What is Loan Management Software?

Loan management software is the operational layer used to control active lending and post-disbursement servicing across the loan lifecycle. In a broad implementation, it can connect origination, loan servicing, collections, reporting, and compliance into a single environment — but its core role is to give lenders a consistent operational view of every loan after it enters the portfolio.

This distinction matters because loan management is not only about processing new applications or collecting payments. It is about keeping loan data, repayment schedules, borrower status, servicing actions, exceptions, and portfolio performance aligned in one structured environment. The servicing engine inside the platform tracks balances, applies interest, processes payments, generates statements, and handles loan modifications — all of which would otherwise sit in separate spreadsheets or legacy systems.

For banks, fintechs, and non-bank lenders, a strong loan management system acts as the control layer between front-office lending activity and back-office portfolio administration and loan servicing operations. It helps teams understand what is happening across active loans, where operational risks are emerging, and which workflows need attention.

This shift towards innovation isn’t happening gradually. It’s accelerating at full speed. Currently valued at $3.1 billion in 2023, it’s projected to reach $7.8 billion by 2031, just 6 years from now.

By the end of 2025, the loan management and debt collection software industry had been transformed by technological advancements. Real-time pipelines, cloud-native, API-first infrastructure, AI decisioning, and mobile-first apps now power the modern loan management process and drive business decisions when integrating new tools.

But the path to digitization isn’t frictionless. The wrong choice of software could introduce significant technical debt or even compliance risks. Poor integration strains business operations. Rigid workflows limit your capacity. Unreliable or unsafe AI models create compliance exposure. Fragmented systems make scaling next to impossible. In a market moving this quickly, making the wrong decision is a strategic vulnerability — which is why the best loan management software today must operate as hyper-connected engines.

What loan management software is responsible for?

A loan management system is responsible for maintaining structure after a loan has been created. While origination tools focus on application intake and approval, loan management software supports the operational life of the loan — its servicing, repayment, and post-disbursement administration — once it becomes part of the lender’s portfolio.

In practical terms, this includes:

- tracking loan status, principal balances, repayment schedules, and borrower activity;

- generating amortization schedules and applying accurate interest calculations across fixed, variable, and irregular payment structures;

- coordinating loan servicing actions such as payment updates, ACH processing, late payment fees, reminders, rescheduling, and account changes;

- managing delinquency tracking, default flags, and connecting with collections workflows when accounts become overdue;

- supporting portfolio visibility through reports, dashboards, and performance indicators;

- integrating with accounting systems (such as QuickBooks, NetSuite, or Sage), credit bureaus, and core banking platforms for reconciliation and regulatory reporting;

- preserving audit trails, investor reporting, and operational consistency across teams, branches, products, or markets

The value of loan management software is therefore not limited to automation. Its deeper function is to create a reliable operating framework where loan data, borrower interactions, repayment behavior, servicing actions, and risk signals remain connected throughout the lifecycle.

How We Evaluate Loan Management Software

This loan management software comparison is based on independent research conducted in 2026 and reflects publicly available data on leading loan management systems. The goal is to help lenders evaluate platforms using consistent, practical criteria aligned with real-world implementation needs.

To build this comparison, we analyzed vendor documentation, product pages, client case studies, and verified user reviews from platforms such as Capterra, G2, and Gartner Peer Insights. Where third-party validation was limited, we relied on documented product capabilities and observable market positioning.

Each loan management system was assessed using a standardized framework designed to reflect how lending software performs across the full loan lifecycle — from onboarding and origination to servicing and collections.

Key evaluation criteria for loan management software

- End-to-end loan lifecycle support

Measures how completely the platform covers onboarding, underwriting, servicing, and collections within a single system - System flexibility and configurability

Evaluates how easily lenders can adjust workflows, credit policies, and loan products without custom development - Integration capabilities and API ecosystem

Assesses the availability of APIs and readiness to connect with CRMs, payment systems, credit bureaus, and other third-party services - Scalability and performance

Examines how well the platform handles growth in loan volume, users, and geographic expansion - Deployment options

Considers support for cloud, on-premise, or hybrid environments depending on regulatory and operational requirements - Security and compliance readiness

Reviews alignment with industry standards, data protection requirements, and auditability - User experience and operational usability

Analyzes both borrower-facing interfaces and internal tools used by underwriting and operations teams - Market validation and real-world usage

Looks at client adoption, case studies, and presence across different lending segments

How to use this evaluation

This framework is designed to compare loan management platforms across dimensions that directly impact efficiency, scalability, and compliance. It does not define a single "best loan management software" for all lenders.

Instead, it helps identify which platform is better aligned with specific business models, loan products, and operational requirements — whether for banks, fintech companies, or non-bank lenders.

Best Loan Management Software Shortlist

The platforms below are not identical in scope. Some are full lifecycle lending platforms, some are stronger in servicing or portfolio administration, and others are more closely tied to origination or mortgage workflows. For that reason, this comparison looks beyond feature lists and considers how each system supports loan control, operational continuity, and portfolio-level visibility.

| Platform | Loan types supported | Modularity & configurability | Developer license & APIs | AI/Automation | Core business use | Standout modules | Deployment |

|---|---|---|---|---|---|---|---|

| HES LoanBox | SME, BNPL, MCA, auto, consumer, mortgage, microfinance, embedded | High (configurable), custom development | Yes | Yes | Banks, Alt lenders, SME lenders, Fintech | Origination, servicing, collections | Cloud/On-prem |

| Mambu | SME, BNPL, mortgage, embedded, business, asset | High (configurable) | Yes | Medium-High | Digital banks, Fintech | Loan, payments, analytics | Cloud |

| TurnKey Lender | Consumer, commercial, BNPL, payday, equipment, leasing | High (configurable, AI-led) | High (AI-led) | High (AI-led) | Banks, fintechs, alt lenders, vertical/embedded lenders, BNPL | Origination, AI scoring, collections | Cloud |

| Finastra Fusion Loan IQ | Syndicated, corporate, commercial | High (configurable) | Yes (SDK/API) | Workflow automation; limited/no native AI | Large, corporate | Syndicated loans, risk, reporting | Hybrid |

| Temenos | Retail, commercial, corporate | High (configurable) | Yes | High | Global banks, retail, commercial | Loan origination, risk, compliance | Cloud/On-prem |

| Fiserv LoanServ | Consumer, commercial, multifamily, mortgage | Medium (configurable) | Yes (APIs, SDK) | Medium | Mid/Large lenders | Servicing, investor management | Hybrid |

| nCino | Commercial, SME | Medium-High (configurable) | High | High | Banks, credit unions | Portfolio management | Cloud |

| ICE Mortgage Encompass | Mortgage | Medium (Salesforce-based configuration) | Yes | Yes | Mortgage lenders (IMBs, banks, credit unions) | Strong submodules in analytics | Cloud |

| Nortridge Software | Consumer, auto, commercial, specialty finance | Medium (configurable) | Limited | Low | Specialty finance, consumer | Servicing, payment plans | Cloud |

| Calyx Software | Mortgage | Medium (configurable) | Limited | Medium | Mortgage lenders | Mortgage origination | Cloud/On-prem |

When comparing the strongest loan management solutions on the market, a single "one-size-fits-all" ranking is not always the most accurate approach. These platforms can differ fundamentally in scope, implementation complexity, and the type of institution they are designed to serve. Some products are built as enterprise-grade ecosystems for large banks, with advanced governance, scalability, and deep integration capabilities, while others are optimized for faster adoption and practicality in smaller or mid-sized organizations.

For that reason, we structured this list into two primary groups.

- Loan management software for non-bank lenders and mid-sized banks

- Enterprise banking loan management platforms

Platform descriptions have been compiled and updated based on vendor-published materials and independent reviews accessible to the public, accurate as of April 2026.

