Late payments and unresolved debts remain a considerable challenge for businesses, putting extra pressure on cash flow and straining relationships with customers. In response to these challenges, implementing some effective debt collection strategies has become essential to improving the recovery process for both businesses and debtors.

Modern debt collection tools come equipped with a lot of built-in features and functionalities that help enhance communication, automate reminders, and provide actionable insights. It’s no surprise, then, that businesses all over the world are eager to embrace them, with the global debt collection software market set to surpass $7.54 billion by 2031.

However, to make the most of these tools, it’s important to be open to adjusting your existing processes and to reinforce them with practical and proven debt collection methods.

In this article, we’ll provide an overview of the most successful debt collection techniques that can help businesses reduce bad debts, maintain positive customer relationships, and optimize their cash flow.

Key Takeaways

- Service-led debt collection techniques are quickly giving way to software-first, AI-powered solutions.

- SaaS and usage-based pricing are increasingly the norm, giving preference to suppliers who can expand consistently across locations and portfolios.

- Entry obstacles are growing as a result of increasing product complexity and regulatory pressure, and this is limiting the market to established and well-funded platforms.

- Together, these trends signal a shift toward using fewer, more advanced vendors that can power debt collection as a long-term operational function.

5 Key Challenges of the Debt Collection Process

Collections teams frequently stumble upon a range of hurdles that complicate debt recovery, and all of them are supposed to be addressed with modern software. Let’s take a closer look at the most pressing challenges.

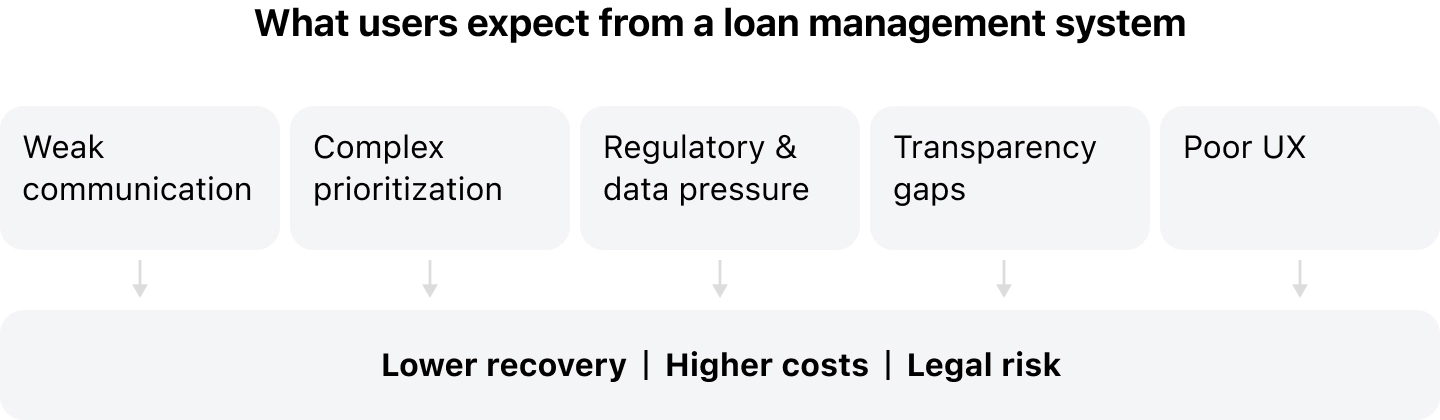

1. Poor Communication Strategy

One of the most common challenges in debt collection strategies is ineffective communication or the absence of a structured outreach plan. This means that businesses may rely on aggressive, poorly timed, or irrelevant messaging, for instance, contacting debtors through the wrong channels, sending generic reminders that disregard their specific situation, or reaching out at inappropriate hours.

Beyond reducing the chances of successful recovery, these practices can also violate regional regulations since different countries impose strict rules on the timing, frequency, and channels of debtor communications. And failing to comply with these rules, or breaking them, can lead to lawsuits, financial penalties, and serious reputational damage.

The FDCPA Annual Report 2025 points out how sensitive communication practices in debt collection are. It found that around 51% of complaints involved frequent or repeated calls, 34% concerned continued contact despite debtors’ requests to stop, 10% cited abusive language, and 5% involved calls outside permitted hours.

