custom quote per organization.

Oracle: Enterprise Trade Finance Infrastructure for Multi-Jurisdiction Banking

Built on a modular and microservices-based architecture, Oracle Banking Trade Finance Cloud Service makes it possible for banks to manage trade finance operations across multiple entities, currencies, and jurisdictions. The platform provides comprehensive support for documentary credits, collections, guarantees, letters of credit, standby LCs, and related trade finance instruments.

Integration is one of the key strengths of Oracle’s trade finance software. Through REST APIs and open system interfaces, it can connect with external systems such as AML/KYC providers, ERP platforms, and back-office modules. And since the solution is built on a microservices architecture, banks have the ability to scale operations, integrate with existing back-office systems, and deploy the Oracle platform across different regulatory and operational environments.

Another prominent feature is a unified 360-degree view of all trade transactions. Through a single-screen interface, users can access details on documentary credits, collections, guarantees, standby LCs, trade loans, limits, and outstanding balances.

The system also supports straight-through processing. Booking, amendments, messaging, and settlement for trade instruments can all be automated. Besides, its reusable data templates for customer information, contract terms, Incoterms, and currencies can further enhance efficiency and consistency.

Key features:

- Comprehensive front-to-back processing of documentary credits, documentary collections, guarantees, and standby LCs

- 360-degree single-screen view of all trade transactions

- Omnichannel support with a form-factor-agnostic UI enabling seamless transitions between self-service and assisted service

- Reusable data templates for customer information, Incoterms, contract terms, clauses, and currency preferences, enabling faster turnaround

- High-volume straight-through processing of B2B SWIFT messages (MT798) across the full lifecycle of documentary credits, guarantees, and collections,

- REST API and open system interfaces for integration with AML/KYC providers, ERP platforms, and back-office modules

Overall user rating: 4.0/5 on Oracle Banking Platform

Pricing: No pricing disclosed publicly.