Best Loan Management Software for Non-Bank Lenders and Mid-Sized Banks

This group covers platforms that are often validated as a practical fit for mid-sized banks and non-bank financial institutions. They tend to emphasize modular adoption, faster adaptability, API-driven integration, and broad lifecycle coverage, with flexibility for configuration and customization depending on the operating model.

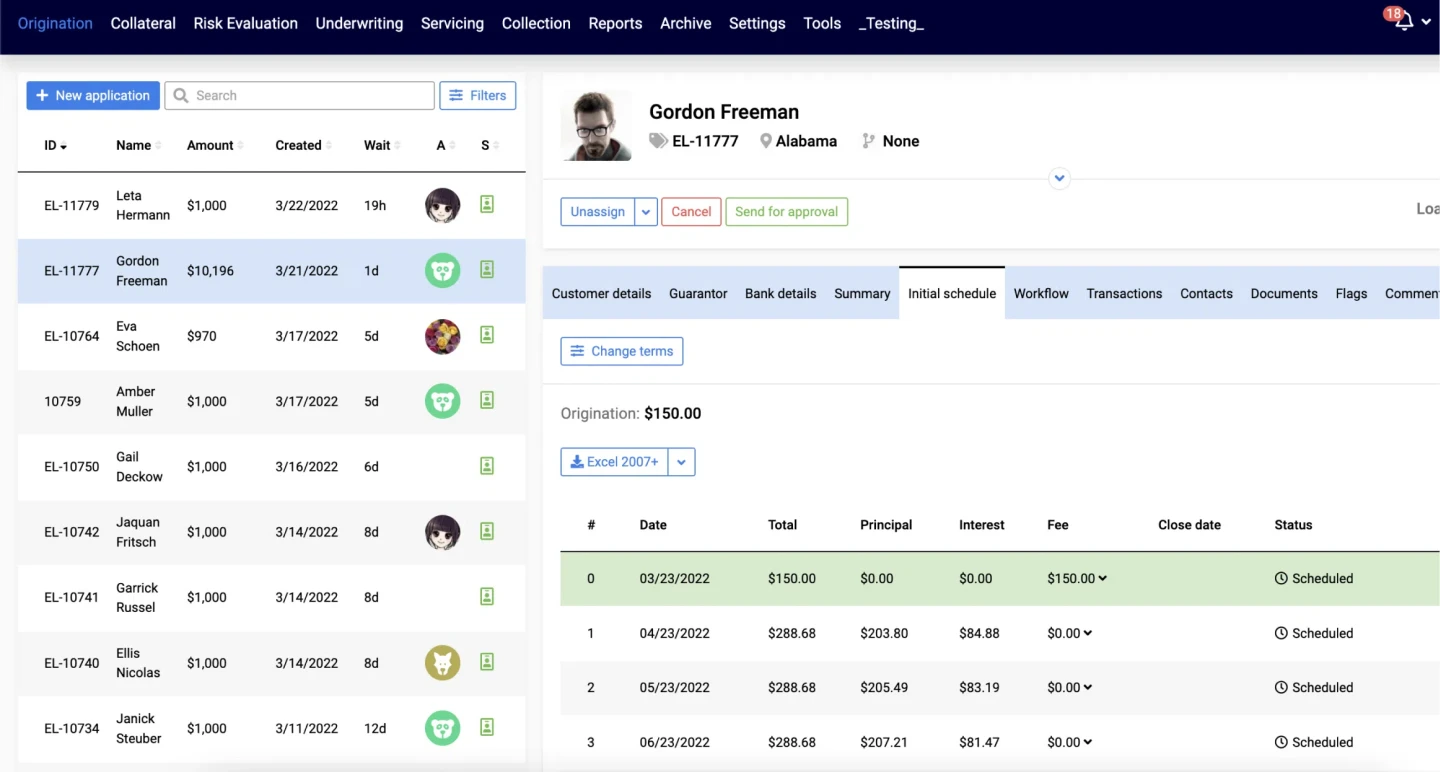

- HES LoanBox—a modular lending platform positioned around loan management with coverage across origination/servicing/collection, typically aligned with configurable deployments. Best for alternative lenders and mid-sized banks.

- Mambu—a cloud-native lending engine used by banks and fintechs to build and run loan products on a composable, API-friendly foundation.

- TurnKey Lender—digital lending automation with loan management/servicing and collections capabilities, often selected by non-bank lenders and mid-market teams.

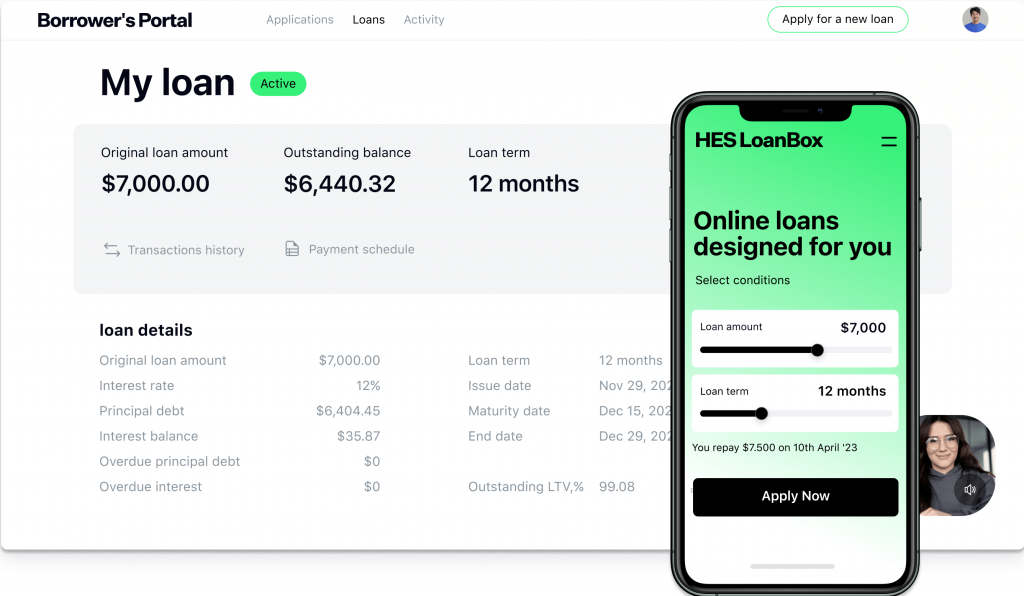

HES LoanBox: API-first modular lending platform, best for alternative lenders and mid-sized banks

HES LoanBox is an end-to-end loan management and loan servicing platform designed to connect digital onboarding, loan origination, servicing operations, and debt collection within one configurable environment. Its value is not only in covering multiple stages of the loan lifecycle, but in keeping borrower data, configurable workflows, decisions, repayments, and collection actions connected across the same operational system.

Best for lenders and financial institutions that need end-to-end, configurable loan management software with deep flexibility across onboarding, origination, servicing, and collections — especially when the project requires complex workflows, unique product logic, or extensive integrations with credit bureaus, payment rails, and accounting platforms.

Top-rated loan management software on G2, ranked #2 among all loan servicing software products of 2026, outperforming the vast majority of competitors.

| Overview | |

|---|---|

| Impact and decision quality | Up to 2.5x faster processing and 3.5x higher decision accuracy compared to conventional setups. |

| Security | Bank-grade security approach supported by ISO 27001 certification, support for AML/KYC-related processes. |

| Customization & implementation flexibility | The platform is positioned around deep configurability across complex projects: configurable underwriting logic, configurable approval rules, configurable product engines, and bespoke borrower journeys. Composable architecture enables phased module rollout or full end-to-end deployment. |

| Supported lending models | Supports a broad range of lending models, including SME lending, BNPL, Merchant Cash Advance (MCA), auto lending, consumer lending, mortgage, microfinance, and other lending types. |

| Tech stack, vendor independence & scaling | Connect with 100+ APIs, including credit bureau data providers, CRMs, payment gateways, ACH and card rails, accounting systems, and internal tools. Built on open-source technologies such as Java and Camunda — reduces vendor lock-in and dependency on a single provider. Optional developer license. |

Key features:

- Compliance-ready digital onboarding & KYC/KYB: includes all the tools for collecting borrower data, managing documents, and supporting identity/business verification flows.