Electronic communication was no better, with 58% reporting repeated messages and 32% noting continued outreach despite opt-out requests.

2. Difficulty Prioritizing and Segmenting Complex Cases

Not all accounts behave the same. Some debtors are temporarily late but are willing to pay, others are high-risk or dispute-heavy, and others fall somewhere in between.

The point is that when portfolios include a mix of debt sizes, repayment capacities, communication preferences, and changing financial circumstances, it becomes difficult for collections teams to determine which accounts need immediate attention and action and which ones can move through automated workflows.

Without proper segmentation and prioritization frameworks, teams spread their efforts too thin, miss early intervention opportunities, and devote too much time to low-impact accounts.

3. Constant Regulatory Pressure and Data Privacy Risks

According to an industry study, addressing compliance requirements is a major challenge for 62% of third-party collectors and 49% of first-party teams.

Data privacy and security introduce another obstacle for businesses. When businesses don’t employ any measures to properly protect, handle, track, and document sensitive information, they might be faced with serious erosion of customer trust and credibility.

4. Transparency and Trust Gaps in Debt Collection Strategies

Debtors want to see detailed disclosures about outstanding balances, realistic timelines, and easy-to-understand fees. However, some debt collection businesses overlook this aspect, which leads to confusion, disputes, delayed responses, and growing mistrust.

What’s more, the absence of flexible payment plans that would allow customers to manage repayments according to their financial wellness as well as poorly outlined payment terms or hidden conditions, discourage engagement and increase the likelihood that accounts will remain unresolved for longer.

5. Poor User Experience

If the debt payment experience feels bewildering and inconvenient, even well-intentioned and responsible customers might postpone and/or abandon the process.

Features like unintuitive portals, vague instructions, and extra steps go against the principles of customer-centric collections and turn what should be a smooth process into a source of frustration, which can reduce repayment rates and increase both operational costs and administrative burden.

8 Most Successful Debt Collection Techniques

Now we will explore the 10 most viable debt collection tactics that can contribute to the successful debt collection process.

1. Properly Assess Creditworthiness Before Extending Credit

If you’ve been wondering how to improve collections and reduce bad debts, the key is to execute thoughtful credit decisioning right from the start. This procedure will enable you to get a better grasp of who you’re doing business with, what their financial capacity looks like, and what kind of repayment terms make sense for them. It also allows for setting more realistic expectations from day one, which reduces misunderstandings later, when payments become due.

These days, lots of businesses opt for sophisticated AI-powered credit decisioning tools to speed up the credit evaluation process and keep it consistent and unbiased. These tools can integrate with different credit bureaus and open banking, promptly analyze huge data sets, and support rule-based decisions that comply with companies’ internal risk policies and regional legislation. All of these aspects allow teams to make smarter calls that balance growth with risk management.

Most importantly, robust credit decisioning software prevents downstream issues before they begin. Responsible onboarding ensures that fewer accounts lapse into serious debt, which translates into a more predictable and manageable recovery lifecycle for everyone involved.

Key tips:

- Collect comprehensive financial and behavioral information during onboarding

- Use automated credit decisioning tools to improve speed and consistency

- Set credit limits and repayment expectations upfront

- Integrate multiple data sources for a more complete financial picture

- Reassess creditworthiness periodically as customer circumstances change

2. Work out a Comprehensive and Consistent Communication Strategy

If you want your debtors to stay engaged and not avoid contact with your business, you need to embrace one of the most effective debt collection techniques—and that is devising a well-rounded communication strategy.

Ideally, it should cover core elements such as the channels you’ll use, tone and voice, contact frequency, escalation logic, and adherence to regional regulations.

What’s more, your strategy should emphasize some other crucial aspects such as structured outreach, personalization, and an omnichannel approach.

