Credit risk management has become more complex as market conditions shift faster and less predictably than before. Borrower behavior is no longer stable: cash flows fluctuate, repayment patterns change, and segments that were historically reliable can deteriorate within months. As a result, decisioning frameworks built on historical assumptions are losing accuracy.

At HES FinTech, we have always centered our work on solutions that help lenders perform better. Based on that experience, we want to share a practical view of what matters most in periods of volatility and how the right software can help lenders stay profitable even in uncertain market conditions.

This guide outlines how lenders can adapt to this environment. It brings together three perspectives from our team, each looking at the market from their experience. What unites their perspectives is a shared conclusion: today’s market requires solutions that can be implemented rapidly, but without compromise on quality. That is where the right technology becomes a competitive advantage rather than just an operational tool.

Read on to learn more about the possible approaches you can implement and practical examples from GiniMachine, our product based on AI tech stack.

Key Takeaways

- Static models are no longer enough. In volatile markets, lenders need adaptive decisioning tools that respond in real time to shifting borrower behavior and macroeconomic signals, not just historical data.

- Resilience is built on three pillars: real-time visibility into portfolio health, the flexibility to adjust risk parameters instantly, and the speed to execute decisions before data becomes outdated.

- Automated platforms significantly shorten the decisioning cycle, allowing lenders to retrain models and update strategies in days rather than months.

- For consistent, data-driven decisions, capabilities should be integrated across the entire lending lifecycle.

Why Credit Risk Is Becoming Harder to Manage

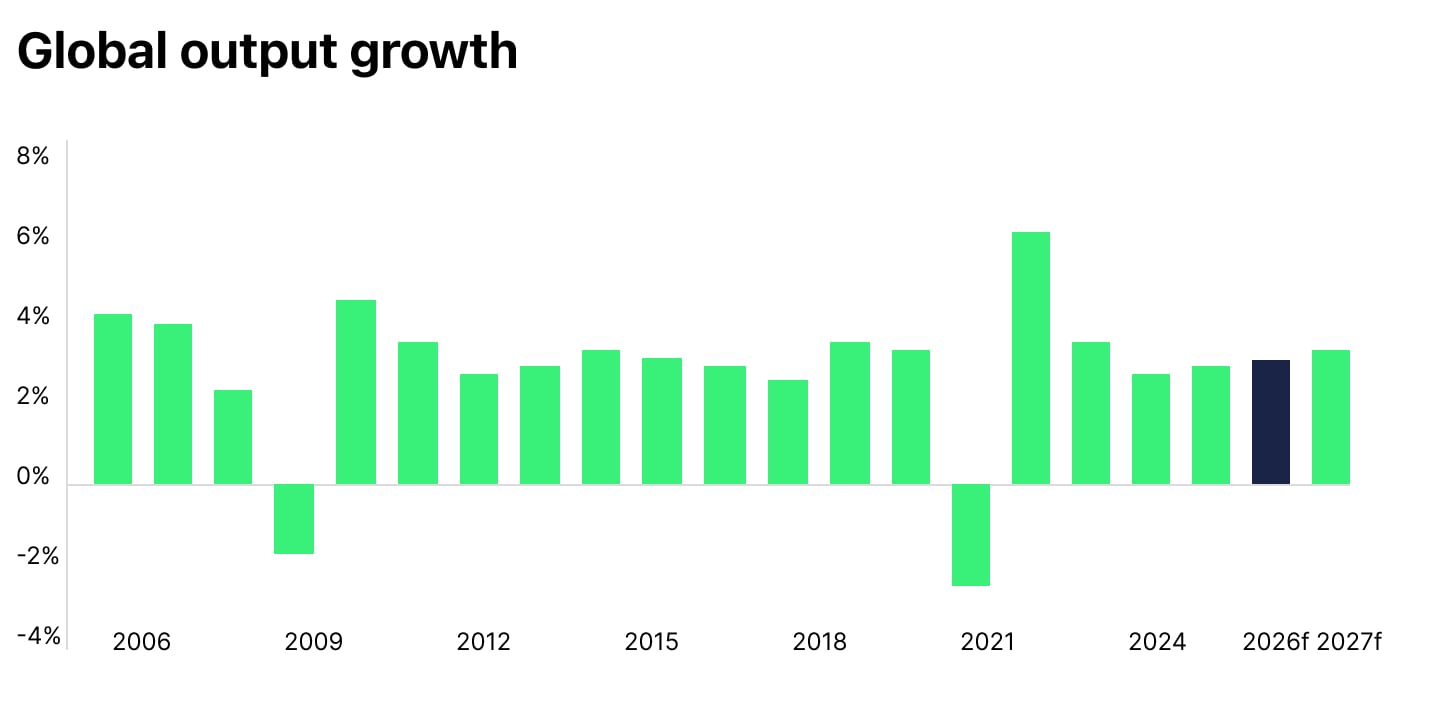

Markets are shifting faster than traditional credit rules can keep up. The current macroeconomic environment is defined by uncertainty rather than recovery.