- Loan origination management + AI-powered credit decisioning: applications automation, document handling, credit scoring, approvals, and disbursement in one process, enhanced with configurable AI models generating real-time risk scores and decisions.

- Loan servicing and collection: repayments, rescheduling, delinquency tracking, automated payment collection combined with AI-driven segmentation, predictive analytics, multichannel outreach, and compliance-aware strategy execution.

- Configurable product engine: support launch of any loan type with flexible terms, interest rates, fees, and repayment schedules through configuration rather than custom code.

- Self-service borrower portal: gives clients more control and flexibility with tracking their applications, loan terms, payment schedules, applying for restructuring, and other tasks.

- Platform infrastructure (multi-entity, integrations, security, analytics): support for multiple entities, currencies, and jurisdictions; 100+ API integrations (KYC/AML, credit bureaus, payments, etc.); ISO 27001 and SOC 2 certified development, encryption, audit trails; real-time dashboards and BI for KPI and portfolio tracking.

Main pros

- Projects can start from 3–4 months, depending on complexity, integrations, and customization scope.

- Reduced classic vendor dependency, with developer license (code access) available for deeper control and extensibility.

- Modular rollout (individual modules) or a full end-to-end deployment, including white-label options for customer-facing portals, applications, and digital journeys.

- High level of customization across workflows, products, rules, roles, and UI.

- Automation support for lender- and borrower-facing processes across onboarding, origination, servicing, and collections with no-code tools, multi-workflow support, and role-based access control.

Cons

- Broad platform scope: some niche requirements may require configuration or customization rather than out-of-the-box coverage.

- Implementation effort variability: timelines and workload depend on integrations, data migration, regulatory needs, and product complexity.

- Configuration governance: extensive flexibility increases the need for clear change control, documentation, and testing to avoid configuration sprawl.

The features listed represent a summary of publicly and internally documented capabilities but do not cover the full scope of HES LoanBox’s functionality.

What users say

On Capterra, where HES LoanBox is the №1 leader in the loan servicing software category, reviewers often describe the platform as a 'turnkey out-of-the-box solution' and highlight ease of configuration and integrations. HES LoanBox also ranks as the №2 leader in the loan management category on G2 by user count and rating, with users emphasizing flexibility, multi-entity and multi-currency capabilities, and the ability to connect with local banks and data vendors.

Some clients admit they had challenges with complex custom reporting, customization of dashboards and user roles at the start of deployment, and initial configuration (those activities needed extra development, planning, and coordination of the in-house team and the vendor).

Reviews are based on publicly available feedback.

Demo and trial period: free demo and trial available.

Notable clients: ID Finance, Fintuinity, Wa’ed, Alraedah, and others.

Pricing: Licence starts from $39K/year, depending on business type. Typically, a fixed subscription model with no limits on users, products, or applications. Custom enterprise licensing available for multi-entity deployments. No vendor lock-in.

Link to the product: here

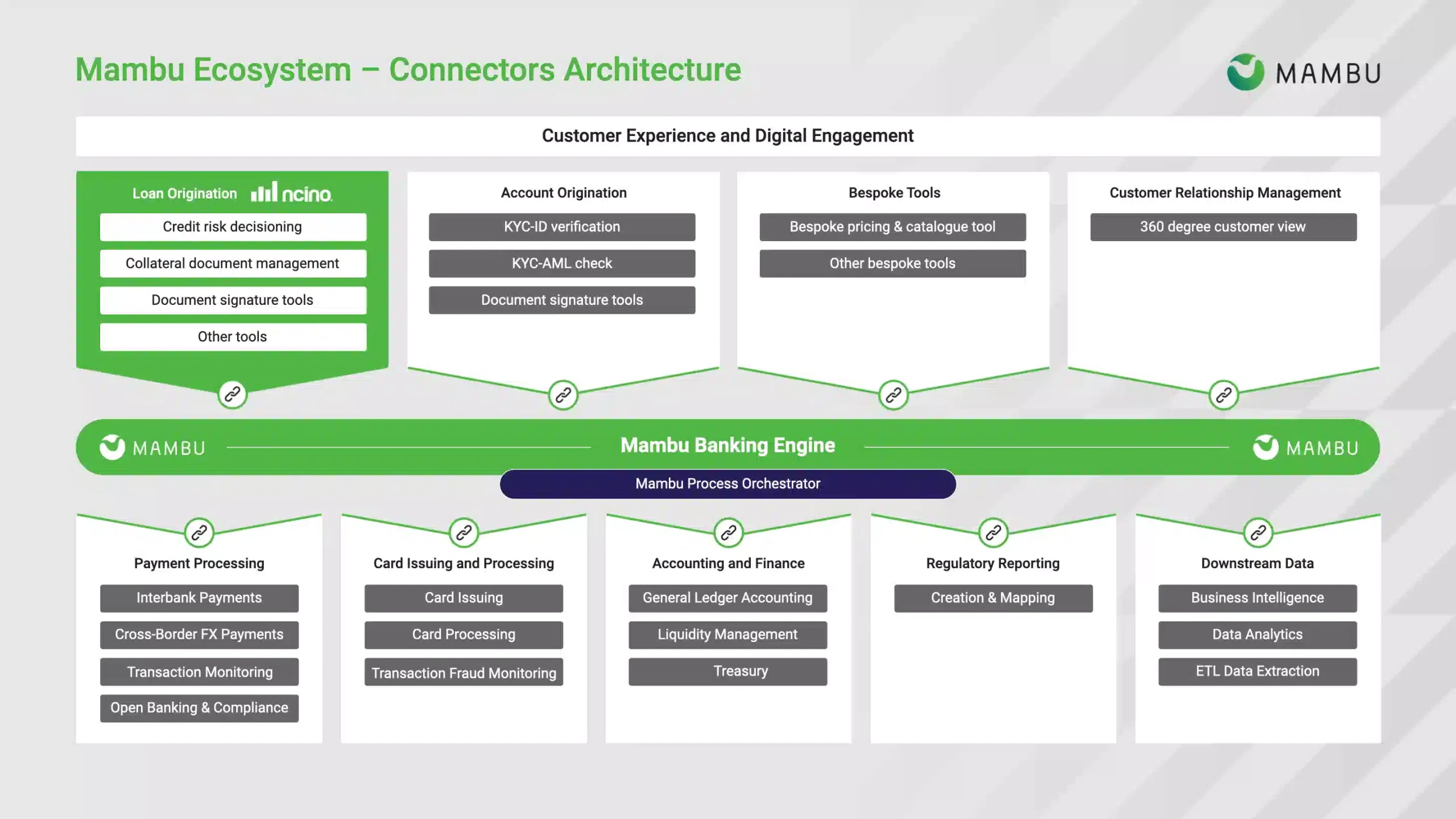

Mambu: Composable lending core for digital banks and embedded finance

Mambu is a cloud-native, SaaS banking and lending platform built around a composable, API-first architecture. Its configurable engine is suited for creating and managing a wide range of loan products, while allowing numerous third-party integrations for onboarding, decisioning, payments, analytics, and adjacent banking capabilities. Designed with fintechs, digital banks, and fast-scaling lenders in mind, it promotes speed, flexibility, and cloud-first operations.

