With the best credit decision engines, lenders are able to handle high-volume applications with far greater accuracy, without relying on outdated manual review processes.

In fact, the popularity of specialized credit decisioning software has been on the rise, with the global market expected to reach $24.6 billion by 2033. This growth, as the report points out, can be attributed to factors such as the increasing demand for automation, enhanced risk assessment, and regulatory compliance.

In this article, we’ll outline the 8 best credit decisioning software vendors to watch in 2026 and highlight what makes each platform stand out.

How We Created This Listing

For this review, we analyzed a range of credit decisioning software providers. We focused on core capabilities: decisioning engine flexibility, support AI-driven scoring, customization possibilities, and integration options. Additional factors included scalability, ease of implementation, reporting and monitoring tools, and the availability of compliance and security information. As credit decisioning platforms can differ significantly depending on configuration, use case, and regional requirements, this list reflects a comparative overview rather than a fixed ranking.

What Is Credit Decisioning Software?

A credit decisioning system is a specialized platform that assists lenders in automating and optimizing the credit approval process.

The solution relies on advanced algorithms and analytics and brings together different data points in order to help lenders make better informed and timely credit decisions and establish a comprehensive picture of a potential borrower’s creditworthiness.

This way, lenders benefit from more consistent and efficient credit-related workflows, and borrowers enjoy quicker lending decisions.

An important aspect to highlight is that generative AI is expected to play a very active role in modern credit risk assessment.

So, according to Deloitte’s insights, GenAI is poised to introduce new capabilities across the credit risk evaluation process, including analyzing documents in context, interpreting complex policies, automatically extracting key information, and generating early drafts of credit memos.

McKinsey also highlights that GenAI tools can take over much of the legwork in the credit decisioning process. They can prepare outreach messages to request missing information from customers, compile and organize borrower data, run preliminary credit analyses, and draft sections of credit memos before an officer steps in.

More advanced agent-style GenAI systems can independently pull data from different sources, calculate ratios, compare them to relevant benchmarks, and produce concise summaries for review.

Who Uses Credit Decisioning Software

Credit decisioning software is used across the entire lending ecosystem — from traditional financial institutions to digital-first fintechs. Each segment uses it for different goals, risk profiles, and customer journeys, but the core purpose is the same: making faster, more accurate, and more transparent lending decisions.

| Lender | What they offer | Key needs from credit decisioning software |

|---|---|---|

| Banks | A wide range of retail and commercial loans | Strong compliance, integrations with core banking, high explainability, enterprise-grade security |

| Credit unions | Community-focused lending with member-first approach | Cost-effective solutions, flexible rules, easy manual review options, simple workflows |

| Fintechs | Digital-first loans with automated onboarding | API-first architecture, rapid decisioning, ML/AI support, alternative data ingestion |

| Micro-lenders | Small, short-term personal loans | Quick evaluation, low-cost processing, automated workflows, fraud detection |

| BNPL providers | Instant point-of-sale credits | Real-time decisions (<1 sec), behavioral and transactional data, high scalability, automated risk models |

| Mortgage lenders | Long-term, high-value loans | Document intelligence, deep verification tools, complex scoring rules, strong compliance audit trails |

| SME / business lenders | Loans for small and medium enterprises | Multi-source financial analysis, cash-flow-based scoring, custom underwriting rules, automation for faster turnaround |