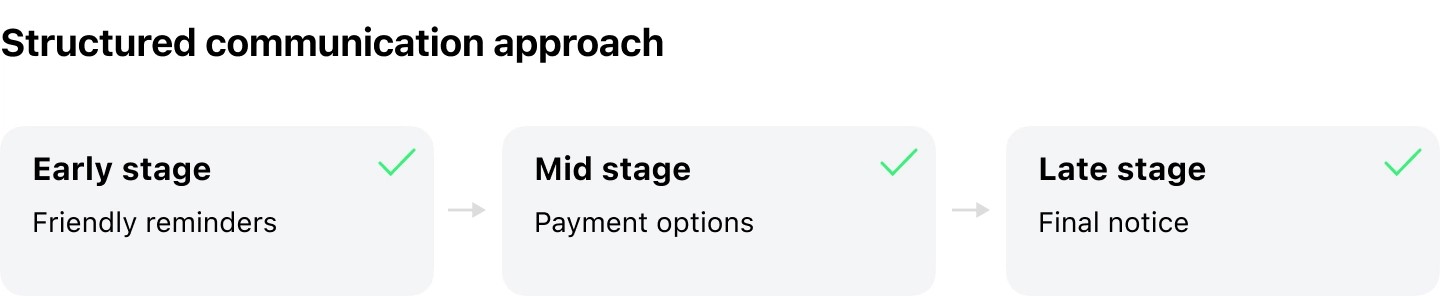

Structured outreach

Think through every stage of your communication journey. Early automated reminders should be helpful and informative, simply confirming balances and due dates. Mid-stage follow-ups can introduce payment options or more flexible arrangements, while later messages may increase urgency, without ever feeling aggressive.

Personalization

Personalization has become part and parcel in all spheres and domains, and debt collection is no exception. Generic scripts and impersonal outreach sequences miss the mark because they ignore individual context, communication preferences, and emotional realities.

That’s why one of the best collection strategy examples is focusing on ethical and personalized interactions. This implies that you should adapt tone, timing, and channels based on each customer’s behavior and their engagement patterns.

Plus, remember that personalization requires clear boundaries. Responsible behavioral nudging such as well-timed reminders or supportive check-ins can encourage action without crossing into manipulation, excessive pressure, or tactics that risk eroding trust.

