"What’s the best loan origination system?" is the wrong question to open with. Ask ten lenders and you get ten answers, because a large commercial bank and a three-person alternative lender are not buying the same thing at all. A single ranked list of "top" platforms buries that difference. It grades every system against one imaginary buyer who doesn’t exist.

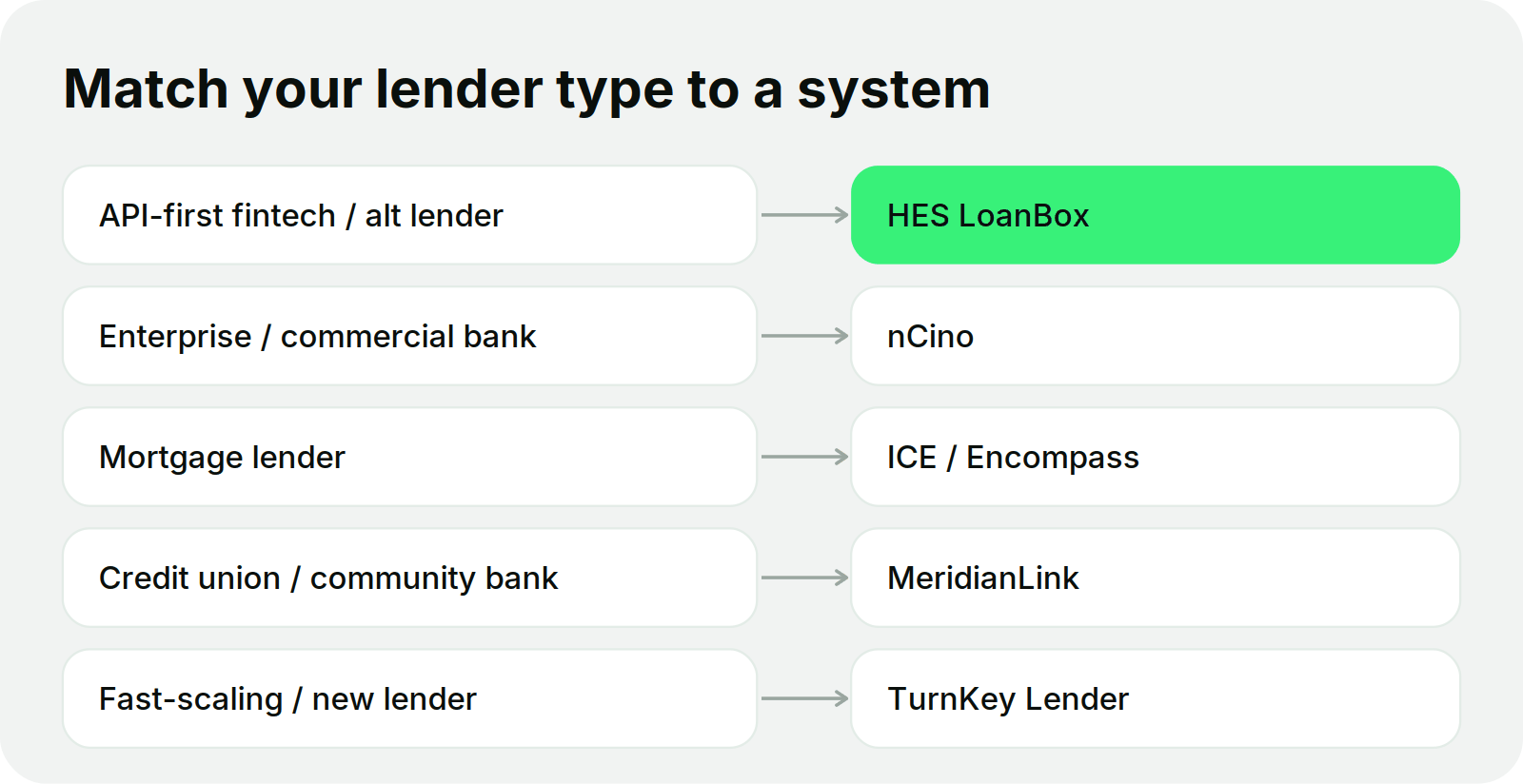

This comparison runs the other way. We sorted the market by the lender doing the buying, five profiles by size and operating model, and paired each with the loan origination system that suits it best. A credit union running on a legacy core has to weigh very different constraints than a fintech that reworks its product line every few months. The right choice falls out of that fit, not out of a leaderboard score.