Ideal for

Banks, fintechs, credit unions, retailers, and embedded-finance providers seek a modern cloud lending core with strong configurability and ecosystem connectivity, particularly when they prefer a composable architecture over a heavily integrated native platform.

| Overview | |

|---|---|

| Impact and implementation speed | 60–80% reduction in time to market, products can launch in 6–12 weeks. |

| Security | Banking-grade controls, including ISO 27001 certification, SOC 1 and SOC 2 compliance, biannual penetration testing, and strong operational resilience. |

| Deployment options | Fully managed in the cloud (supports deployment across AWS, Google Cloud, and Microsoft Azure.) |

| Customization & implementation flexibility | Modular architecture that supports low-code/no-code APIs, various product configurations, and rapid product design without heavy custom infrastructure. |

| Supported lending models | Supports a wide range of lending use cases, including embedded finance, BNPL, mortgages, SME lending, purchase finance, business lending, asset finance across banks, fintechs, retailers, and corporates. |

| Tech stack, vendor independence & scaling | API-first, cloud-native, and composable platform with REST APIs, webhooks, orchestration options, and a broad partner ecosystem for connecting identity, AML, payments, risk, and other services. |

Key features:

- Cloud-native lending engine: allows building and managing multiple loan offerings on a SaaS platform designed for scale and agility.

- Composable and API-first product architecture: tailored lending products can be created through configuration, not only custom development.

- Flexible loan product setup: possibilities to configure multiple loan types, payment options, due dates, repayment schedules, payment holidays.

- Low-code workflow and product configuration: products are flexibly launched and updated with low-code tooling and APIs.

- Security and compliance foundation: ISO 27001, SOC reports, embedded security processes, and resilience controls.

- Payments adjacency: for institutions that need broader financial infrastructure, Mambu offers payment orchestration through Mambu Payments.

The features listed represent a summary of publicly documented capabilities and do not cover the full scope of Mambu’s functionality.

Pros

- Cloud-native / SaaS positioning with strong security and no legacy-style deployment framing.

- Quick deployment and rapid launch cycles — products can launch in weeks.

- Comprehensive developer tools, configurable APIs, composable architecture, and broad partner ecosystem.

- Scalable for fintechs, digital banks, and microfinance organizations that need to launch and iterate configurable loan products quickly.

Cons

- Some capabilities may depend on partner integrations rather than one native out-of-the-box stack.

- Architecture, speed, and flexibility win over deeply detailed native operations stack in one place.

- Requires technical expertise for full customization, especially with third-party integrations.

- No on-premise option: may matter for institutions with strict hosting requirements.

What users say

Official Mambu case studies emphasize rapid launches, IT cost reduction, and efficiency gains. Though public reviews are scarce, clients highlight flexibility, scalability, and faster product development. Among the drawbacks, clients mentioned unwieldy migration. Also, some wished for a better interface.

Reviews are based on publicly available feedback.

Demo and trial period: free live demo upon request.

Notable clients: Wio Bank, BancoEstado, Platcorp, Esperanza, My Community Finance, Ashman.

Pricing: Available upon request. Typically subscription-based SaaS pricing with module-based and usage-based components depending on portfolio size and product mix.

Link to the product: here

TurnKey Lender: All-in-one lending automation engine for fintechs and non-bank lenders

TurnKey Lender is an AI-powered end-to-end lending automation platform designed to automate the entire lending journey in one environment: loan origination, underwriting, servicing, debt collection, and reporting. The company positions it as infrastructure for non-bank, embedded, and traditional lenders, with strong emphasis on configurable workflows, proprietary decisioning, broad automation coverage, and relatively rapid deployment.

Ideal for

Banks, credit unions, consumers, commercial lenders, and embedded lenders that need a single lending operations platform with automation and broad product-type coverage. Turnkey Lender appears suitable for lenders seeking a comprehensive operational scope, encompassing origination, servicing, and collections.

| Overview | |

|---|---|

| Implementation impact | 90%+ automation for lending tasks, 5–12% more approvals, 20–50% more repaid loans. |

| Security | ISO, SOC 2 Type 2, PSI, OWASP-aligned security, fraud prevention, and support for AML/KYC-related processes. |

| Deployment options | Primarily cloud-based (SaaS) with limited reports of on-premises/hybrid options. |

| Customization & implementation flexibility | Configurable application flows, decision rules, credit products, white-label interfaces, modular automation. Separate modules for origination, servicing, underwriting, collection, and enterprise customization. |

| Supported lending models | Supports a range of lending use cases, including consumer, commercial lending, embedded, and bank lending, accounts receivable financing, equipment finance, payday/microfinance, leasing, P2P lending, credit cards, and nonprofit credit. |

| Tech stack, vendor independence & scaling | 75+ preconfigured integrations. Multi-user scalability, multi-currency support, audit trails, white-label portals, and broad API coverage across front-office and payments-related operations. Proprietary AI decision engine. |

Key features:

- End-to-end lending automation: origination, underwriting, booking, servicing, collection, and reporting workflows are covered in one platform.

- AI-powered decisioning: proprietary machine learning credit scoring and decision automation.

- Flexible credit product builder: terms, fees, taxes, schedules, rates, and decision policies can be configured for multiple loan products.

- Loan servicing automation: automated schedules, reminders, fees, collections workflows, and performance tracking.

- 75+ integrations + API management: lenders can connect credit bureaus, KYC/AML, payments, e-signature, notifications, accounting, and other tools.

- Reporting and analytics: dynamic configurable reports and portfolio analytics.

- Multi-currency/multi-language support: the system supports multiple currencies and 10+ country editions.

The features listed represent a summary of publicly documented capabilities and do not cover the full scope of Turnkey Lender’s functionality.

Pros

- Broad end-to-end lifecycle coverage across origination, underwriting, servicing, collection, and reporting with seamless borrower experiences.

- Wide credit-product coverage: the core platform can support products, which is valuable for lenders with diverse portfolios.

- Modular design: lets the vendor match the specific client’s needs.

- Strong operational value: the platform offers automation of payment processing, document management, and borrower communications, leading to reduced manual work and fewer errors.

- Security and compliance posture: the company highlights ISO 27001 and SOC 2 Type II compliance, which is a crucial point for enterprises.

- Fast time-to-market with cloud deployment, claimed as taking a 2-months’ time.

- Strong integration and scaling capabilities.

Cons

- Deployment speed and requirements management appear to vary by package and customization/configuration scope.

- Along with cloud deployment, official materials rarely mention deployment on the lender’s servers.

- Despite open-source foundations and extensibility, the company’s public materials hardly mention deep technical transparency.

What users say

Official customer quotes emphasize convenience, automation, and centralized operations, as well as responsive support team, while case studies also cite two-month tailored deployments. Occasionally, users experience poor performance due to a learning curve and some delays in customized feature requests.

Reviews are based on publicly available feedback.

Demo and trial period: TurnKey Lender offers a demo/intro call. No information about public demo is available.

Notable clients: Windmill Microlending, Cash Direct, U.S. Black Chambers, Money Managers, Zilingo.

Pricing: Available upon request. TurnKey Lender offers several licensing models based on portfolio size and platform functionality — typically subscription-based with module-based and per-loan components.

Link to the product: here

Top Best 4 Enterprise Banking Loan Management Platforms

This group includes platforms typically selected by large banks and enterprise lenders with complex operating models. The solutions here are commonly associated with high governance requirements, large-scale deployments, deep integration landscapes, and support for sophisticated product structures and portfolio servicing at volume.

Finastra Fusion Loan IQ: Complex loan servicing engine for corporate and syndicated lending

This enterprise-class platform specializes in commercial and syndicated loan portfolio management for multinational banks. It’s built for large institutions to meet their structural capabilities and high-volume servicing needs with rigorous risk management.