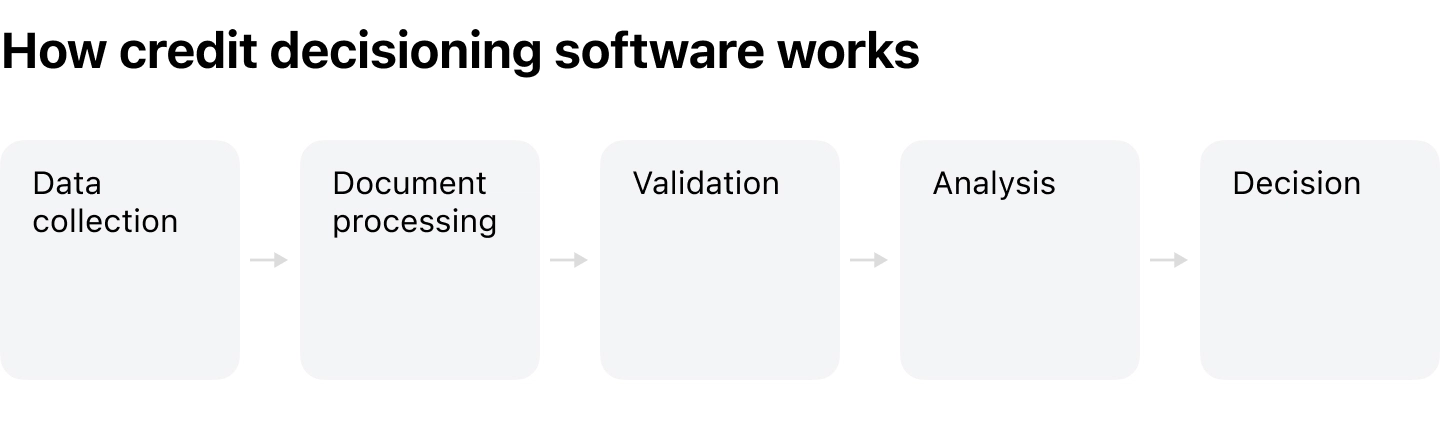

How Does the Best Credit Decisioning Software Work?

Although credit decision tools may work in different ways, the core working principles usually look like this:

1. Document collection. A credit decisioning platform gathers information from diverse data sources such as credit bureau data, financial statements, bank transaction histories (often through open banking), and any other documents that the borrower submits directly. Noteworthy is that this data is pulled automatically from external data sources and bureaus through API integrations.

2. Document processing. Once the files are collected, the software employs OCR tools, intelligent document processing, and ML-based classification models so as to convert different file formats into a clean structure and organize everything into consistent digital records.

3. Data validation. During this stage, credit decision software verifies the completeness and consistency of the submitted information, checks it against internal policy rules (for example, required minimum income, maximum debt-to-income ratio, or acceptable document types), and ensures compliance with regulatory constraints such as KYC and AML requirements. Then, if it spots any missing data, inconsistencies, or policy violations, it flags them before the credit application moves further.

4. Creditworthiness assessment. Next, it evaluates the borrower’s creditworthiness, considering ratios like debt-to-income, cash-flow stability, repayment history, credit scores, and your own custom risk rules. Importantly, to better manage risk as well as identify patterns that traditional scoring might miss, many platforms apply machine learning models, behavioral scoring, or predictive analytics.

5. Decision generation. After analysis, credit risk decisioning software compiles all results and generates a recommended decision such as approve, decline, or send for manual review. Some tools also produce draft credit memos or summaries so that credit officers can quickly understand the reasoning behind each outcome.

Best Credit Decisioning Software to Look Out For in 2026

While there are lots of the best credit decisioning software for banks available on the market, we’ve researched and selected the seven most notable options worth considering.

Let’s take a closer look at their key features and capabilities.