Below is the at-a-glance version, with a full breakdown on each system further down.

| Loan origination system | Best-fit lender | Core approach | Deployment | Watch for |

|---|---|---|---|---|

| HES LoanBox | API-first fintechs and alternative lenders | Configurable, modular full lifecycle you can own at code level | Cloud, on-prem, or hybrid; API-first | Configuration depth needs some engineering time |

| nCino | Enterprise and commercial banks | Salesforce-native lending layer | Cloud (Salesforce) | Salesforce licensing, storage, and integration costs to clarify |

| ICE / Encompass | Mortgage lenders, brokers, IMBs | Deep mortgage-specific origination and compliance | Cloud | Built around mortgage, including HELOC; limited fit beyond it |

| MeridianLink | Credit unions and community banks | Multi-product origination for community FIs | Cloud | Best fit when needs match its configurable suite |

| TurnKey Lender | Fast-scaling and newly launching lenders | End-to-end LOS with AI-led decisioning and automation | Cloud | SaaS model; less code-level control than open platforms |

Compiled from publicly available vendor materials and independent user reviews (G2, Capterra), combined with our own assessment against a single set of criteria. Last checked: July 1, 2026. Confirm current details with each vendor.

How we compared these systems

This comparison was prepared by HES FinTech, which is also included in the list. We applied the same evaluation criteria to every loan origination system, and we cite public vendor materials and review platforms (G2, Capterra, and similar) where available. First place here means the best fit for one specific scenario, not the winner of a scored contest. Where a figure could not be sourced, we describe it qualitatively rather than estimate.

Five loan origination systems, matched to lender type

API-first for fintech and alternative lenders - HES LoanBox

HES LoanBox is a configurable, end-to-end lending platform that treats origination as one connected stage inside the full loan lifecycle, not a bolt-on intake form. Onboarding, application intake, decisioning, servicing, and collections run in the same operational system, so an approval made at origination carries its data and logic straight into repayment, with no handoff to a separate tool. Built API-first on open-source foundations, it fits lenders that want to shape their lending stack rather than rent a fixed one.

Best for API-first fintechs and alternative lenders that want origination inside a configurable, ownable platform, especially where the roadmap involves non-standard product logic, alternative-data decisioning, or deep integration with credit bureaus, payment rails, and accounting systems.

Market validation. HES LoanBox was listed in G2’s Credit Origination category, where HES reported a top-three position by user satisfaction at the time of review. Reviewers most often reference configuration depth and integration breadth.

| Overview | |

|---|---|

| Impact and decision quality | No standardized public benchmark is cited here. The platform’s stated value is consolidating onboarding, origination, decisioning, and servicing on one configurable stack rather than a single headline metric. |

| Security and compliance | ISO/IEC 27001-certified; HES FinTech completed a SOC 2 examination in 2026. Encryption, audit trails, role-based access, and support for KYC and AML processes; audit-ready by design. |

| Customization and implementation flexibility | Configurable underwriting logic, approval rules, product engines, and borrower journeys, set up through a no-code workflow builder. Composable architecture allows a phased module rollout or a full end-to-end deployment. Projects can start from around three months, with three to six months typical depending on integrations, data migration, and product complexity. |

| Supported lending models and scope | SME lending, BNPL, merchant cash advance, auto, consumer, mortgage, microfinance, and other loan types, launched through configuration. |

| Tech stack, vendor independence and scaling | Over 100 API integrations spanning credit bureaus, CRMs, payment gateways, ACH and card rails, and accounting systems. Built on open-source technologies including Java and Camunda. An optional developer license and code-access model can reduce dependency on the vendor, subject to the commercial agreement. Multi-entity, multi-currency, and multi-jurisdiction support. |

Key features

- Compliance-ready digital onboarding with KYC and KYB.

- Loan origination with configurable decisioning, real-time risk scores, and in-built scorecards.

- Servicing and collections: repayments, rescheduling, delinquency tracking, and automated recovery.

- A configurable product engine to launch any loan type without custom code.

- A white-label self-service borrower portal for applications, schedules, and restructuring requests.

- Platform infrastructure for multi-entity operations, integrations, security, and real-time analytics.

Main pros

- Deployment can start from three months depending on scope.

- An optional developer license gives deeper control and extensibility.

- Modular or full end-to-end rollout, including white-label borrower-facing journeys.

- High customization across workflows, products, rules, roles, and UI.