Key features:

- Complex loan structuring and servicing

- In-depth risk management and reporting

- Advanced workflow customization with SDKs and APIs

- Tailored support for syndicated and large corporate loans

- Integrations with treasury and accounting systems

The features listed represent a summary of publicly documented capabilities and do not cover the full scope of Finastra’s functionality.

Pros

- Can handle the complexity of syndicated and shared loans

- Highly customizable for institutional workflows

- Strong compliance and risk analytics reputation

- Global deployment support

Cons

- Requires a Salesforce platform license, which increases total cost.

- Relies heavily on Salesforce infrastructure, which might limit customization flexibility.

- Out-of-the-box functionality is limited for non-commercial loans, which can limit agility.

Pricing: Available upon request. Typically enterprise licensing with implementation fees, sized to institution complexity and deployment scope.

Temenos: Full-scale banking platform with integrated lending for global institutions

A full-scale banking platform that offers fairly comprehensive loan origination and servicing capabilities. It has been widely adopted across Europe, Asia, and emerging markets for commercial lending.

Key features:

- End-to-end loan lifecycle management

- Integrated risk and compliance modules

- Multi-channel digital onboarding and servicing

- Advanced analytics and AI for credit scoring

- Core banking integration

The features listed represent a summary of publicly documented capabilities and do not cover the full scope of Temenos functionality.

Pros

- Strong presence in global markets, especially trusted in Europe

- Highly customizable for a wide range of lending products

- Deep regulatory compliance support across jurisdictions

- Scalable cloud and on-premises deployment options

Cons

- Complex implementation process that requires expertise

- May require significant investment for smaller financial institutions due to cost of ownership

- Mixed feedback on support responsiveness and system bugs

Pricing: Available upon request. Typically enterprise licensing with module-based components; on-premise deployments include separate infrastructure costs.

Fiserv LoanServ: Portfolio servicing infrastructure for high-volume lenders

One of the more mature options on the fintech scene, LoanServ is a full-service loan management platform that covers consumer, commercial, and multifamily loan portfolios with end-to-end automation. It’s trusted by organizations that need compliance, investor reporting, and reliability.

Key features:

- Full-cycle services for mortgages, consumer loans and more

- Automated servicing and payment processing

- Investor reporting and audit capabilities

- Default and loss mitigation management tools

- Integration with core banking, accounting, and treasury systems

- Configurable business rules and workflow automation

The features listed represent a summary of publicly documented capabilities and do not cover the full scope of LoanServ’s functionality.

Pros

- Tried and trusted solution for high-volume lenders

- Extensive servicing and collections capabilities

- Supports hybrid cloud and on-premises deployments

- Compliance and investor reporting features

Cons

- The user interface can feel a bit dated and overcomplicated

- Implementation and upgrade cycles may be lengthy and require training

- Mixed sentiment over support features

Pricing: Available upon request. Typically per-loan or per-account pricing combined with subscription components for high-volume servicing portfolios.

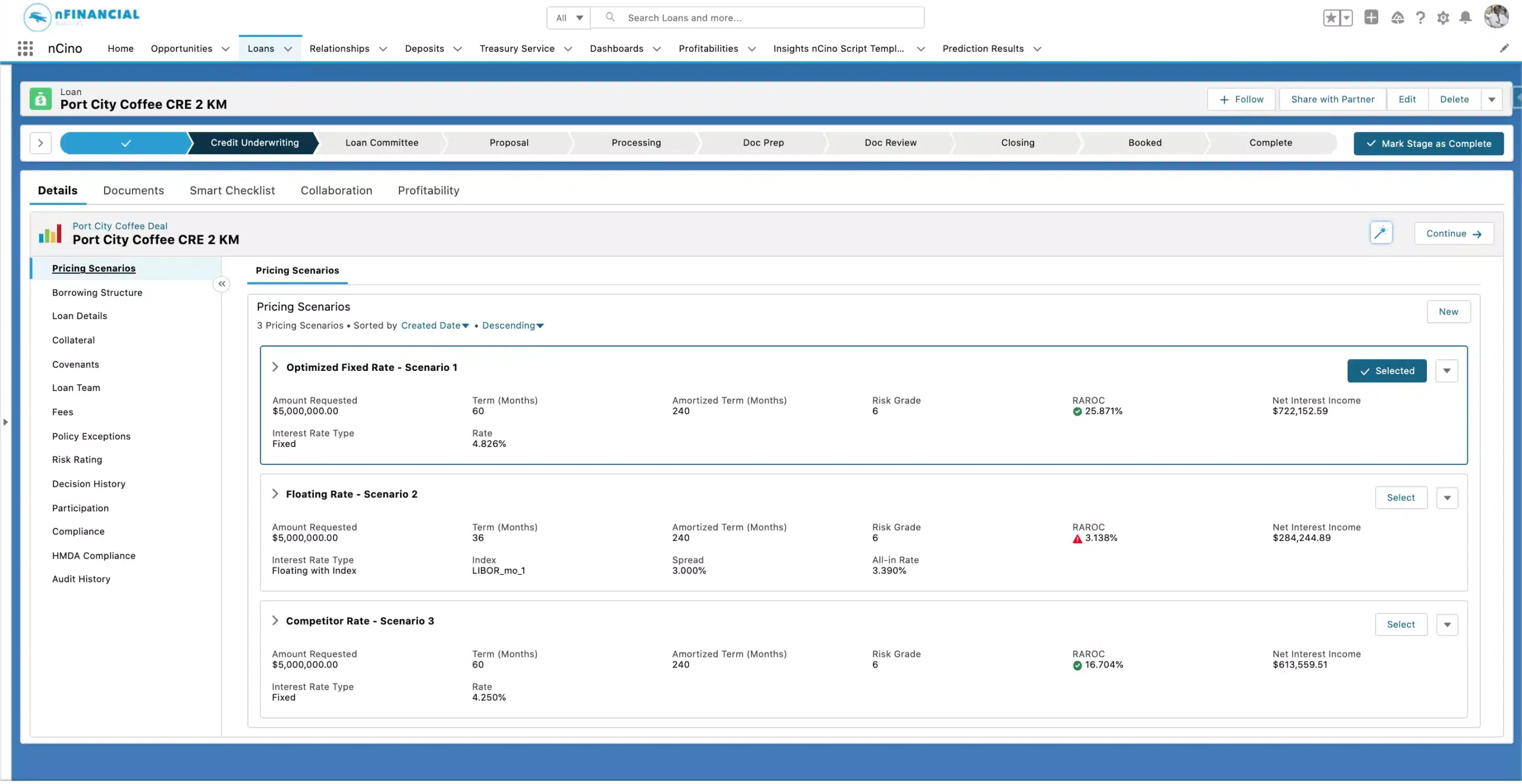

nCino: CRM-driven lending workflow platform for commercial banking

Built on Salesforce, nCino is a cloud-based solution for commercial lending and portfolio management. This platform mainly focuses on enhancing banking CRM and digital workflows and less on being a jack-of-all-trades.

Key features:

- Loan origination and underwriting workflow automation

- Portfolio and risk management dashboards

- Compliance and audit trail automation

- Salesforce ecosystem API integrations

- Loan product configuration

The features listed represent a summary of publicly documented capabilities and do not cover the full scope of nCino’s functionality.

Pros

- Seamlessly integrates with Salesforce

- Works well for commercial and SME lenders

- Has adaptive workflows and real-time reporting

- Wide partner ecosystem and developer support at all stages

Cons

- Requires a Salesforce platform license, which increases total cost.

- Relies heavily on Salesforce infrastructure, which might limit customization flexibility.

- Out-of-the-box functionality is limited for non-commercial loans, which can limit agility.

Pricing: Available upon request. Subscription-based licensing requires a separate Salesforce platform license, which adds to total cost of ownership.

Common Pricing Models for Loan Management Software

Pricing in this market varies significantly depending on deployment scope, implementation complexity, product coverage, integration needs, and transaction volumes. There is no single pricing model that is universally better—the right option depends on each lender’s operating model, growth plans, internal resources, and expected scale.

