The significance of digital transformation in banking can not be overstated and the numbers make it clear. The global digital transformation market in banking and financial services is expected to hit $215 billion by 2030, so it’s pretty evident that banking and digital transformation have become inseparable and that innovation is poised to continue to change the way financial institutions operate, compete, and create value.

In this article, we will take a look at what digital transformation for banks is all about, some of the key benefits and challenges it brings, the technologies driving this change, such as AI, ML, lending software, cloud, and IoT, as well as share some practical insights on how to build a robust strategy for successful digital transformation.

What is Digital Transformation in Banking?

Typically, it involves modernizing legacy systems with the help of sophisticated new technologies and tools such as cloud computing, artificial intelligence, machine learning, advanced data analytics, and automation. All of these enable banks to improve their efficiency, substantially reduce operational costs, mitigate risk, and create more personalized experiences for their customers.

The Importance of Digital Transformation in Banking

Digital transformation in the banking industry is important because, thanks to it, banks manage to remain competitive as well as meet customers’ expectations for greater speed, personalization, and more accessible digital services.

What’s more, digital transformation initiatives help banks enhance operational efficiency, bolster data-driven decision-making, and significantly improve risk management.

What’s Driving Digital Transformation in Banking?

According to Precedence Research, there exist lots of factors that allow for the acceleration of digital innovation in the banking sector.

These include:

- Technological advancements — With the ubiquitous adoption of modern tech across industries and domains, banks, too, are compelled to refine their systems and service models.

- Need for operational efficiency — The pressure to give a boost to internal processes, cut down on operational costs, and enhance customer experience remains a very big motivator for transformation.

- Digital channels — Expanding digital platforms allows banks to deliver far better services while lowering operational expenses.

- Need for cybersecurity measures — According to IBM’s 2025 Cost of a Data Breach Report, the average global cost of a data breach has reached $4.4 million. Because of this, banks are eager to launch digital transformation initiatives so as to reinforce stronger cybersecurity frameworks and safeguard sensitive data.

- Investment in technology — The growing investment from leading banks and top financial institutions continues to speed up innovation.

Crucially, apart from the research data, there are some other factors that need to be highlighted:

- Rising customer expectations — The rising demand for more personalized and agile digital services is pushing banks to innovate.

- Evolving regulatory requirements — Frequent changes in regulatory frameworks make banks revise their existing compliance strategies and systems.

- Cost pressures — The need to control expenses and sustain profitability urges banks to integrate novel technologies in their operations.

- Intensifying competition — The growing presence of fintechs and other digital-first players forces traditional banks to make the grade and get more agile and customer-focused.

Which Technologies Can Help Bring About Digital Transformation in the Banking Industry?

Several cutting-edge technologies and tools enable the proliferation of digital innovation in banking.

Below, we will provide a lowdown on the ones that stand to make the biggest impact.

- With artificial intelligence and machine learning in their arsenal, banks are able to give a leg up to numerous operations as well as process more datasets, automate decision-making, and better detect fraudulent activities.

AI also gives banks an opportunity to advance in credit scoring and risk checks operations. It helps them figure out who is a good borrower faster and more accurately, all while opening up credit opportunities to more people. On top of that, AI-powered virtual assistants can jump in with instant and personalized support, which both speeds things up behind the scenes and makes the overall service feel a lot smoother.

An important thing to notice here is that generative AI, in particular, stands to help banks take customer interaction to a whole new level. According to McKinsey’s Global Banking Annual Review 2025, more than half of consumers already use generative AI tools and expect their banks to provide similar capabilities, with many willing to switch providers if those expectations aren’t met. - Blockchain technology is increasingly finding specialized uses within the banking sector. Lots of banks worldwide are already experimenting with it for cross-border payments, trade finance, asset tokenization, and secure identity checks. What’s more, blockchain can be used for bank-issued tokenized deposits. A notable example of this is JPMorgan’s JPM Coin that facilitates real-time settlement of tokenized deposits on a permissioned blockchain.