- Automation for both lender and borrower processes through no-code tools and role-based access.

Cons

- Broad scope means some niche requirements are met through configuration rather than out of the box.

- Implementation effort varies with integrations, data migration, and regulatory needs.

- Deep flexibility raises the need for clear change control and testing to avoid configuration sprawl.

The capabilities above are a summary of documented functionality, not the full scope of the platform.

What users say. On G2, HES reported a top-three position by user satisfaction in the Credit Origination category at the time of review. Reviewers most often reference configuration depth, integration breadth, and multi-entity and multi-currency support. Some clients note that complex custom reporting, dashboard and role customization, and initial configuration required extra planning and coordination with the vendor early in deployment.

Reviews are based on publicly available feedback.

Demo and trial: free demo and trial available.

Notable clients: ID Finance, Wa’ed, Fintuity, Alraedah, and others.

Pricing: license from $39K/year depending on business type; a fixed subscription with no per-user or per-application limits. Custom enterprise licensing available for multi-entity deployments.

Sources: HES FinTech product materials; G2 Credit Origination category. Last checked: July 1, 2026.

Other systems lenders in this category also weigh: DigiFi, LoanPro, LendFoundry, and Mambu.

Enterprise and commercial banks - nCino

nCino is a Salesforce-native cloud banking platform that runs lending inside the wider bank operating system, covering commercial, small-business, consumer, and mortgage workflows. Origination is one function within that broader environment rather than a standalone product, which is the point for institutions already on Salesforce that want loan data, pipeline, and CRM in the same place. It is aimed at banks with the scale, budget, and Salesforce footprint to absorb an enterprise platform.

Best for enterprise and commercial banks, particularly those already invested in Salesforce that want origination, portfolio monitoring, and CRM inside one ecosystem rather than stitched across separate tools.

Market validation. Reviews on G2 and Capterra are mixed. Reviewers credit the Salesforce integration and out-of-the-box origination coverage, while others cite total cost of ownership and the dependence on Salesforce skills.

| Overview | |

|---|---|

| Impact and decision quality | No standardized public performance metrics. Reviewers describe the value as consolidating borrower data, pipeline, and CRM into one environment. |

| Security and compliance | Built for regulated institutions and runs on Salesforce infrastructure, inheriting its access controls and audit tooling. |

| Customization and implementation flexibility | Configuration tends to standardize teams toward the vendor’s model. Implementation typically requires process design, data preparation, and Salesforce-skilled administrators or partners. |

| Supported lending models and scope | Commercial, small-business, consumer, and mortgage lending. |

| Tech stack, vendor independence and scaling | Built on Salesforce; buyers should clarify Salesforce licensing, storage, implementation, and integration costs in the commercial proposal. Large partner and integration ecosystem, with the company citing 2,700+ customers globally. |

Key features

- Salesforce-native loan origination and underwriting workflow.

- Borrower onboarding and client data capture.

- Portfolio monitoring and compliance workflows.

- Pipeline and relationship management inside the CRM.

- Loan product configuration within the platform.

Main pros

- Native Salesforce integration for institutions already on that stack.

- Consolidates borrower data, pipeline, and CRM into one system.

- Broad coverage across commercial, small-business, consumer, and mortgage lending.

- Built for regulated institutions.

Cons

- Because it is built on Salesforce, buyers should scope Salesforce licensing, storage, and integration costs up front.

- Customization typically needs Salesforce expertise.

- Some product-specific reviews (for example, the Mortgage Suite) cite UX and default-setting friction.

- Configuration standardizes teams toward the vendor’s model rather than their own.

The capabilities above are a summary of documented functionality, not the full scope of the platform.

What users say. On G2, reviewers frequently point to the Salesforce integration and describe origination coverage that works out of the box for standard commercial workflows. Criticism clusters around total cost of ownership and a platform some call broad rather than specialized. Product-specific feedback, notably on the Mortgage Suite, cites UX and default-setting friction, though that does not necessarily apply across every nCino product. Reviews range from positive notes on support to sharply critical accounts from some commercial-lending users.

Reviews are based on publicly available feedback.

Demo and trial: demo available via vendor contact; no open self-serve trial advertised.

Notable clients: the company cites 2,700+ customers globally; specific names are not listed individually here.

Pricing: available on request. Because nCino is built on Salesforce, clarify Salesforce licensing, storage, implementation, and integration costs in the proposal.

Sources: nCino profiles on G2 and Capterra; nCino company materials. Last checked: July 1, 2026.