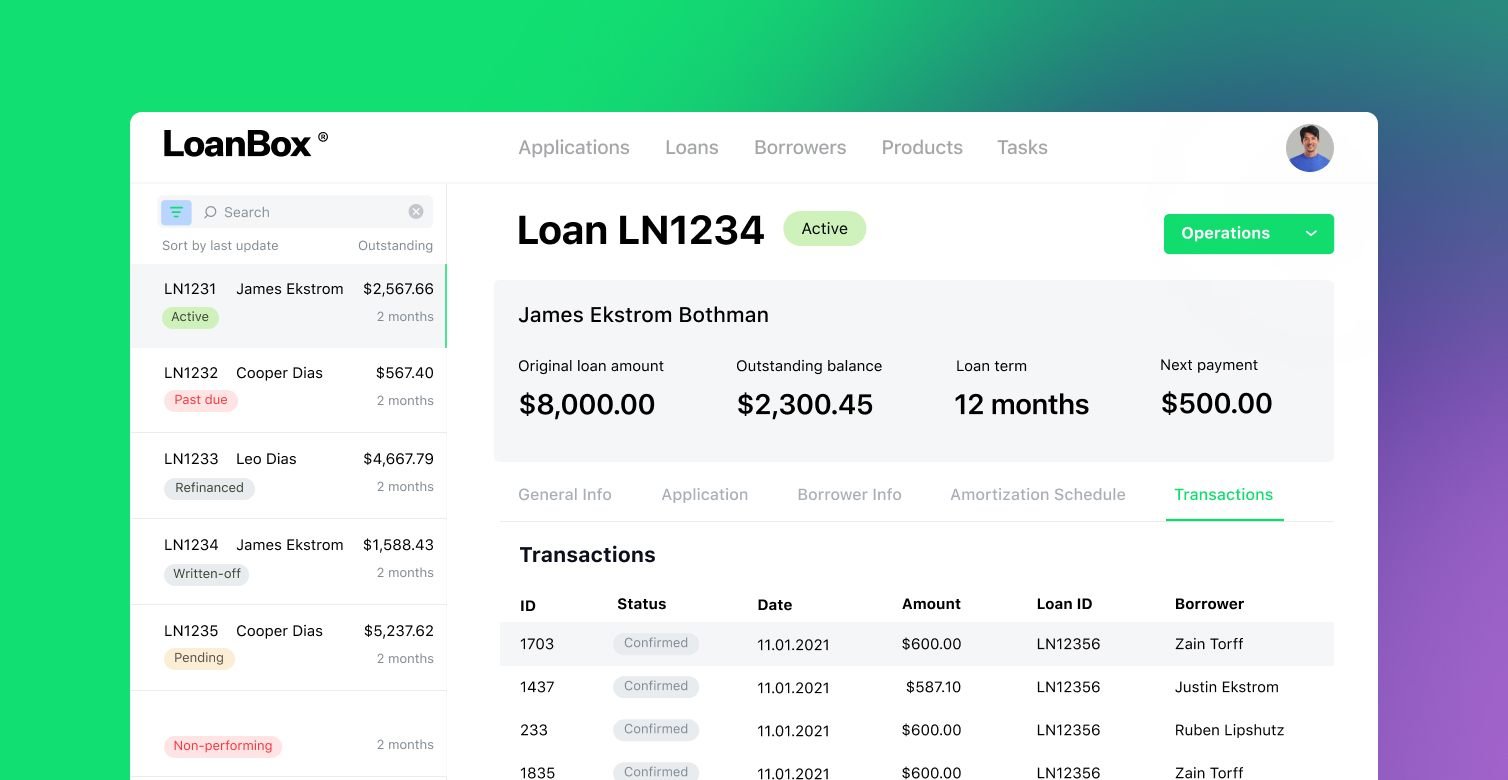

1. HES LoanBox

HES FinTech delivers HES LoanBox, an end-to-end lending platform combining credit decisioning, workflow automation, and loan management in a single customizable system.

Best suited for: Banks, fintechs, and alternative lenders that need flexibility and scalability and credit decisioning inside a broader lending operating system, not just a rules engine in isolation.

A major strength of this top credit decision software is its high level of flexibility and customizability. Unlike standalone decision engines, HES covers the full lending lifecycle, from application intake to servicing. Yet, lenders can choose to embrace the platform as a full end-to-end lending system or integrate only the modules they need (for instance, credit decisioning module), depending on their workflow, regulatory environment, or lending model. The platform also allows for flexible loan products and approval workflows. Depending on what matches their internal setup and overall business goals, lenders can opt for manual, semi-manual, or fully automated decision flows.

An AI-powered credit decision engine can be optionally included to enhance the capabilities of the internal score cards and risk modeling. Still, you are free to keep the fully rule-based or hybrid setups if you prefer. Importantly, these scoring models can be customized to your specific risk approach, business rules, and product requirements.