The most common pricing models include:

Fixed subscription fee—a recurring monthly or annual platform fee, typically used in SaaS-based deployments and often preferred for cost predictability.

Implementation fee—a one-time charge covering setup, configuration, integrations, migration, testing, and go-live support. This is common for platforms with broader workflow and customization scope.

Usage-based pricing—fees tied to actual platform consumption, such as application volume, active accounts, processed payments, or API usage. This model can align costs more closely with business activity. Account- and transaction-based fees are also widely used in financial software markets.

Per-loan or per-account pricing—costs linked to the number of originated, serviced, or active loans/accounts on the platform. This model is often easier to map to portfolio growth.

Module-based pricing—pricing depends on the specific modules selected, such as onboarding, origination, servicing, collections, scoring, or analytics, rather than the full platform.

Enterprise or custom licensing—individually structured commercial terms for larger institutions with more complex deployment, governance, security, or multi-entity requirements. Subscription-based licensing is also used in enterprise banking technology contracts.

You can also request a rough project estimation based on your business model, loan products, target markets, integrations, and deployment preferences. Even an early estimate can help clarify the likely implementation scope, pricing logic, and the most suitable commercial model for your lending operation.

Other Loan Management Solutions to Consider

This group includes strong products that are widely used in lending but are not always directly comparable to full lifecycle loan management platforms. In many cases, they are specialized primarily in origination (often mortgage-focused) and are typically deployed alongside separate servicing and collections systems rather than replacing the entire loan management stack.

Encompass: ICE Mortgage Technology

One of the world’s premier digital mortgage origination and servicing platforms. Encompass has been widely adopted by large banks and mortgage lenders for comprehensive loan lifecycle management, and is known as a mortgage industry staple. Encompass (ICE Mortgage Technology) - typically considered a mortgage loan origination system, so it fits better as "adjacent" software rather than a full LMS spanning servicing and collections as a single platform.

Key features:

- Automated mortgage loan application and processing

- Compliance-first document management systems

- Integrated closing and underwriting workflows

- Marketplace available for third-party integrations

- Developer tools, including APIs and customization frameworks for maximum flexibility

The features listed represent a summary of publicly documented capabilities and do not cover the full scope of Encompass’s functionality.

Pros

- Automation optimized for mortgage lending

- Compliance tools and regulatory support

- Extensive ecosystem

- Works with third-party tools

- Scalability for high-volume lenders and enterprises

Cons

- Niche product that is focused primarily on mortgages. It is less flexible for other loan types

- A complex onboarding process requires significant training for staff and can be less user-friendly for clients.

Pricing: Available upon request. Typically per-user or per-loan pricing for mortgage origination workflows.

Nortridge Software

Nortridge Software—categorized here because it is positioned as configurable loan management software focused on running and servicing portfolios with lifecycle visibility and workflows (often alongside an external LOS). NLS is known for its customizable workflows and ability to support diverse loan products on a single system. It’s widely used in specialty finance, consumer lending, and niche credit markets in North America.

Key features:

- Full loan servicing and portfolio management

- Configurable payment and collection strategies

- Customer communication tools integrated

- Automated invoicing and reporting

- Integration with accounting systems

- 150+ built-in reports and dashboards

The features listed represent a summary of publicly documented capabilities and do not cover the full scope of Nortridge’s functionality.

Pros

- Supports specialized loan products and small- to mid-sized lenders

- Flexible servicing workflows and payment plans

- Strong automation tools

- Caters to niche lending markets

Cons

- Smaller market presence with less brand recognition than other providers

- Limited advanced AI and automation features compared to larger platforms

- Large learning curve for users.

Pricing: SaaS pricing starts at $1,200/month; enterprise licensing available for high-volume servicing portfolios.

Calyx Software

Dedicated to mortgage loan origination and processing with some additional avenues in lending, Calyx Software primarily serves the North American market and has a strong focus on automation and regulatory compliance. Calyx Software is primarily positioned around mortgage origination/LOS workflows (broker/lender origination tooling), making it less directly comparable to full lifecycle loan management platforms.

Key features:

- Mortgage loan origination and processing tools

- Automated compliance, regulatory forms, and audit functions

- Document management and e-signature integrations

- Reporting, pipeline tracking, and workflow management

- Integrations with credit bureaus, appraisal services, and other secondary market investors

Pros

- Experienced in mortgage lending

- Comprehensive compliance automation and form accuracy

- User-friendly interface tailored to mortgage professionals

- Effective integration with mortgage investors and agencies

- Cloud platforms available for growing businesses

Cons

- Limited scope mostly deals with mortgage loan origination

- Less suited for broader loan servicing or commercial lending

- Legacy versions still exist and can be outdated

Pricing: Subscription-based pricing varies by edition (Calyx Point, PointCentral, and others); available upon request.

Loan management vs loan origination, servicing, and collections software

Loan management software often overlaps with other lending technology categories, but the scope is not identical.

Loan origination software is focused on the pre-disbursement stage: borrower intake, document collection, underwriting, approvals, and loan setup. It helps lenders decide whether a loan should be issued and under what terms.

Loan servicing software is focused on the execution of active loan agreements. It usually covers repayment schedules, billing, interest calculations, payment processing, account updates, and borrower communication during the repayment period.

Debt collection software is used when accounts become delinquent or require recovery-focused workflows. It supports reminders, segmentation, collection strategies, restructuring actions, and follow-up processes.

Loan management software sits above these layers as a broader operational framework. It may include origination, servicing, and collections modules, but its primary purpose is to help lenders manage loans as portfolio assets, monitor performance, coordinate workflows, and maintain control across the full lending operation.

Loan management vs loan servicing software

Loan management software and loan servicing software are often discussed interchangeably, but they describe two different scopes. Loan servicing software is a focused operational tool: it executes the post-disbursement work on each loan — applying payments, calculating interest, generating amortization schedules, sending statements, handling delinquency, and processing modifications. Many specialized servicing platforms (such as Nortridge or Margill Loan Manager) sit precisely in this layer.

Loan management software is broader. It usually includes a loan servicing engine but also coordinates origination, underwriting, collections, portfolio analytics, investor reporting, and compliance within one platform. In practice, lenders often choose between two paths: deploying a dedicated servicing system alongside an external origination tool, or selecting a unified loan management platform that covers both servicing operations and the surrounding lifecycle. The right choice depends on portfolio complexity, integration appetite, and how tightly servicing needs to connect to the rest of the lending stack.

Key Takeaways

- Loan management software should be evaluated as a portfolio control system, not only as a tool for automation or borrower-facing workflows.

- Strong platforms connect origination, servicing, collections, reporting, compliance, and portfolio monitoring without forcing lenders to rely on disconnected systems.

- The most important capabilities include lifecycle coverage, repayment tracking, workflow configurability, auditability, integrations, deployment flexibility, and operational visibility.

- Loan management software overlaps with loan origination, loan servicing, and debt collection tools, but its broader role is to coordinate lending operations and maintain control over active loan portfolios.

- The best platform depends on the lender’s business model, product complexity, region, internal technical capacity, and need for customization.

What Makes for the Best Loan Management Software?

The best loan management software is not defined by the longest feature list. In lending operations, value comes from how well the system maintains control across products, teams, borrower segments, repayment flows, and compliance requirements.

A strong platform should help lenders answer practical operational questions: which loans are performing as expected, which accounts require action, where repayment behavior is changing, whether workflows are being followed, and how easily the organization can adapt rules or products without disrupting the portfolio.

This is why modern loan management systems are increasingly judged by four factors: lifecycle cohesion, configurability, technical openness, and governance. Automation matters, but it only creates long-term value when it is supported by reliable data structures, clear audit trails, and flexible operating logic.