Other systems lenders in this category also weigh: Finastra and Temenos.

Mortgage lenders, brokers, and IMBs - Encompass

Encompass by ICE Mortgage Technology (formerly Ellie Mae) is one of the most widely used mortgage loan origination systems in the United States, run as the system of record for a large share of US mortgage lenders. It carries a loan from application through processing, underwriting, closing, and investor delivery, tied into ICE’s wider ecosystem: the product and pricing engine, eClose, Simplifile, and MERS. For a mortgage shop, the draw is depth and reach in one lineage rather than breadth across loan types.

Best for banks, credit unions, and independent mortgage banks whose core business is residential mortgage, especially those that want mortgage compliance tooling and tight integration with the settlement and secondary-market ecosystem.

Market validation. ICE reports a customer base of more than 3,100 lenders and investors. On G2, Capterra, and TrustRadius, reviewers credit the end-to-end mortgage coverage and file organization; recurring criticism centers on a dated interface, a steep learning curve, and cost.

| Overview | |

|---|---|

| Impact and decision quality | No standardized public performance metric. Reviewers describe a single system of record that consolidates the mortgage file from application to investor delivery. |

| Security and compliance | ICE offers mortgage compliance tools and integrations that can support HMDA, TILA/RESPA, and other regulatory workflows, depending on the selected configuration; some components may be separate or licensed modules. |

| Customization and implementation flexibility | Configurable task-based workflows and an open API suite (Developer Connect). Reviewers describe implementation as resource-intensive and the interface as dated. |

| Supported lending models and scope | Residential mortgage, including HELOC and home equity, across retail, wholesale, and correspondent channels; limited fit for non-mortgage products. |

| Tech stack, vendor independence and scaling | Cloud-based, integrated across the ICE ecosystem (PPE, eClose, Simplifile, MERS) with a large partner marketplace; heavy reliance on that ecosystem. |

Key features

- End-to-end mortgage origination, processing, and underwriting in one system of record.

- Integrated product and pricing engine, borrower and TPO point-of-sale, and eClose.

- Compliance tooling and integrations for residential mortgage workflows.

- Secondary-market and investor-delivery workflows.

- Open API access through Developer Connect.

Main pros

- Deep, mortgage-specific functionality across the full loan lifecycle.

- Large integration marketplace and settlement and secondary-market ecosystem.

- Widely adopted, with a broad talent pool familiar with the system.

- Strong mortgage compliance coverage through the ICE ecosystem.

Cons

- Built for mortgage; weak fit for multi-product or non-mortgage lenders.

- Interface widely described as dated, with a steep learning curve.

- Costly and resource-intensive to implement, which smaller teams feel most.

- Some compliance capabilities may be separate or licensed modules rather than built in.

The capabilities above are a summary of documented functionality, not the full scope of the platform.

What users say. On G2 and TrustRadius, mortgage teams describe Encompass as a default LOS for residential lending, valued for keeping the entire file in one place and for its integration reach. The consistent complaints are an interface reviewers call antiquated, a learning curve that needs formal training, and cost that some smaller shops say they cannot carry.

Reviews are based on publicly available feedback.

Demo and trial: demo available; no open free trial.

Notable clients: ICE cites more than 3,100 lenders and investors; specific names are not listed individually here.

Pricing: available on request; widely described by reviewers as a premium-priced platform.

Sources: Encompass and ICE Mortgage Technology profiles on G2, Capterra, and TrustRadius; ICE company materials. Last checked: July 1, 2026.

Other systems mortgage lenders also weigh: Calyx Point, Floify, and LendingPad.

Credit unions and community banks - MeridianLink

MeridianLink is a loan origination platform built around the operating reality of credit unions and community banks, covering consumer, mortgage, and indirect lending. It leans on pre-built connections to core systems and bureaus and a configurable process engine, so lending teams at community institutions can run origination without rebuilding around the tool. Its fit is strongest where compliance, indirect lending, and core connectivity matter more than deep custom logic.

Best for credit unions and community banks that need multi-product consumer and mortgage origination with strong core and bureau connectivity, and that prefer configured best-practice defaults over a heavily bespoke build.