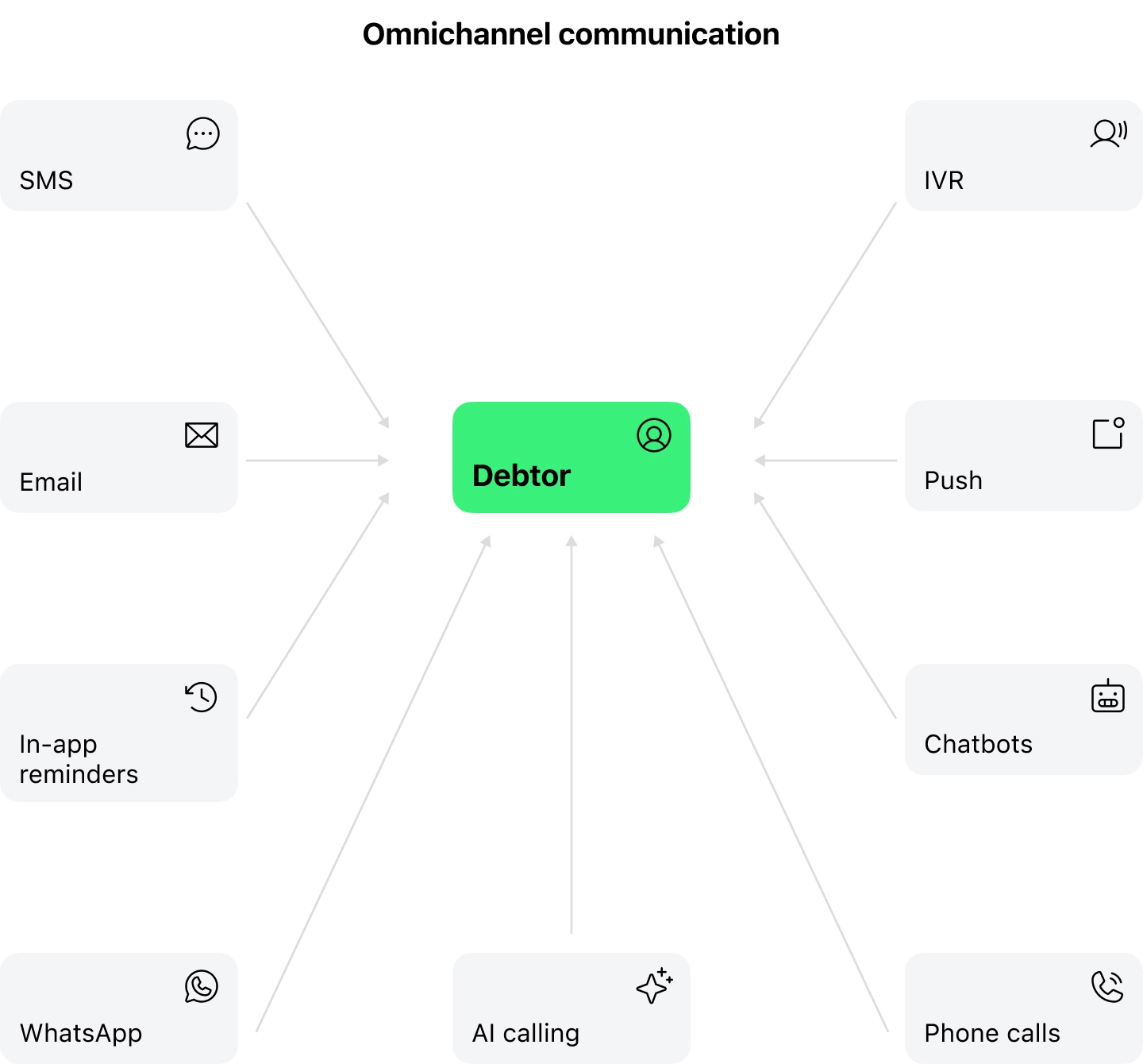

Omnichannel approach

Meeting customers on their preferred channels increases the chances that your messages are seen and acted upon. For example, Gen Z is known to prefer texting or email over phone calls, while older generations may respond better to voice contact. Thus, your omnichannel strategy should combine various channels such as SMS, WhatsApp, in-app reminders, IVR, email, push notifications, chatbots, and phone calls, using each one according to customer preferences.

The most advanced automated debt collection software includes AI calling tools that handle routine reminders and delegate more nuanced conversations to human agents. They can also adjust outreach based on results, optimizing engagement and improving overall collection effectiveness.

Key tips:

- Plan contact strategy with frequency, escalation logic, tone, and channel hierarchy in mind

- Start with structured and courteous outreach and escalate gradually

- Let customers choose or confirm preferred communication channels

- Personalize messages to customer behavior and engagement patterns, avoiding irrelevant or generic reminders

- Always adhere to regional regulations to minimize legal and reputational risk

3. Offer Easy and Flexible Payment Options

Flexible payment options increase the chances of successful debt repayment. That’s because customers tend to gravitate toward what feels most convenient and manageable. Providing a diverse range of payment methods, including online transfers, credit cards, digital wallets, and self-service portals, is one of the most effective debt collection tactics to reduce friction and encourage timely payments.

| Timing flexibility | Amount flexibility |

|---|---|

| Payment date alignment | Installment plans |

| Short-term payment deferrals | Variable installment plans |

| Grace periods | Partial payments |

| Staggered start dates | Minimum payment agreements |

Besides, if you demonstrate understanding to customers who are facing temporary financial stress, your business will be perceived as supportive and client-oriented. Therefore, consider introducing flexible options, such as customized payment plans, adjustable due dates, payment holidays, short-term deferments, and negotiated schedules. Some companies take some extra measures by freezing interest or restructuring balances to make repayment feel more attainable and less overwhelming. Plus, building in reasonable grace periods provides some customers with a necessary buffer to resolve payments without immediate pressure.

It’s also worth encouraging customers who pay early by offering small incentives for timely settlements. Introduce and integrate simple perks like modest discounts, loyalty rewards, or extended credit terms. These will act as gentle motivators and move the resolution process in a positive way.

Key tips:

- Offer multiple digital and automated payment channels

- Provide installment plans or partial payment options when needed

- Allow payment dates to align with customers’ income cycles

- Communicate payment terms, deadlines, and fees from the start

- Keep repayment negotiations open and solution-focused

4. Enable Self-Service Through Digital Portals

There are generally two types of users: those who prefer guided support and those who are more tech-savvy and perfectly comfortable managing things on their own. For the latter, self-service portals make it possible to manage accounts on their own terms. They provide direct access to balances, repayment options, account updates, and scheduling tools.