- Thanks to application programming interfaces (APIs), banks can quite easily connect with third-party providers, fintechs, and other digital ecosystems. As a result, they manage to deliver more comprehensive and interconnected financial products and provide a far better and integrated customer experience.

- Cloud technology is getting popular among banks worldwide. It is expected that the global spending by financial services companies on cloud computing will have grown to $205 billion by 2028. With cloud tech, banks can store and process large volumes of data, rather quickly deploy new digital services and products, and strengthen security and resilience through advanced infrastructure management.

- The Internet of Things (IoT) has quite a versatile role in banking. The tech makes life easier for customers with contactless payments on smartphones and smartwatches and automates a multitude of tasks like cash management in ATMs and even energy optimization in branches. In addition to this, IoT devices like smart cameras, biometric scanners, and tamper sensors provide continuous monitoring while wearable-based fingerprint authentication adds an extra layer of protection for transactions.

- Robotic process automation (RPA) helps automate repetitive and rule-based banking tasks, so employees are able to zero in on more important and higher-value work. Plus, RPA cuts down on errors that happen during manual processing, accelerates workflows, and ensures greater consistency across processes such as loan management, compliance checks, and account reconciliation.

- Big data analytics gives banks a better read of customer behavior, market dynamics, and risk exposure. By transforming mountains of data into useful insights, banks are better prepared to anticipate customer needs, customize their products and offerings, and make more informed strategic decisions.

What Are the Main Benefits of Digital Transformation in Banking?

The benefits of digital transformation initiatives are vast and continually expanding. Below are some of the most impactful advantages of digital innovation in the banking sector.

| Benefit | How it works |

|---|---|

| Greater operational efficiency and cost savings | Automation through RPA and AI reduces manual work, cuts costs, and boosts efficiency, which allows teams to focus on strategic priorities and long-term resilience |

| Improved customer experience | Digital tools offer faster and more reliable banking with real-time insights and easier access to services, fostering customer loyalty and driving higher retention |

| Smarter decision-making | Advanced analytics and ML reveal trends, risks, and customer needs, empowering banks to make informed decisions and confidently plan growth |

| Stronger security | Integrated digital systems enhance oversight and risk detection, which helps banks protect assets and customer trust while maintaining business continuity |

| Simplified compliance | Specialized reporting and monitoring tools streamline reporting and monitoring, reduce errors, and free up teams to focus on innovation and service improvements |

| Competitive advantage | Modern DevOps practices, CI/CD pipelines, and API-first design enable faster product launches and more personalized offerings as well as help banks stay ahead of competitors and build lasting growth |

1. Greater Operational Efficiency and Cost Savings

Technologies such as RPA and AI help automate repetitive manual tasks, which bolsters workflow efficiency, reduces errors, and, crucially, enables teams to zero in on more valuable strategic priorities and essential work.

As a result, banks can achieve measurable cost reductions and manage to significantly improve operational efficiency from infrastructure and engineering-modernization efforts (for instance, JPMorgan Chase reported gaining $500 million in productivity and cost efficiencies).

2. Improved Customer Experience

Digital has become the primary mode of bank-customer interaction. With banking solutions like digital wallets, automated financial planners, and AI-enabled chatbots, banking gets simpler and way less of a headache. 54% of banking customers worldwide check their banking app daily, according to recent research.

For banks, the outcome of this is quite clear: the happier customers are, the more loyal they become, and the more opportunities banks will gain to boost revenue.

3. Smarter Decision-Making

Advanced analytics and machine learning equip banks with actionable insights that enable them to spot emerging customer needs, detect trends, and anticipate potential risks before they escalate.

Thus, analyst studies, like McKinsey, show upgraded origination journeys can shorten loan processing times by 15–40%. Certain cases show that automation can dramatically shorten origination and disbursement cycles, for instance, in microfinance.

4. Stronger Security

Banking industry digital transformation strengthens a bank’s ability to protect its assets, operations, and customer trust.

Integrated risk management platforms, real-time monitoring systems, and AI-driven fraud detection tools help banks spot risks early and deal with them before they turn into huge financial losses or operational troubles. For instance, IBM reports that American Express got a 6% uplift in fraud detection, while PayPal got a 10% real-time detection improvement with AI tools.