Market validation. Rated about 4.1 out of 5 on G2 as a vendor aggregate; MeridianLink Consumer is rated about 4.7 out of 5 on Capterra across roughly 17 reviews. Reviewers credit platform stability at volume and prebuilt integrations; the recurring criticism is a dated interface and configuration that routes through vendor services.

| Overview | |

|---|---|

| Impact and decision quality | One public G2 reviewer reported auto-approving around half of its standard loans; outcomes depend on credit policy, product setup, and institution data. |

| Security and compliance | Compliance tooling and audit support aligned with community-institution lending, including built-in data checks. |

| Customization and implementation flexibility | Configurable process engine with many configuration points, but changes past the standard rule engine typically route through MeridianLink Support rather than self-service. |

| Supported lending models and scope | Consumer, mortgage, and indirect lending for community financial institutions. |

| Tech stack, vendor independence and scaling | Cloud-based with 600+ prebuilt integrations and core connectivity. |

Key features

- Consumer, mortgage, and indirect loan origination.

- Configurable process engine and product and pricing tooling.

- 600+ prebuilt integrations with cores, bureaus, and third-party vendors.

- Borrower-facing digital application and eDocs.

- Compliance and data-check tooling.

Main pros

- Purpose-built for credit union and community-bank workflows.

- Stable across high application volumes.

- Broad prebuilt integration and core connectivity.

- Strong indirect-lending support.

Cons

- Interface reviewers describe as dated.

- Deeper configuration usually requires vendor services, not self-service.

- Best suited to institutions whose requirements fit its configurable suite and partner ecosystem.

The capabilities above are a summary of documented functionality, not the full scope of the platform.

What users say. On G2 and Capterra, reviewers from credit unions say the workflow assumptions match how their lending teams actually operate, and they point to stability at volume and the breadth of prebuilt connections. The common complaints are an interface described as dated and clunky, and configuration limits: several reviewers note they cannot rename fields or change required-or-optional logic without contacting support.

Reviews are based on publicly available feedback.

Demo and trial: demo via sales contact; no open trial.

Notable clients: published case studies include A+ Federal Credit Union, Rogue Credit Union, and APL Federal Credit Union.

Pricing: quote-based, depending on the selected products, integrations, and deployment scope.

Sources: MeridianLink profiles on G2 and Capterra; MeridianLink case studies. Last checked: July 1, 2026.

Other systems community lenders also weigh: Abrigo and Origence.

Fast-scaling and newly launching lenders - TurnKey Lender

TurnKey Lender is an end-to-end lending platform aimed at lenders that want to launch and scale quickly with heavy automation. It covers origination, servicing, and collections, with AI-led decisioning and configurable workflows available out of the box. For a fast-growing or newly launching lender, the pull is speed to market and automation without building the stack, rather than deep code-level ownership.

Best for fast-scaling and newly launching lenders, including consumer, SME, BNPL, and embedded-finance providers, that want an out-of-the-box, automation-led platform covering origination through collections.

Market validation. Rated about 4.7 out of 5 on G2 across roughly 18 reviews and about 4.6 out of 5 on Capterra across roughly 36 reviews, with reviewers citing automation and speed of deployment.

| Overview | |

|---|---|

| Impact and decision quality | No standardized public benchmark is cited here. The platform’s stated value is automating decisioning and workflow across the lending lifecycle; reviewers cite fast deployment. |

| Security and compliance | Cloud-based with role-based access and configurable compliance workflows. Confirm certifications and regional compliance coverage in the proposal. |

| Customization and implementation flexibility | Configurable, AI-led workflows set up largely without custom code, which is faster to launch than a heavily bespoke build, with less code-level control than open-source platforms. |

| Supported lending models and scope | Consumer, SME, commercial, BNPL, payday, auto, equipment, and embedded finance. |

| Tech stack, vendor independence and scaling | Cloud SaaS with API integrations and prebuilt connectors; a multi-tenant model rather than code-level ownership. |

Key features

- Online application intake and borrower onboarding.

- AI-led credit decisioning and scoring.

- Configurable workflows and product setup.

- Servicing and collections in the same platform.

- Borrower self-service portal.

Main pros

- Fast deployment and out-of-the-box automation.

- End-to-end coverage from origination through collections.

- AI-led decisioning without a custom build.

- Broad loan-type coverage for growing lenders.

Cons

- Less code-level control than open-source platforms; a SaaS, multi-tenant model.

- Customization is bounded by the platform’s model.

- Certification and regional-compliance depth should be confirmed per deployment.

- Pricing is not publicly listed.

The capabilities above are a summary of documented functionality, not the full scope of the platform.