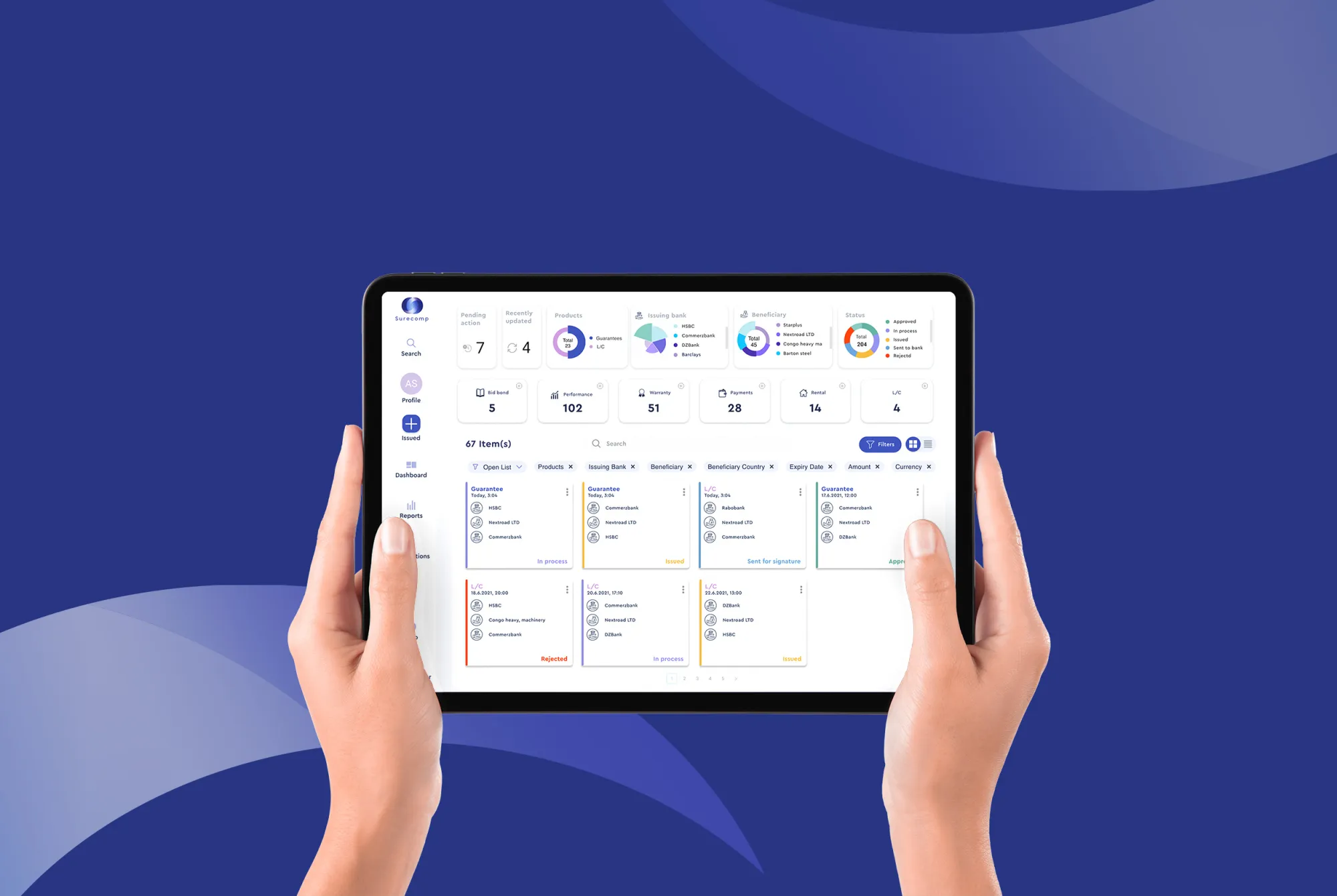

Surecomp: Collaborative Trade Finance Network for Banks and Corporates

Surecomp provides a web-based platform called RIVO that streamlines the management of trade finance for corporate clients. This financial solution enables users to manage a range of trade finance instruments, including letters of credit, bank guarantees, documentary collections, and trade loans.

One of the key strengths of the platform is its network model: rather than operating as a standalone corporate tool, it provides technology integration for companies with fintech partners, external systems, or internal banking systems.

At its Enterprise tier, RIVO supports the issuance of electronic documents of title in line with MLETR—relevant for corporates operating in jurisdictions that have enacted the model law, such as the UK, Singapore, and Bahrain.

Through structured data flows, workflow automation, document digitization, and centralized trade finance management, it supports secure and efficient processing of trade transactions. RIVO includes transaction-level ESG tracking and scoring, giving treasury and sustainability teams visibility into the ESG profile of their trade finance activity.

Surecomp also offers GenAI-powered features at the Professional and Enterprise tiers, including a guarantee text interpreter and GenAI converters for guarantee and LC notifications.

Key features:

- Full lifecycle management of LCs, SBLCs, guarantees, documentary collections, and trade loans across a multi-bank, multi-counterparty network

- Transaction-level ESG tracking and scoring for sustainability reporting across the trade finance portfolio

- Workflow automation and document digitization with comprehensive audit trails supporting compliance review and regulatory reporting

- Open API connectivity for integration with ERP, TMS, and fintech ecosystem partners

- Real-time credit limit visibility and utilization tracking across all connected institutions

- ISO 27001 and SOC 2 certified; hosted on AWS

Overall user rating:

Pricing: 5-tier plan structure (Starter through Enterprise); pricing is not disclosed publicly.

How to Choose the Best Trade Finance Software Provider?

To help you evaluate providers with more clarity, our experts have outlined the core aspects that you should pay close attention to when selecting trade finance software for your business.

No platform in this guide is the right choice for every organization. The best advice is to match the scope of the platform to the scope of your requirement—and verify that match through direct technical engagement, not marketing materials.

1. Start with your instrument mix, not the platform's capabilities

Before comparing vendors, map exactly which trade finance instruments your organization issues, processes, or plans to digitize—letters of credit, bank guarantees, documentary collections, supply chain finance, invoice financing, or a combination. This single step will eliminate most of the list immediately.