The platform supports rule-based decision-making and connects with multiple credit bureaus. Additionally, AI-powered scoring models can be enhanced with alternative data. All this makes decisioning more grounded and data-driven.

Built-in compliance automation feature guarantees adherence to security standards, audit requirements, and financial regulations throughout the process.

HES LoanBox is built to support multiple loan products, different borrower segments, and evolving risk strategies, which makes it a robust, future-ready, and scalable solution.

Key features:

- Modular and flexible architecture with configurable workflows and lending products.

- AI/ML-based scoring with customizable risk models

- Configurable loan products and segment-specific approval paths

- API-driven integrations and flexible deployment options (cloud, on premise, hybrid)

- Built-in compliance trails

- Advanced interactive dashboards and customizable reporting

- Advanced security with KYB/AML checks, biometric verification, OWASP-compliant infrastructure, and ISO 27001 and SOC 2 certified development.

Pros:

- Can be used both for full lifecycle control instead of fragmented tools and as specific microservices

- Has fully configurable scoring models, workflows, products and approval logic

- Flexible choice between manual, semi-automated, and fully automated workflow

- Gives full visibility into credit decisions

Cons:

- Initial configuration can take work or appear complex for early-stage fintechs and small lending teams

- As the solution is designed for configurability, UX may feel not intuitive at once