What users say. On G2 and Capterra, reviewers describe TurnKey Lender as quick to deploy and highly automated, and they credit the AI-led decisioning. Some note that deeper or non-standard customization runs into the bounds of a packaged platform, and that pricing is disclosed only after contact.

Reviews are based on publicly available feedback.

Demo and trial: demo via vendor contact; no open self-serve trial advertised.

Notable clients: serves lenders across consumer, SME, and embedded finance; specific names are not listed individually here.

Pricing: available on request.

Sources: TurnKey Lender profiles on G2 and Capterra; vendor materials. Last checked: July 1, 2026.

Other systems fast-scaling lenders also weigh: HES LoanBox, LendingPad, Bryt (servicing-led), and LendingWise.

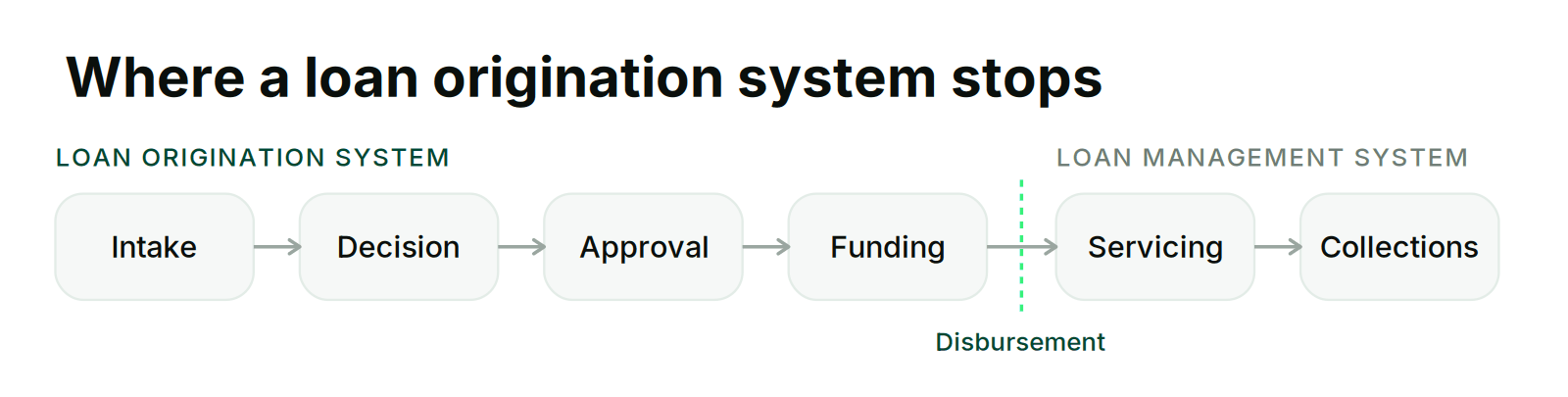

What a loan origination system does, and where it stops

A loan origination system typically covers application through approval and funding: application intake, data capture, credit checks and decisioning, document handling, approval, and disbursement. Servicing usually begins after disbursement, and what comes next, repayments, statements, delinquency, restructuring, collections, and portfolio reporting, belongs to a loan management or servicing system (LMS). Some platforms combine both capabilities on one record.

The distinction matters at buying time. A lender that treats origination as the whole job can end up bolting a separate servicing tool onto the back, then reconciling two systems that were never designed to share a borrower record. Some platforms cover only origination, some only servicing, and some carry the loan end to end. You need to settle which of the three you are actually buying up front, because a mismatch here is one of the most expensive kinds to unwind later.

What separates a modern loan origination system from a basic one

After more than 15 years building lending technology and watching the market shift, our view is that in 2026 the line between a basic and a modern loan origination system is usually not the feature list. In our experience, most serious vendors now offer digital intake, some decisioning, a document store, and an API. What tends to separate them sits underneath:

- Speed of change. How fast your own team can adjust a rule or launch a product without opening a vendor ticket. Configuration you control, versus configuration you request, is the difference between a roadmap you own and one you wait on.

- Explainable decisioning. Whether a credit decision comes with reason codes and an audit trail, not just a score with no paper behind it. Examiners and credit committees both ask how a decision was reached.

- Connection to servicing. Whether origination shares a borrower record with servicing and collections, or hands off to a separate system that then has to be reconciled.

- How the platform is owned. In our view, a fixed multi-tenant model tends to tie you to the vendor’s roadmap, while code-level access or a developer license lets you extend the system where your business is different.