A platform built around guarantee lifecycle management for corporate treasury teams cannot replace a bank-grade documentary credits engine. A lending platform that covers invoice financing is not the same as a system built for UCP 600-compliant LC processing. Misaligning instrument requirements with platform scope is the most common and most expensive evaluation mistake.

Ask vendors directly: which of these instruments are native, production-deployed features — and which require configuration, customization, or third-party integration to deliver?

2. Identify your real integration constraints before evaluating features

Every platform in this guide claims broad integration capability. What matters is whether it integrates with your specific systems—your core banking platform, your ERP, your KYC/AML engine, your SWIFT connectivity model.

Integration failures are the primary cause of trade finance implementation delays. A platform with 100 available APIs is only as useful as the specific connections your operations team can actually build and maintain.

Before any demo: document your current technology stack and ask each vendor for reference clients running the same or similar integrations in production.

3. Separate deployment preference from deployment requirement

Cloud versus on-premise is often treated as a preference question. For many institutions it is a compliance requirement determined by data sovereignty rules, internal security policy, or regulatory mandate—particularly for banks operating in the EU, GCC, or APAC jurisdictions with strict data residency obligations.

Establish your deployment constraints with your IT and compliance teams before engaging vendors. A platform that only offers cloud deployment is not a viable option for an institution with on-premise requirements, regardless of its feature set.

4. Test configurability against your actual workflows, not a demo environment

Every vendor will show you a polished demo built around standard workflows. What you need to evaluate is how the platform handles your exceptions—your non-standard guarantee structures, your jurisdiction-specific document requirements, your internal approval hierarchies.

Request a proof of concept or a sandbox environment with your own data and your own edge cases. The platforms that perform well under those conditions are the ones that will perform well in production.

Specifically test: custom approval chains, non-standard product configurations, and document rule exceptions that reflect your actual operating complexity.

5. Evaluate compliance coverage against your specific jurisdictions, not global claims

"Compliance-ready" is a claim every vendor makes. What it means in practice depends entirely on where you operate.

A bank processing LCs under UCP 600 needs a different compliance architecture than a corporate managing guarantees under URDG 758. A lender operating in the EU under CRR3 faces different capital and reporting requirements than one operating in the UAE or Australia. A platform compliant in one regulatory environment may require significant reconfiguration—or may not be viable at all—in another.

Map your jurisdictions and the specific frameworks that apply—ICC rules, AML/CFT requirements, sanctions screening obligations, Basel IV exposure calculations where relevant—and verify coverage for each explicitly with the vendor's compliance team, not its sales team.

6. Assess total cost of ownership, not licensing cost

The licensing fee is rarely the largest cost in a trade finance software implementation. Implementation services, data migration, integration development, staff training, ongoing customization, and the internal resources required to manage the platform over time frequently exceed the initial contract value.

Request a total cost of ownership estimate across a three-to-five-year horizon, including implementation, integration, ongoing support, and the cost of upgrades or regulatory updates. For complex deployments, ask for references from clients of comparable size and operational complexity and speak to them about actual costs versus initial estimates.

7. Evaluate the vendor's trade finance domain depth, not just their technology

Trade finance is operationally complex in ways that generic fintech is not. ICC rule changes, SWIFT messaging updates, shifts in documentary practice, and jurisdiction-specific regulatory developments require a vendor that tracks and responds to the market—not just one that builds software.

Ask how the vendor handled recent market events: the adoption of eBLs in key jurisdictions, updates to URDG 758 practice, changes to sanctions screening requirements. The quality and speed of their response to those questions will tell you more about long-term partnership viability than any feature comparison.

Conclusion

The best trade finance software provider helps businesses accelerate transaction processing, reinforce compliance and risk controls, gain clearer visibility across global operations, reduce manual workload, and collaborate more effectively with banks and trading partners.

Choosing the right solution, however, suggests looking closely at several factors such as integration capabilities, customization options, the provider’s expertise, long-term scalability, and more.

To see how HES FinTech's platform fits your lending and trade finance operations, schedule a demo with our team.