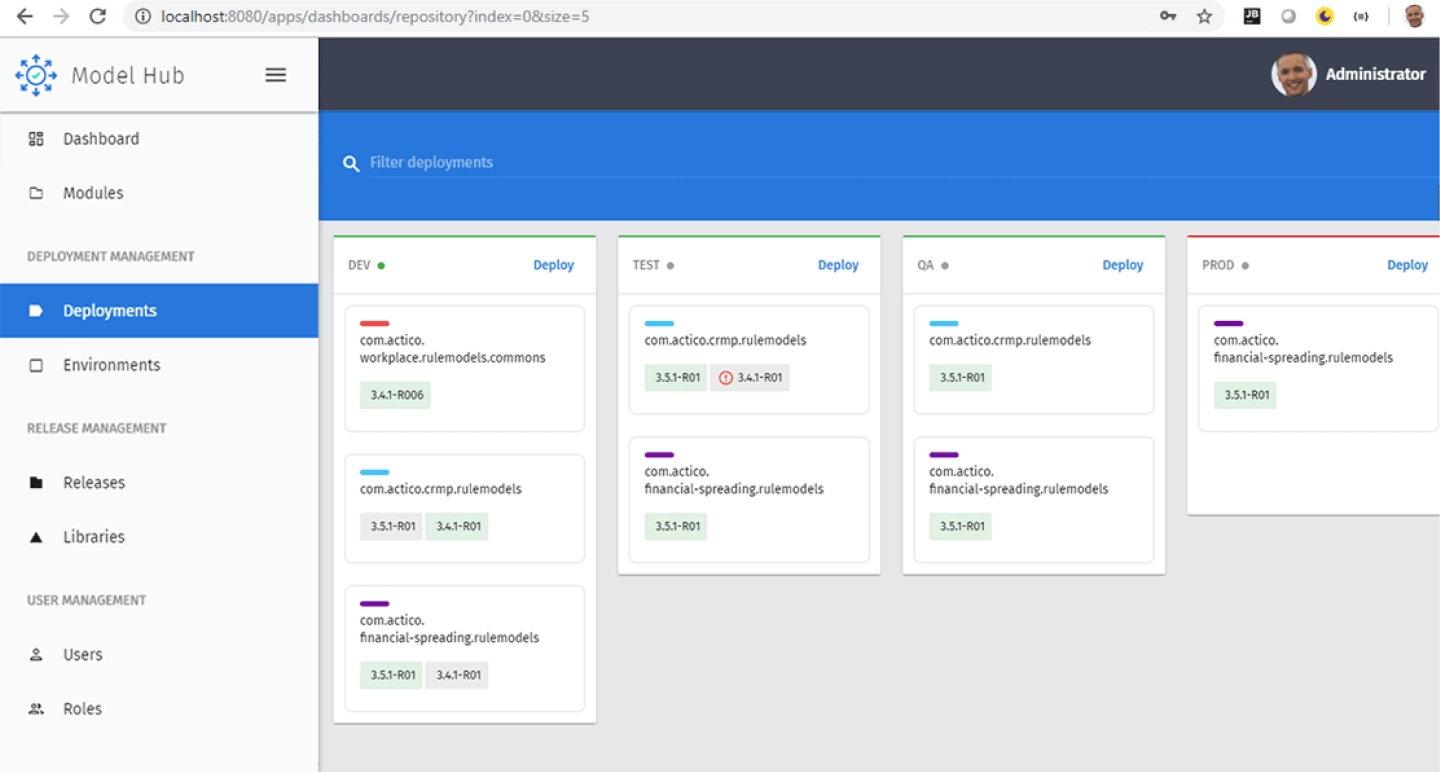

2. ACTICO

ACTICO positions itself as a stronger pure-play decisioning product with a graphical drag-and-drop rules environment, real-time execution, model simulation, and Git-based versioning.

Best suited for: Banks and regulated lenders that want serious decision automation accompanied with auditability, model governance, and business-user control over decision logic.

Built on a graphical decision automation engine, the credit decision platform by ACTICO enables banks to design, test, simulate, and optimize their internal decision services such as risk scoring, pricing, and even complete credit decisioning strategies. The platform can be integrated into existing origination workflows and can execute bank-internal decision logic in real time.

One of ACTICO’s key strengths is the fully graphical drag-and-drop editor, which makes it easier for business and risk teams to create, implement, and adjust decision models without relying heavily on developers. Plus, all models are stored in a centralized Git-based repository, so version control and collaboration stay organized and transparent.

ACTICO also supports the management and integration of existing models built in Python, Java, R, SAS, or H2O, which gives lenders the freedom to keep using the tools they already rely on.

The platform can simulate and refine risk models and decision strategies, helping teams understand potential outcomes before promoting changes into production.

Key features:

- Visual drag-and-drop editor for building and adjusting decision logic without relying heavily on developers

- Real-time execution of credit rules and strategies

- Centralized Git-based repository with full version tracking

- Simulation tools for testing and optimizing risk models

Pros:

- Solid choice for explainable, governed decisioning in a banking environment.

- Strong for institutions that already have model assets and want to operationalize them without rebuilding everything.

- Great tool for workload reduction with strong automation benefits, according to public reviews

Cons:

- Centered on origination and decisioning rather than full servicing.

- According to reviews, UI may feel confusing to some users.

3. CloudBankin

CloudBankin positions itself as an end-to-end loan software, low-code configuration, digital onboarding, a loan origination system, loan management, and a credit rule engine.

Best suited for: Banks, NBFCs, MFIs, and fintechs that want fast digital transformation with one cloud platform.

With over 2,000 configurable data points, CloudBankin’s digital lending platform includes a credit decision engine that lets lenders tailor their underwriting logic precisely to their own risk guidelines. Decisions can either be fully automated through straight-through processing or routed to underwriters for manual review when needed.

The system also includes a scoring module that creates custom scorecards based on your criteria. For instance, assigning a score of 10 if a borrower’s credit score is above 600, and 12 if it’s above 650. Beyond that, the rule engine can interpret 100+ parameters such as age, income, and credit history to generate decision outcomes and recommend terms, including interest rate tiers.

One of the platform’s most outstanding features is the calculation script module, which allows you to define non-standard financial ratios like debt-to-income without the need to go into traditional software development coding.

CloudBankin is highly configurable, which means that lenders can add, tweak, or remove data points and rules to keep their credit decisioning process agile and precise.

Key features:

- Automated straight-through processing + optional underwriter review

- Credit rule engine for simple to complex credit policies

- Built-in scorecard creation using custom scoring rules

- Scripted calculation support (e.g., debt-to-income, financial ratios)

- Low-code setup and workflow management

Pros:

- Broad lifecycle coverage makes it a credible alternative for lenders who prefer a single cloud stack.