- Real integration depth. Live API exchange with bureaus, payment rails, and core banking, versus batch files and middleware that quietly slow every change.

- Data and decisioning fit. Whether the platform can integrate the data sources and decisioning tools your credit policy requires, rather than only a standard bureau pull.

By 2026, in our view AI in the pitch deck tells you little on its own. The more useful question is whether the architecture lets a model actually move your operation, or whether the model is attached to a platform too rigid to act on what it produces.

Why the right loan origination system depends on your business type, not your industry

Two lenders in the same industry can need opposite systems, and two in different industries can need the same one. What drives the choice is business type: size, product complexity, volume, regulatory surface, and how much you intend to change the system yourself.

A three-person private lender and a national bank both make loans, but one needs a tool it can run alone for a modest monthly fee and the other needs an enterprise platform with a project team behind it. A single-product consumer lender and a multi-product alternative lender both sit under the fintech label, yet one can live inside a fixed workflow while the other needs configurable product logic to survive its own roadmap.

Sorting vendors by industry label, mortgage software here, credit-union software there, hides this. The more useful axis is operating model: how many products you run, at what volume, under how much compliance weight, and whether your edge comes from changing the system faster than competitors or from running a proven one at scale. That is why the five loan origination systems above are grouped by lender type, not by vertical.