According to the latest IMF World Economic Outlook, global growth is expected to hold at around 3.3% in 2026, while the World Bank warns that it could slow to around 2.6%, reflecting weakening momentum in certain regions of the global economy.

The current economic instability seems to be not a single-factor disruption but a combination of interconnected shocks that directly affect lending performance and borrower behavior. Logistical disruptions continue to break supply chains, which has a cascading effect on businesses’ cash flows. As a result, credit and factoring lines are no longer sufficient when existing limits simply do not cover operational gaps.

At the same time, time lags in revenue realization are becoming more pronounced: companies fail to receive expected income on time, which immediately affects their ability to service debt.

When instability hits, for both businesses and lenders, the priority is no longer growth alone but maintaining control by understanding where risks are building and which segments require immediate attention.

Artiom BrytunHead of Business Development

Artiom BrytunHead of Business Development

For borrowers, reduced cash flow leads to declining debt-to-income ratios and missed payments. For lenders, this uncertainty translates directly into operational pressure and delinquency risks. More applications no longer fit standard approval logic, and previously stable customer segments begin showing signs of financial stress.

In this environment, reducing risk is not enough. Lenders also need decision accuracy that holds up as market conditions change.

What Lenders Need for Credit Risk Management

The current economic downturn fundamentally changes the conversation with clients. The focus shifts from growth at any cost to something more practical: how to stay in control, protect portfolio quality, and make sound decisions in an environment that changes faster than many internal processes can adapt.

Every decision is now weighed against efficiency and return on investment. The question on everyone’s mind is, "Can we grow sustainably while managing risk?”

Ivan KovalenkoHES FinTech CEO

Ivan KovalenkoHES FinTech CEO

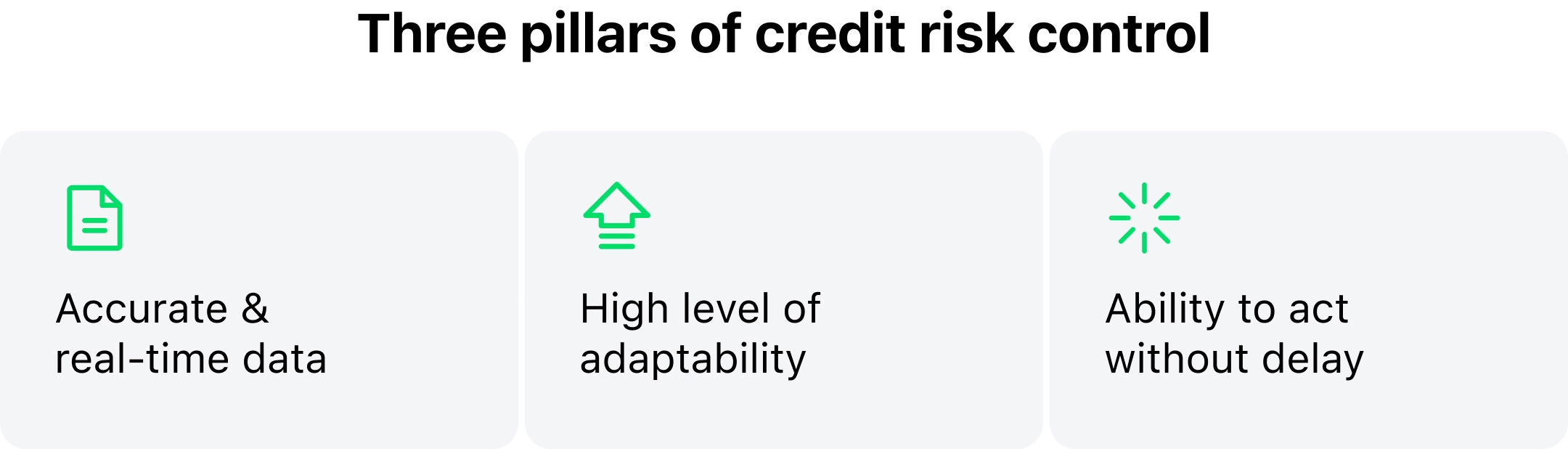

In this context, effective credit risk management is no longer defined by a single tool or model. The right approach for lenders combines three core capabilities: visibility, adaptability, and execution speed.