- User-friendly interface

- Support for over 2,000 configurable data points

Cons:

- Some users mention slowness with large data volumes.

- CloudBankin’s public materials put little emphasis on deep model governance and advanced decision simulation.

4. Lendflow

Lendflow is strongest when the goal is embedded lending and API-first credit infrastructure rather than a classic bank-grade origination core.

Best suited for: Fintechs, vertical SaaS firms, and platforms that want to embed lending quickly and orchestrate multiple lending workflows.

Lendflow’s credit engine enables lenders to deliver fast and smart credit decisions by giving them access to a broad set of financial, business, and fraud-related data through a single API. This includes accounting and payroll data, business credit scores, social scoring, personal credit information, and even bankruptcies, judgment liens, and UCC filings. If more information is needed, the platform can automatically pull additional real-time data from multiple sources through conditional triggers.

Apart from this, Lendflow provides lenders with the freedom to build their own proprietary credit scoring models directly inside the platform. These models can be customized in accordance with businesses’ specific risk appetites, which allows teams to fine-tune the way they interpret each applicant’s profile. For teams seeking a quicker setup, Lendflow offers pre-built scoring templates that assign weight to each data point and generate applicant rankings in seconds.

Each component of the Lendflow platform, such as credit decisioning or borrower onboarding, is fully embeddable, which means that you’re free to use individual features as needed or scale them as your platform grows.

Key features:

- Custom underwriting workflows with conditional data triggers

- Ability to build proprietary scoring models or use ready-made templates

- Fast applicant ranking powered by flexible scoring logic

- Fully embeddable components for credit decisioning and onboarding

- Connectivity to 75+ capital partners and 5+ product types

Pros:

- Solid option for speed, modularity, and embedded finance use cases

- Flexible entry points make it appealing for teams that want to start small and expand

Cons:

- It is less of a full lending operating system, centering on embedded connectivity and marketplace infrastructure.

5. Pega Credit Risk Decisioning

Pega is an enterprise choice for organizations that want credit risk decisioning tied to BPM, case management, and cross-functional orchestration.

Best suited for: Large enterprises and banks that want decisioning embedded in broader process automation and customer operations.

Pega’s credit risk decisioning feature delivers context-aware decisions, accelerates time to value, as well as integrates dynamic case management.

At the core of the solution lies the Pega Customer Decision Hub that acts as the platform’s central intelligence layer. Powered by AI and real-time insights, it evaluates each credit situation in context and recommends the next best action.

What’s more, all audit trails, version control, and governance can be handled right within the platform, which gives companies greater oversight and, consequently, allows them to gain extra confidence when performing credit risk operations. Besides, Pega comes with strong compliance and security capabilities. The platform also supports major privacy and data protection requirements, including GDPR, the California Consumer Privacy Act / California Privacy Rights Act, FDA regulations, and the Data Privacy Framework through built-in security controls, governance tools, and policy automation.

Another prominent feature of Pega is that it promotes consistency across every interaction. It keeps the customer at the center by delivering a unified contextual experience across all channels for both customers and employees.

And because Pega connects credit risk functions with marketing, sales, and service teams, organizations are able to collaborate more effectively and keep credit decisions in sync with overall business goals.

Key features:

- Real-time credit risk decisioning powered by a centralized AI-powered hub

- Unified data, workflows, and decision logic across business functions

- Unified decision logic across all customer and employee channels

- Dynamic case management and omni-channel orchestration

- Built-in audit trails, governance, and version management

- Low-code tools for business-user policy and decision logic management

Pros:

- Strong enterprise-grade option for complex workflows and decisioning at scale.

- G2 and Capterra reviews frequently feature its customization power, drag-and-drop design, and ability to build complex business solutions.

Cons:

- Learning curve and implementation complexity might pose a challenge

- Pega might appear a heavy enterprise transformation choice for lenders that mainly want lending-native functionality.

6. RiskSeal

RiskSeal focuses on alternative-data scoring via digital footprint analysis.