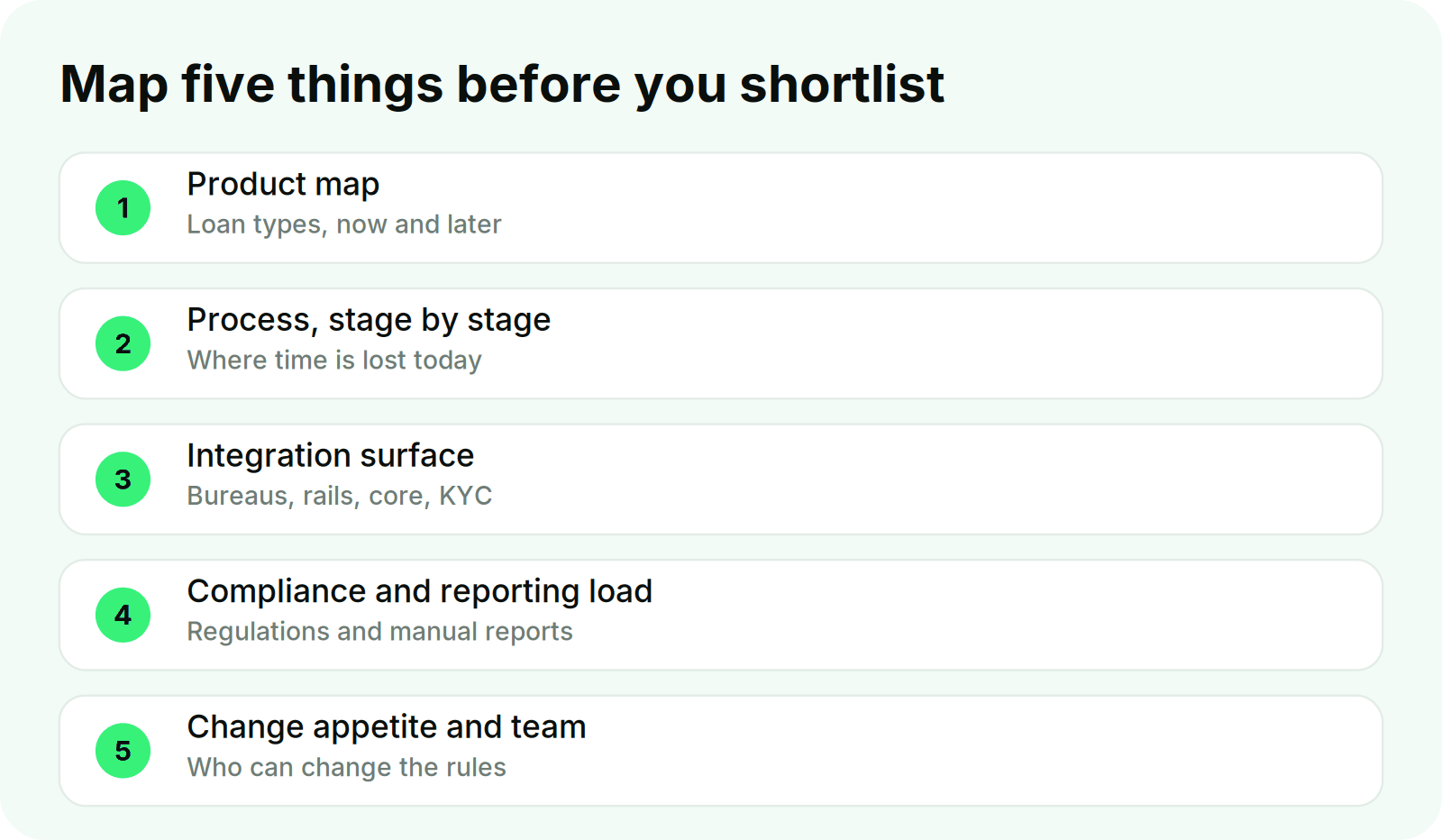

How to prepare before you shortlist loan origination systems

Most poor LOS decisions trace back to shopping for features before understanding your own operation. Before the first vendor call, put five things on paper. The map turns demos from feature tours into a test the system either passes or fails.

- Your product map. Every loan type you run today and plan to run in 18 months, with the terms, rates, and repayment logic that make each one different. This tells you whether you need a configurable product engine or a fixed one.

- Your process, stage by stage. Application, verification, decision, approval, funding, and the handoff to servicing, with the role that owns each step: loan officer, underwriter, credit committee, processor. Mark where time is lost today; weeks of delay usually hide in one or two handoffs.

- Your integration surface. The systems the LOS must talk to: credit bureaus, KYC and AML, payment rails, core banking, accounting, e-sign. Separate must-connect-on-day-one from later.

- Your compliance and reporting load. The regulations and audits you answer to, and the reports you still assemble by hand.

- Your change appetite and team. Whether you have engineers who can extend a platform or need a system your ops team runs alone, and how often you expect to change rules.

In our experience, lenders who bring this map to the first call cut their selection time and avoid the mid-deployment surprise of a loan origination system that cannot bend to how they actually work.

Mistakes lenders make when choosing a loan origination system

- Buying by feature checklist. The longest feature list rarely wins; fit to your process does. A system can do everything on paper and still fight the way your team works.

- Confusing origination with the full lifecycle. Choosing an origination-only tool, then discovering servicing and collections need a second system and a reconciliation project between them.

- Ignoring speed of change. Not asking who has to be involved to change a rule or launch a product. If every change is a vendor ticket, your roadmap becomes the vendor’s roadmap.

- Taking "API-first" on faith. Some integrations are batch files or need middleware. Ask for a live demo of the actual connection, not a logo wall.

- Reading star ratings as verdicts. Review scores mix incentivized and organic feedback and often reflect servicing or borrower-side experience rather than origination depth. Weigh review volume, recency, the reviewer’s role, and the specific use case, not just the average.

- Sizing for today, not 18 months out. Picking a tool that fits current volume and product mix, then re-implementing a year later, which costs far more than the platform ever did.

How loan origination system pricing works

Pricing for a loan origination system is rarely a public sticker. It ranges from transparent entry pricing for small-lender and broker tools, where some publish plans from around $50 a month, to enterprise licensing quoted only after scoping, as with nCino, Encompass, MeridianLink, and TurnKey Lender. What moves the number: deployment scope, the count of products and modules, integrations, data migration, user or entity count, and compliance needs.

Watch the total cost of ownership beyond the license. A Salesforce-native platform brings its own licensing, storage, and integration costs to clarify. Some tools price capabilities like ACH or a borrower portal as add-ons. Enterprise mortgage systems carry implementation and training costs that can dwarf the annual fee. A useful discipline is to ask each vendor for a three-year total rather than a first-year price, and to confirm what is included versus billed separately. HES LoanBox, for context, uses a fixed subscription from $39K a year with no per-user or per-application limits, which is a different model from per-seat or per-module pricing.

A short checklist for choosing your loan origination system

- Is it origination-only, servicing-only, or end to end, and which do you actually need?

- Can your own team change a rule or launch a product, or does every change route through the vendor?

- Is decisioning explainable, with reason codes and an audit trail?

- Do the integrations you need exist as live connections, shown in a demo, not just listed?

- Does it fit your business type (size, product complexity, volume, compliance), not just your industry?

- What is the three-year total cost, including licenses, add-ons, implementation, and training?

- Does it scale to your 18-month plan, not just today’s volume?

- What do the negative reviews say, and are they about origination or something else?