1. Visibility: Understanding Portfolio Risk in Real Time

A resilient risk strategy begins with a clear and continuously updated view of portfolio health. Effective decision-making must rely on accurate data rather than assumptions.

This requires continuous tracking of key metrics, such as delinquency rates, approval dynamics, and borrower behavior.

While traditional models such as logistic regression may be less responsive to sudden shifts in borrower behavior, modern scoring approaches rely on ensemble models. These can detect complex and sensitive dependencies, especially when enriched with macroeconomic variables such as inflation rates, currency fluctuations, and other external indicators. In the end, you have more accurate assessments of borrower solvency.

2. Adaptability: Adjusting Strategy as Conditions Change

In volatile environments, static decisioning frameworks quickly lose relevance. As market conditions evolve, lenders must be able to revise credit limits, adjust interest rates, and recalibrate approval criteria and acceptable debt-to-income thresholds.

These changes need to be directly reflected in portfolio strategy, including the ability to anticipate movement into higher-risk ‘gray’ or ‘red’ zones.

3. Execution Speed: Turning Insight Into Action

The value of an early risk signal drops sharply if the response comes too late. Speed implies operational readiness and smooth workflows.

Traditional model retraining and pipeline adjustments can take months, while the business cannot afford to wait. Modern platforms automate recalculations and simplify retraining, so teams can work with up-to-date data without long delays.

Mark RudakAI Product Owner, GiniMachine

Mark RudakAI Product Owner, GiniMachine

In short, lending teams benefit from systems that shorten the entire decision cycle and clear ownership of who updates thresholds, validates changes, and approves exceptions. AI-powered platforms help achieve this goal with automation: it ensures that decisions move quickly from analysis to execution, and changes are consistently applied across the portfolio.

In the next section, we'll elaborate on how these pillars work in practice with decision-making tools in each stage of the lending flow.

How Decisioning Supports Every Stage of the Lending Flow

Across the market, lenders are moving away from isolated tools toward integrated decisioning environments. They are looking for reliability and clarity across the entire credit lifecycle without adding complexity to their operations. So, the value of decisioning tools is measured by how consistently they support each stage of the lending process.

Let’s see how to manage credit risk by implementing a software solution that consistently supports you at each stage of the lending flow.

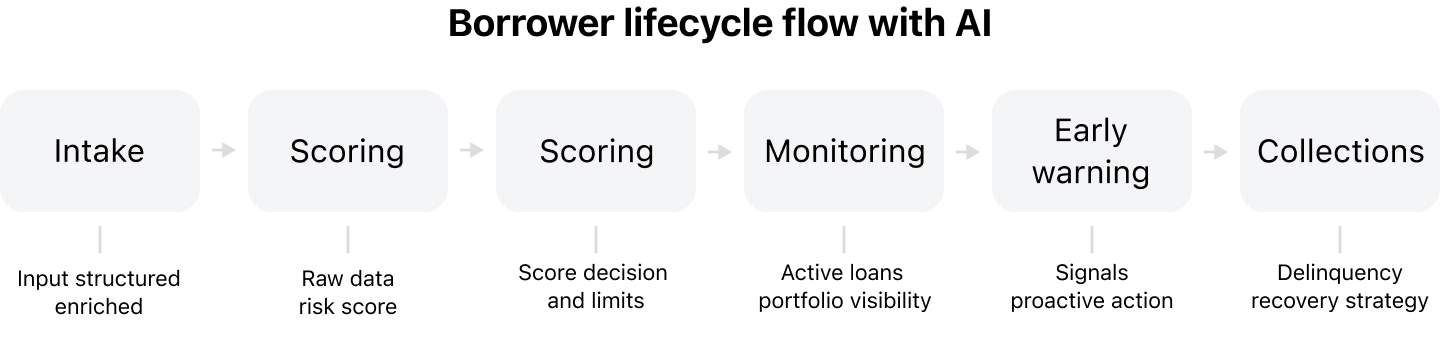

Application Intake

At the point of application intake stage, the quality of all downstream decisions is set, and inconsistent data leads directly to mispriced risk and unnecessary delays. Lenders therefore need structured, decision-ready inputs from the start.