A bonus point here is that customers feel much more confident engaging with digital services while the bank manages to safeguard its reputation and support sustainable growth.

5. Simplified Compliance

Modern financial management systems enable banks to stay on top of requirements such as the Bank Secrecy Act (BSA) and Anti-Money Laundering (AML) regulations. On top of that, they deliver real-time regulatory updates and secure record-keeping, so that teams can spend less time on routine checks and devote more effort to enhancing the quality of services.

Thus, the Deloitte report on RegTech says that automated KYC onboarding can reduce onboarding time by up to 70%.

6. Competitive Advantage

Banking digital transformation assists teams in launching innovative products and services as well as customizing offerings to ever-changing customer needs and wants. Digitally advanced banks outperform their peers in revenue growth and expense control, according to a McKinsey report.

That blend of speed, actionable insights, and adaptability positions banks ahead of their competitors and builds long-term loyalty and sustainable growth.

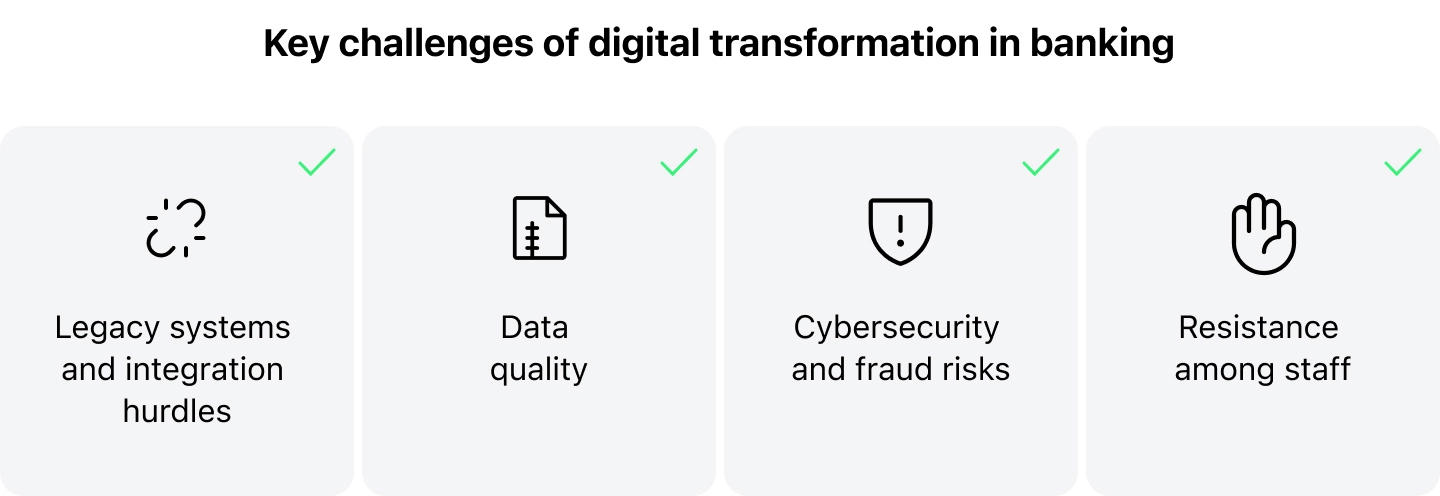

Key Challenges of Digital Transformation in Banking

In spite of all its advantages, digital transformation in the banking sector comes with several challenges, and it is crucial for institutions to understand them before embarking on their digital transformation journey.

Below, we highlight the most common digital transformation challenges in banking and offer some practical tips on how to address them.

1. Legacy Systems and Integration Hurdles

Many banks still rely on outdated IT infrastructure and integrating modern platforms with these legacy systems usually requires careful planning and significant resources.

Any misalignment, though, may slow down transformation initiatives and prevent banks from fully realizing the operational efficiencies that digital transformation promises.