Best suited for: Lenders that want to augment traditional underwriting with alternative data, especially in thin-file or emerging-market contexts.

With RiskSeal, businesses are able to tap into more than 400 alternative data signals per applicant. The credit decision platform analyzes a borrower’s email, phone number, IP address, full name, location, and photos, and evaluates their digital footprint across more than 200 online platforms. All of this comes together in a single API call, delivering a detailed client profile, a ready-to-use digital credit score, and actionable insights in one place.

The credit decision platform makes use of digital footprint data and AI-driven analytics to deliver precise identity verification and solvency assessments. Plus, it also explains each applicant’s score so that lenders can better understand how credit decisions are made. Importantly, all processed data is then returned to the lender to guarantee full control and transparency over the inputs used in credit decisions.

Apart from standard credit risk scoring, RiskSeal allows teams to build custom features for their scoring models so as to boost predictive power and decision accuracy.

Chiefly, the RiskSeal platform is designed with strict adherence to privacy regulations and ensures full compliance with GDPR and the California Consumer Privacy Act.

Key features:

- AI-powered identity verification and solvency checks

- Customizable scoring features for maximum predictive power

- Alternative-data enrichment for thin-file underwriting and fraud-related signals.

- 400+ data points and digital-footprint analysis across 200+ platforms

- Identity verification through multiple names, photos, and email/phone number links

Pros:

- Solid solution for alternative-data enrichment and fraud-aware scoring.

- Very light integration model through API delivery.

Cons:

- Not a full decisioning or lending stack on its own, but rather a scoring enrichment layer.

7. Experian

Experian remains one of the safest names in the category when a lender wants decisioning tied directly to rich data assets, analytics, and risk controls.

Best suited for: Banks, card issuers, and established lenders that want data-led decisioning with strong analytics and risk visibility.

Experian’s credit decisioning engine enables lenders to combine machine learning with Experian’s proprietary and partner data to produce an optimized credit decision. Its flexible orchestration and built-in advanced analytics let lenders run thorough risk assessments, apply targeted verifications, and tweak decision flows in real time.

The platform provides a 360-degree view of both consumer and business accounts, which allows lenders to identify tricky or high-risk debtors, spot trends and patterns, and uncover predictive insights that guide smarter decisions. By pulling together a wide range of data sources, including consumer and commercial credit information, contact data, and analytical services, lenders manage to establish the full picture of borrowers’ creditworthiness, make more informed credit decisions, and optimize their overall profitability.

As well as this, Experian supports proactive risk management and enables lenders to catch inconsistencies early, prevent potential fraud, and step in confidently before small problems turn into bigger ones.

Key features:

- Full view of consumer and business accounts

- Built-in analytics enriched by proprietary and partner data sources

- Proactive risk controls that surface inconsistencies earlier

- Decisioning workflows optimized for speed, accuracy, and consistency

- Support for pricing, customer acquisition, and portfolio risk management.

Pros:

- One of the strongest choices for data depth, analytics credibility, and enterprise trust.

Cons:

- For lenders that want a highly configurable, lending-native workflow platform, Experian can feel more data-and-decisioning centric than operationally end-to-end.

Credit Decisioning Software Comparison Table

| Software product | Key strength | Customization | AI capabilities | End-to-end coverage | Best use-case |

|---|---|---|---|---|---|

| HES LoanBox | End-to-end lending and credit decisioning | Very high (fully configurable workflows, scoring, UX) | Advanced (AI scoring + rule-based transparency) | Full (origination, decisioning, servicing) | Banks and fintechs that need rapid embedding, audit-friendly explainability, and higher approval accuracy with lower manual review overhead |

| ACTICO | Visual decision automation | High (rule-based decision automation) | Moderate/advanced (AI + rules) | Partial (decisioning + compliance focus) | Banks and risk teams that want non-technical model design and testing |

| CloudBankin | Highly configurable decision engine | Medium/high | Moderate (rule-based + some AI) | Full (lending lifecycle platform) | Lenders requiring very granular underwriting logic |