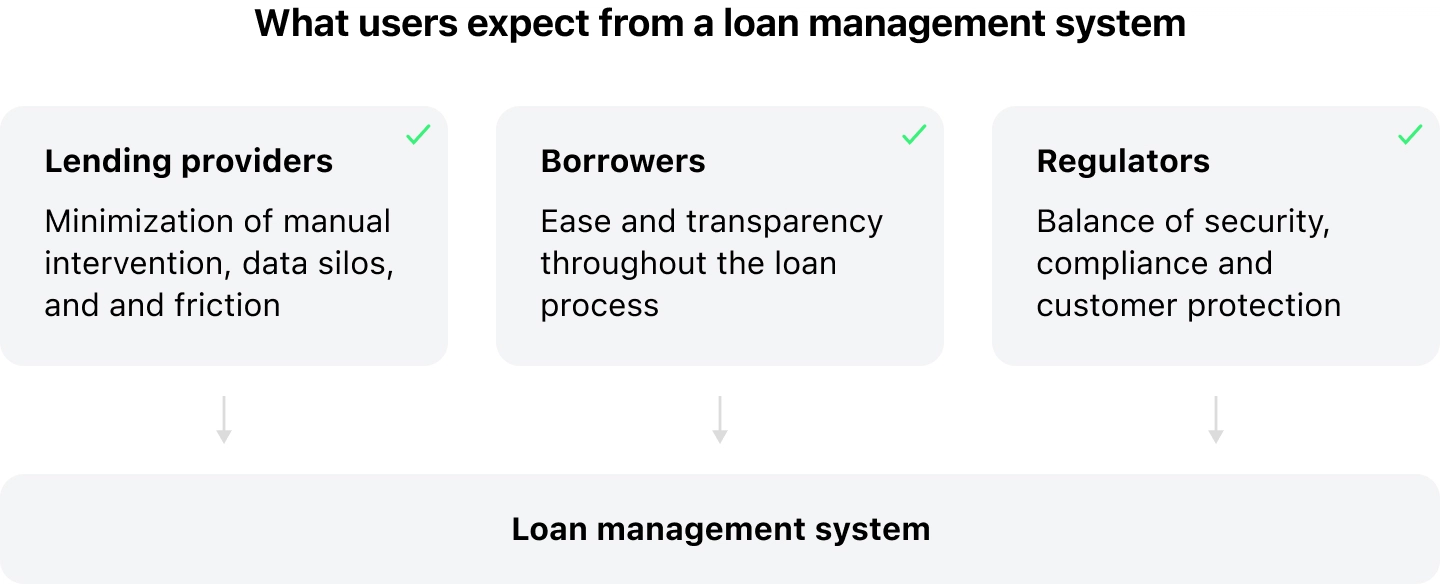

Modern lending providers aim to consolidate loan origination and servicing platforms into unified platforms to reduce manual intervention and data silos, reducing human error and friction. Meanwhile, borrowers expect ease and transparency throughout the loan process.

At the same time, regulators seek a balance of security, compliance, and customer protection—as it stands in today’s market, which includes ensuring that lending practices are fair and transparent while also safeguarding sensitive borrower information. Failing to balance these not only means customer churn, but also falling behind your competitors, higher costs, operational strain, and potentially sanctions. For lenders, that means prioritizing several components and ensuring they are woven into the fabric of their loan management systems.

What Features Should the best LMS Have?

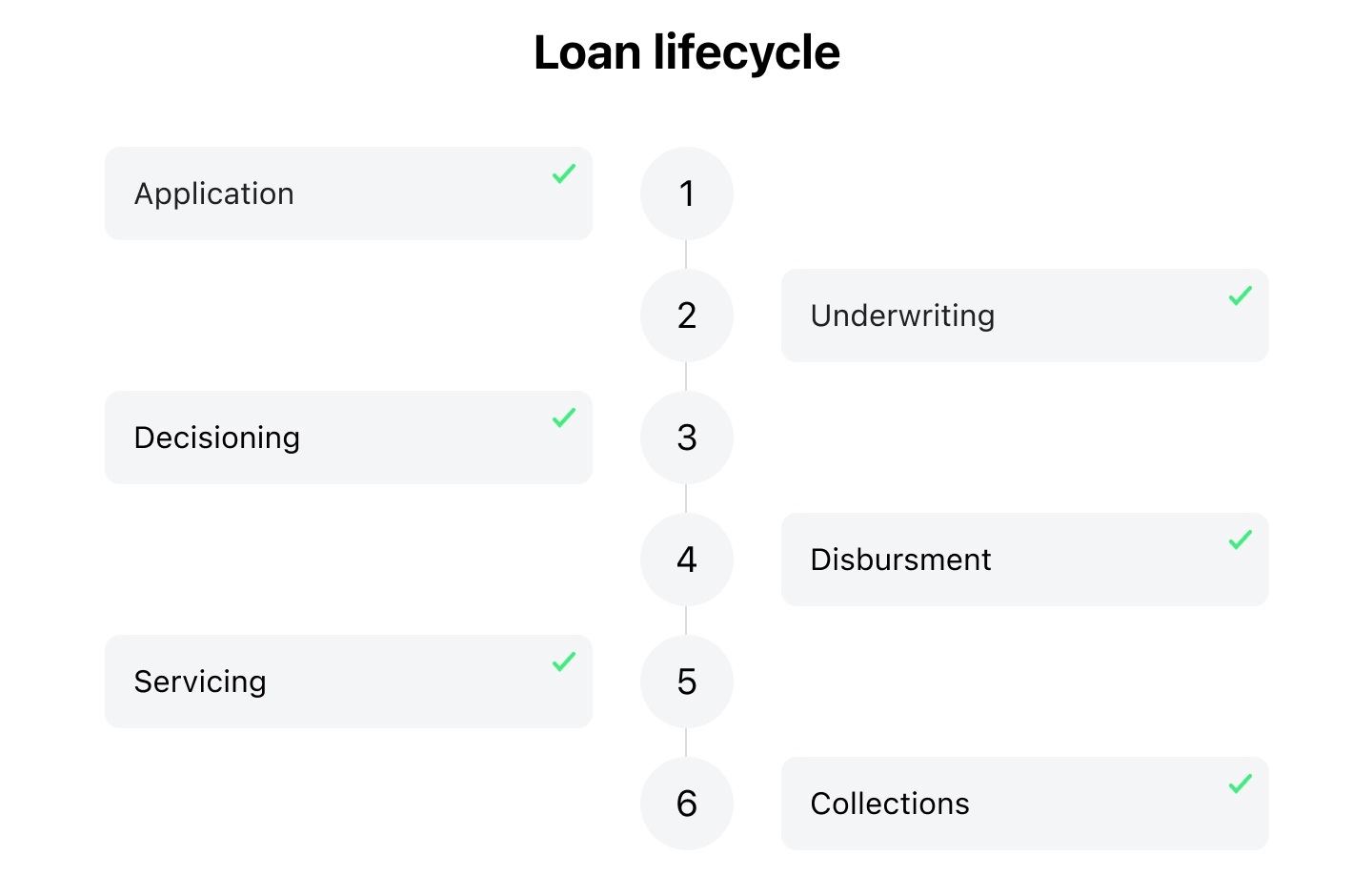

Businesses evaluating loan management software should first understand the full loan lifecycle. By mapping lifecycle stages to clear software capabilities, organizations can define the features an LMS must include.