Self-service platforms, such as borrower portals, also increase transparency and reduce friction. Using them, customers can log in whenever it’s convenient for them, explore options, and take action at their own pace. Furthermore, the integrated features such as automated payment scheduling, downloadable statements, and real-time balance tracking improve usability and boost accuracy in account information.

Key tips:

- Provide balanced visibility and repayment options inside the portal

- Enable automated payments and scheduling tools

- Offer secure messaging for quick questions or clarifications

- Keep interfaces simple and mobile-friendly

- Combine self-service with easy access to human support when needed

5. Segment and Prioritize Accounts Based on Risk and Recovery Potential

Businesses first segment accounts based on factors such as debt size, account age, payment history, and responsiveness. After segmentation, they prioritize accounts to decide which need immediate attention and which follow automated workflows.

Many companies still use volume-based prioritization, focusing on the total overdue amount, while risk-based prioritization evaluates accounts more holistically, considering the likelihood of repayment and potential impact on collections. With these insights, teams can decide which accounts need immediate human attention and which can move through automated workflows.

The most advanced debt collection platforms make use of AI-driven engines that aptly analyze behavioral and transactional data to calculate propensity-to-pay scores. This makes it possible to estimate the probability of who is most likely to repay, when they are most likely to respond, and which communication channel will be the most effective for reaching them. As a result of this, high-risk or high-value accounts receive personalized attention much earlier in the process. Meanwhile, lower-risk accounts move through standardized communication sequences that maintain professionalism and consistency without requiring constant manual oversight.

| Type of segmentation | Factors businesses consider |

|---|---|

| Basic preliminary segmentation | Debt size Account age Payment history Responsiveness |

| Volume-based prioritization | Total overdue amount |

| Risk-based prioritization | Likelihood of repayment Potential impact on collections |

| AI-driven prioritization | Propensity-to-pay scores based on behavioral and transactional data |

Key tips:

- Rank accounts based on risk level and recovery potential

- Use AI-driven scoring models to guide prioritization decisions

- Focus human resources on high-impact or complex cases

- Automate outreach for lower-risk accounts where appropriate

- Continuously refine prioritization rules based on performance data

6. Centralize Data and Maintain Comprehensive Documentation

When teams have to work with information that is scattered across multiple sources, they either make or have to deal with issues such as duplicated outreach, mixed messages, missed updates, and unnecessary confusion for everyone involved. In this case, one of the most viable debt recovery strategies is centralizing all debtor data in a single system so that every staff member works from the same source of truth.

Chiefly, don’t forget to maintain comprehensive documentation. This is needed to protect both the business and the debtor, plus this creates accountability across the process, supports fair and compliant communication, and makes internal handoffs smoother.

Key tips:

- Maintain a unified system for communication logs and payment records

- Record all agreements, disputes, and account updates promptly

- Provide real-time access to data across teams

- Use documentation to support compliance and audits

- Analyze historical data to improve future strategies

Related Posts

12 Best Debt Collection Software in 2026

7. Use Data Analytics to Guide Strategy and Improve Performance

To keep abreast of risk and make smarter debt collection decisions, teams need to thoroughly analyze both portfolio-level trends and individual debtor behaviors, and data analytics is a huge help here. By tracking key metrics such as DSO and aging buckets as well as behavioral patterns and repayment history, businesses get a more vivid picture of where receivables are slowing down and which accounts are drifting into higher-risk stages.

Analytics also give teams a chance to experiment and learn. With the insights they uncover, collections teams can try out different outreach timing, channels, or messaging approaches, and see what helps drive greater engagement and repayment.

Key tips:

- Monitor portfolio performance using structured metrics like DPD

- Track which communication strategies drive the best repayment outcomes

- Use predictive analytics to identify high-risk accounts early

- Continuously test and refine outreach approaches

- Share insights across teams to align strategy and operations

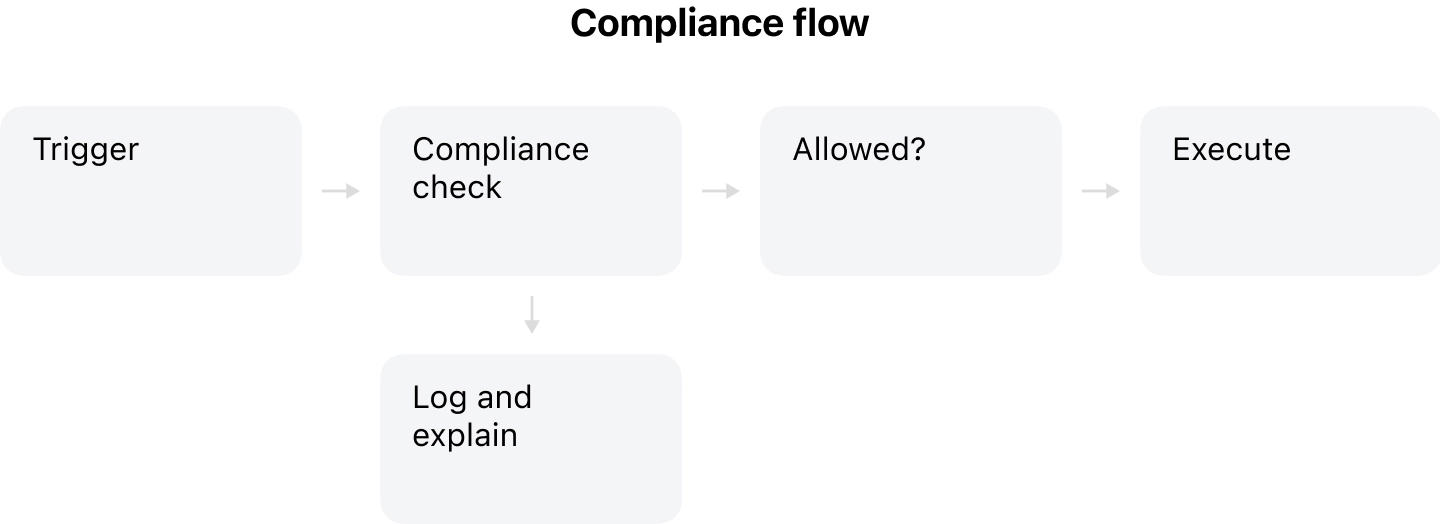

8. Embed Compliance in Debt Collection Workflows

As you know, debt collection is a highly regulated field, which means that compliance must be built directly into your operational workflow. Thus, from the moment a case enters your system, regulatory logic should guide how, when, and through which channel communication is allowed.

To make compliance actionable, your platform should enforce:

- Time-of-day call restrictions to respect regulations and debtor preferences

- Contact frequency caps to prevent over-communication

- Jurisdiction-specific rules for timing, consent, and disclosure

- Consent management to track opt-ins and preferences

- Full audit logs for all communications and data access to enable accountability and traceability

These controls help support adherence to frameworks such as Regulation F, the Telephone Consumer Protection Act (TCPA), rules set by the Financial Conduct Authority (FCA), EU Consumer Protection laws, the Australian Consumer Law (ACL), and the General Data Protection Regulation (GDPR).

Parallel to the legal obligations, take care of data security, too. This means that you have to store and manage sensitive financial and personal information in secure systems, track who accesses it, and protect it from breaches and misuse to avoid operational disruptions and reputational fallout.

Also, your business will be better off if you roll out practical safeguards such as role-based access permissions, encrypting data both in transit and at rest, turning on multi-factor authentication, keeping an eye on access logs, running regular security checks, and making sure that your teams know how to handle customer data responsibly.

Importantly, to make compliance actionable in your workflows, consider implementing the following practices:

Key tips:

- Configure communication rules before outreach begins and ensure that timing and frequency limits are enforced automatically

- Embed compliance checks directly into automated workflows

- Apply jurisdiction-based logic for disclosures, consent, and contact strategy at scale

- Protect customer data with role-based access, encryption, and multi-factor authentication

- Maintain comprehensive audit trails for traceability and dispute resolution

Conclusion

The most effective debt collection strategies in 2026 include assessing creditworthiness upfront, building a consistent communication strategy, offering flexible payment options, enabling self-service, prioritizing accounts based on risk, centralizing data, leveraging analytics for performance optimization, and embedding compliance and data security into operational workflows.

When these best practices in collections strategies are applied consistently and correctly, businesses are able to improve their operational efficiency, strengthen relationships with debtors, and build more resilient collections workflows.