To overcome this hurdle, it’s advisable to prepare a phased bank digital transformation strategy: clearly map system dependencies, develop a detailed migration plan, prioritize security and compliance, and invest in middleware or APIs to successfully bridge the gap between old and new technologies and systems.

2. Data Quality

As you know, accurate and accessible data is the foundation of successful digital transformation.

Yet, many banks have to deal with fragmented or siloed datasets across departments, which can hinder analytics, risk management, and the delivery of personalized services.

In this case, banks must invest in data governance frameworks, cleansing processes, and unified data platforms in order to ensure that only reliable and high-quality information drives their decision-making.

3. Cybersecurity and Fraud Risks

While novel technologies do help strengthen defenses, expanding digital services sometimes increases banks’ exposure to cyber threats and fraud, which can compromise customer trust, damage reputations, and disrupt operations.

To prevent this from happening, banks will be better off if they allocate significant attention and resources to advanced security measures like encryption, intrusion detection systems, and endpoint security, as well as consider adopting continuous monitoring and fraud detection systems so as to protect sensitive information and maintain confidence among customers.

4. Resistance Among Staff

One of the most widespread banking digital transformation challenges is the resistance among the staff.

Employees who are accustomed to traditional workflows may resist new tools or processes, often fearing that technology will replace them, which can slow adoption.

To tackle this challenge, you need to cultivate a culture that encourages innovation, learning, and collaboration, plus communicate to your employees that technology is meant to assist rather than replace them.

How to Start Digital Transformation in Banking in 2026

Although the digital transformation process may vary from organization to organization and involve different steps depending on current readiness, there are some universal actions worth considering to ensure a successful digital transformation.

Let’s take a closer look at the most essential steps.

1. Develop a Comprehensive Strategy

Before starting your digital revolution in banking, you need to map out a clear vision that coordinates teams, guides investments, and focuses on improving both operations and customer experiences.

With a solid strategy in place, it will be much easier for you to cope with complex changes and better measure success along the way.

2. Assess Systems, Processes, and Opportunities

Not every workflow or system requires immediate change.

With respect to this, conduct a thorough analysis of your departments, processes, and technologies to pinpoint where transformation efforts will deliver the most meaningful impact.

Such practice will help you reduce unnecessary disruption, enable phased implementation, and make sure that the bank can maintain smooth operations while modernizing the most critical areas.

3. Create a Change Management Framework

A structured change management framework supports employees as they adapt, fosters engagement, and encourages ownership of new ways of working. When staff gets the purpose and benefits of transformation, adoption becomes more natural and effective.

Plus, don’t forget that specialized training programs, mentoring, and ongoing support help employees gain extra confidence with new systems and workflows.

4. Plan Finances and Allocate Resources

Undeniably, digital transformation is a costly initiative and requires careful planning around budgets, investments, and expected returns.

Therefore, take the time to execute resource planning that balances ambition with practical execution, keeping projects realistic and manageable. This will help you accurately forecast costs and properly allocate resources to high-priority initiatives.

5. Tap Into Strategic Partnerships

Digital transformation is complex but you don’t have to tackle it alone.

Engage trusted technology partners with domain expertise and regulatory experience alongside digital transformation consulting experts who can bring specialized skills and hands-on experience to your initiative. Their guidance will help you anticipate challenges, optimize processes, select the right technologies to support your strategic objectives, as well as make the entire transformation process smoother and more successful.

6. Monitor Progress, Adapt, and Secure Operations

Keep in mind that digital transformation is an ongoing process rather than a single project.

You will be better off if you regularly track progress, explore emerging technologies, and keep a pulse on customer needs to ensure that your initiatives stay effective and relevant.

Simultaneously, enforce robust security measures to safeguard operations and customer trust and create a strong foundation for sustainable growth and continuous innovation.

Conclusion

Digital transformation in banking provides a wide range of benefits such as enhanced operational efficiency, significant cost savings, stronger security, improved customer experiences, and a more competitive market position.

Achieving these results requires banks to develop a clear strategy, prioritize the systems and processes that matter most, equip staff to adopt new ways of working, and engage reliable and knowledgeable partners.