| Lendflow | API-centric credit engine | Medium | Moderate (data-driven decisioning) | Limited/partial (decisioning + integrations layer) | Lenders requiring very granular underwriting logic |

| Pega Credit Risk Decisioning | Unified AI-powered credit risk hub | High (case management + workflows) | Advanced (AI + decisioning + BPM) | Partial–Full (strong workflow, not lending-specific end-to-end) | Large enterprises needing context-aware, regulated decisioning |

| RiskSeal | Alternative data & digital footprint scoring | Medium/high | Advanced (AI/ML risk scoring) | Limited (decisioning layer only) | Teams focusing on alternative data for enhanced risk insights |

| Experian’s Decisioning Engine | ML-enhanced credit decisions with rich data | Medium | Advanced (strong data + analytics) | Partial (decisioning + data, not full LOS) | Lenders wanting deep data integration and advanced analytics |

Main Benefits of Credit Decisioning Software

The best credit decisioning software brings several big advantages for businesses. Let’s take a look at the most significant ones.

| Benefit | How it works |

|---|---|

| Faster credit decisions | Automated workflows allow lenders to reduce decision times from hours to minutes and approve credit applications faster |

| Reduced manual workload and fewer errors | Streamlined processing minimizes manual effort and reduces common mistakes related to data entry, document verification, and policy compliance |

| Better-quality credit assessments | Models leverage data from multiple sources, including credit bureaus, open banking, and alternative data (e.g., utility bills, rental payments, and social scoring), which enables teams to build more accurate borrower profiles and improve risk assessment |

| Stronger compliance and auditability | Detailed logs ensure decisions remain transparent, fair, and easy to review |

| Higher customer satisfaction | Faster responses create smoother borrower experiences, which translates into stronger loyalty |

| Stronger portfolio security | Built-in fraud checks identify risks before they impact lending operations |

1. Faster credit decisions

Given that the loan decision software automates the data collection, validation, and initial analysis processes without requiring substantial involvement of the staff members, lenders can move through applications much faster and, therefore, generate lending decisions much quicker.

2. Reduced manual workload and lower risk of errors

With the best credit decisioning software, manual data entry is reduced to the barest minimum.

A large portion of the repetitive work such as sorting documents, checking for missing details, calculating ratios, and pulling bureau data gets handled by the platform, which frees up underwriters to zero in on the more nuanced and higher-risk cases.

Plus, this also cuts down on human errors and overlooked details.

3. Better-quality credit assessments

With access to richer datasets, open banking transactions, and historical trends, lenders can establish a more comprehensive picture of a borrower’s financial behavior alongside their overall creditworthiness profile.

4. Stronger compliance and auditability

In the best credit decisioning software, every step of the decisioning process is logged and can be easily traced, which is crucial for regulatory checks.

Modern credit decision software assists lenders with demonstrating fairness, transparency, and non-discrimination under regulations such as the European Union Artificial Intelligence Act (EU AI Act) or the U.S. Equal Credit Opportunity Act (ECOA), Regulation B, by providing a transparent record of what influenced each credit decision.

Another important aspect is the explainability of AI/ML models, which lets lenders show both regulators and applicants how automated scoring works, providing clear reasoning for approvals or declines.

5. Higher customer satisfaction

As far as borrowers are concerned, they benefit from quicker responses, fewer back-and-forth requests, and a generally more satisfying user experience.

For businesses, higher customer satisfaction translates into stronger loyalty, improved conversion rates, and a more competitive offering.

6. Stronger portfolio security

Some advanced credit decisioning solutions come with robust fraud detection capabilities that can flag mismatched details, unusual transaction patterns, or documents that don’t match the known data sources.

Thanks to this, lenders can step in early, prevent fraudulent cases from advancing through the pipeline, protect portfolios, and preserve the overall decision quality.

Conclusion

The best credit decisioning software delivers a range of meaningful benefits, including faster decisions, stronger compliance, deeper risk insights, and better protection against fraud. Altogether, these advantages allow lending teams to operate much more efficiently and provide borrowers with a more satisfying experience.