Here’s a brief summary of the core features to be included at each stage of the loan lifecycle:

| Loan stage | Feature | Why it’s crucial | Must-have or nice-to-have | Business benefits | Development/integration complexity |

|---|---|---|---|---|---|

| Application intake | Automated onboarding | Eliminates manual data entry, reduces errors, and speeds up the start of the lending cycle. | Must-have, especially for digital-first lenders. | Higher conversion, lower operational costs, faster processing. | Medium – requires good UX, form logic, and data capture workflows. |

| Application intake | Streamlined KYC/AML checks | Ensures identity verification and regulatory compliance; reduces fraud risks. | Must-have for all regulated lenders. | Faster onboarding, reduced compliance workload, and fewer drop-offs. | Medium to High – requires integration with identity/KYC providers and meeting varied regulatory requirements. |

| Decisioning | Decisioning engine | Centralizes rules, scores and policies to produce fast, consistent outcomes | Must-have | Faster approvals; reduced bias; auditability. | Medium to High – requires APIs to bureaus/IDV, rule engine, model management and versioning. |

| Underwriting | AI-driven underwriting | Improves accuracy, consistency, and risk detection; enables faster decisions. | Becoming a must-have for competitive lenders; still optional for very small teams. | Better risk assessment, fewer defaults, ability to approve more borrowers safely. | High – needs data pipelines, model integration, explainability tools. |

| Disbursement | Flexible disbursement tools | Ensures smooth and fast loan payouts via bank transfers, cards, or wallets. | Must-have | Improved borrower experience, faster fund delivery, reduced manual work. | Medium – depends on payment processor APIs and reconciliation needs. |

| Servicing | Real-time compliance monitoring | Protects against regulatory breaches, errors, and missing documentation. | Must-have for regulated markets; strong "should-have" for fintechs. | Lower compliance risks, better audit readiness, fewer manual checks. | Medium to High – requires rules engine, monitoring logic, and up-to-date regulatory inputs. |

| Collection | Integrated debt collection workflows | Helps track missed payments, automate reminders, and recover late loans faster. | Must-have once the portfolio grows; nice-to-have for small lenders. | Higher recovery rates, early risk detection, reduced delinquency. | Variable: simple reminders = low; advanced workflows = high. |

Four Pillars of the Best LMS Systems

We’ve covered the features crucial for building a market-ready loan management system. The next step is cementing this set with a robust architecture and operating model that reliably deliver the functionality across the entire loan lifecycle.

Cohesion and Modularity

Modern platforms should unify the full loan lifecycle in one environment to reduce fragmentation, improve accuracy, and lower risk, while staying modular. In practice, this means a system with deployable modular microservices for new loan products, customizable borrower portals, easy third-party integrations, and regional compliance.

Although this may sound like somewhat of a contradiction, the logic is quite simple. While the main platform should be complex and seamless, businesses need to onboard different tools for their needs. This flexibility lets lenders scale into new products or markets without costly system rebuilds, and lowers risk to the overall business.

Developer Empowerment

This is now a core differentiator. Lending software that provides REST APIs, webhooks, SDKs, event-driven architecture, and sandbox environments helps fuel rapid innovation and scaling. Cloud-native, API-first, configurable platforms enable fintech agility and continuous evolution — adapting quickly to market changes, supporting custom servicing workflows, and allowing developers to focus on business needs that truly matter.

Artificial Intelligence

Last but not least, artificial intelligence that manages risk scoring, fraud detection, document and smart collection processing, and smart collections operations is playing a major role in the modern lending process.

When combined with advanced analytics, AI turns loan management into a smoother, automated, or half-automated process. It provides lenders with real-time insights that improve decisions, reduce defaults, and enhance borrower satisfaction and repayment performance.

Compliance and Security

Compliance and security are critical features in any lending platform and not boxes to tick. In the US alone, consumers lost over $12.5 billion to fraud in 2024. This is an almost 25% increase on the previous year’s figures. Meanwhile, Visa’s 2024 Global eCommerce Payments & Fraud Report indicated that while 82% of merchants added at least one new payment method or more in the last year, showing an interest in diversification, at the same time, 80% struggle to effectively use data and technology to improve AI/ML fraud-prevention tools.

With fraud threats expanding and operational gaps on the rise, lending systems need to support the tools to target this. Strong security, including cloud-native architecture, strict access controls, and continuous threat detection, is essential in dealing with rapidly evolving financial crime.

What to Look for When Choosing Your Top Loan Management Software?

Selecting the best loan management software isn’t all about comparing features or the tech stack. You need to be able to match your business needs to a platform and operational model, taking into account deployment preferences, enterprise size, loan product mix, geographic strategy, and a variety of other factors. This balances the market landscape, technological demand, and business needs. Let’s take a look.

- Deployment mode

- Enterprise size

- Loan type

- Geography specifics

1. Deployment mode: cloud vs. on-premises

- Cloud-based systems are leading the market due to their scalability, faster rollout time, and lower initial costs. Fintech, SMEs, online lenders, and banks moving to digital-first architectures often choose these for their flexibility. Cloud platforms enable modular updates, automatic scaling, and rich API ecosystems for agility. But they’re not perfect for everyone, as there is often reliance on a third-party data provider, and this could cause some data residency or sovereignty risks, and therefore, compliance issues.

- On-premises solutions are often preferred by large financial institutions with complex security, compliance, and legacy demands. They allow for maximum data control and deeper customization but deploy more slowly and require a large investment for any sort of development. There are often high up-front costs to consider, as well as the need to manage and monitor every step.

2. Enterprise size: SMEs vs. large institutions

- SMEs generally favor cost-efficient, cloud-first platforms. These can offer fast onboarding, automated scoring, and user-friendly workflows to reduce staffing needs and cut costs. This delivers flexibility and agility to adjust to changing business demands without jeopardizing operations.

- Large enterprises often seek out highly customizable, enterprise-grade systems with extensive integrations, diverse loan portfolio support, and scalable architectures capable of handling millions of transactions. These types are suitable for long-term sustainability, but are more rarely open to rapid development.

3. Loan type: functional pressure points

The type of loans you plan to offer will demand a different approach to your platform. This choice will impact the type of provider you choose as your vendor. Mistakes in this area could prove costly, as tech debt can be expensive to fix down the line. Consider whether you will offer:

- Personal loans: These are high-volume and require automated decisioning, instant credit scoring, and agility.

- Auto loans: Consider adding in dealer integrations, title management, structured repayment plans, and more.

- Mortgage loans: Demand complex underwriting solutions, layered compliance, and long-term servicing to manage efficiently.

- Commercial loans: These are multi-entity structures that require collateral management solutions, covenants, and syndication workflows to work effectively.

- Buy Now, Pay Later (BNPL): This approach demands real-time risk assessment, almost instant approval processes, tight merchant integrations, and flexible installment management, without compromising security.

4. Geography: Regulation, Market Maturity, and Digital Adoption

Even in an increasingly globalized world, finance is an area where location matters. This is mainly due to regulations and national laws. However, it pays to check at the beginning where your chosen platform operates and compare it to your markets.

Varying regions come with very different expectations and challenges:

- North America leads in digital adoption but enforces strict regulatory standards.

- Europe is compliance-heavy, shaped by GDPR, PSD2, and fast-moving supervisory frameworks.

- Asia-Pacific grows at a remarkable speed, driven by mobile-first banking and financial inclusion, favoring cloud-first, highly scalable platforms.

- Latin America is modernizing quickly, with fintech expansion creating demand for agile, API-friendly systems.

- The Middle East and Africa are evolving rapidly as regulatory clarity and digital infrastructure improve, offering strong long-term growth potential.

That means any software adoption has to consider its key markets closely first.

Conclusion

Choosing the best loan management software is a strategic decision critical to your company’s ability to scale, innovate, and exceed borrower and regulator expectations. In a market where almost every vendor boasts their tools are the best, it’s by being able to ask the right questions and understand the tools you need that you will be able to automate your processes most effectively.

The right choice can transform your loan management process from frustration into a growth engine that is powered by efficiency, agility, and superior borrower experiences. The wrong one can be costly. The trick is getting it right, at the right time, and with the right team and tools at your back.