In modern platforms, the intake layer standardizes data across all channels, validates it in real time, and enriches it with internal history and external data sources. So, before scoring begins, the borrower profile is more complete and up-to-date.

Also, to reduce operational load further down the flow, vendors often offer basic eligibility checks and initial risk signals. These remove clearly non-viable cases and fast-track stronger ones.

This approach was implemented at GiniMachine, where we combined data structuring, enrichment, and rule-based pre-decisioning in a single environment. As a result, every application entering scoring is already consistent, enriched, and aligned with current risk policies.

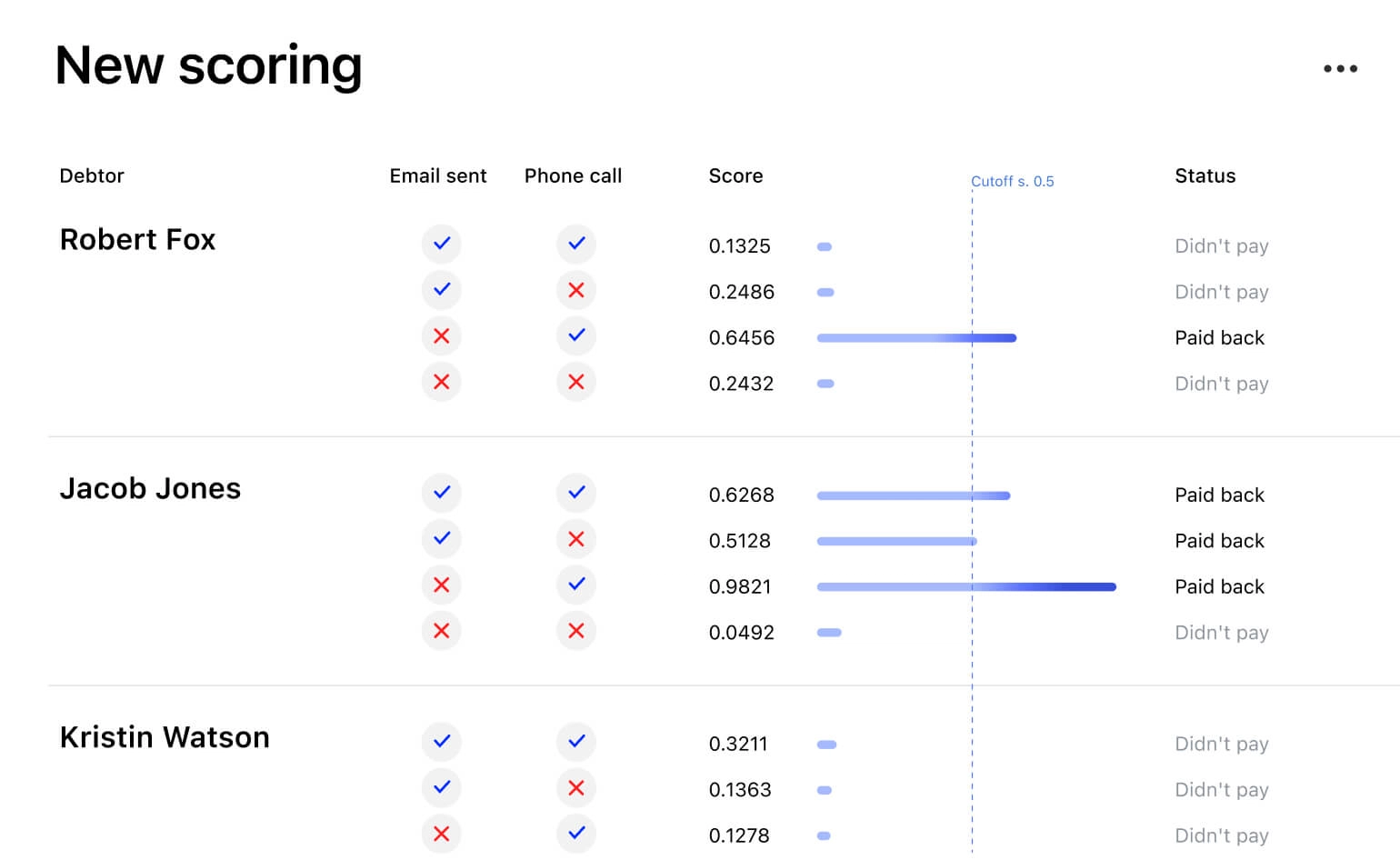

Scoring

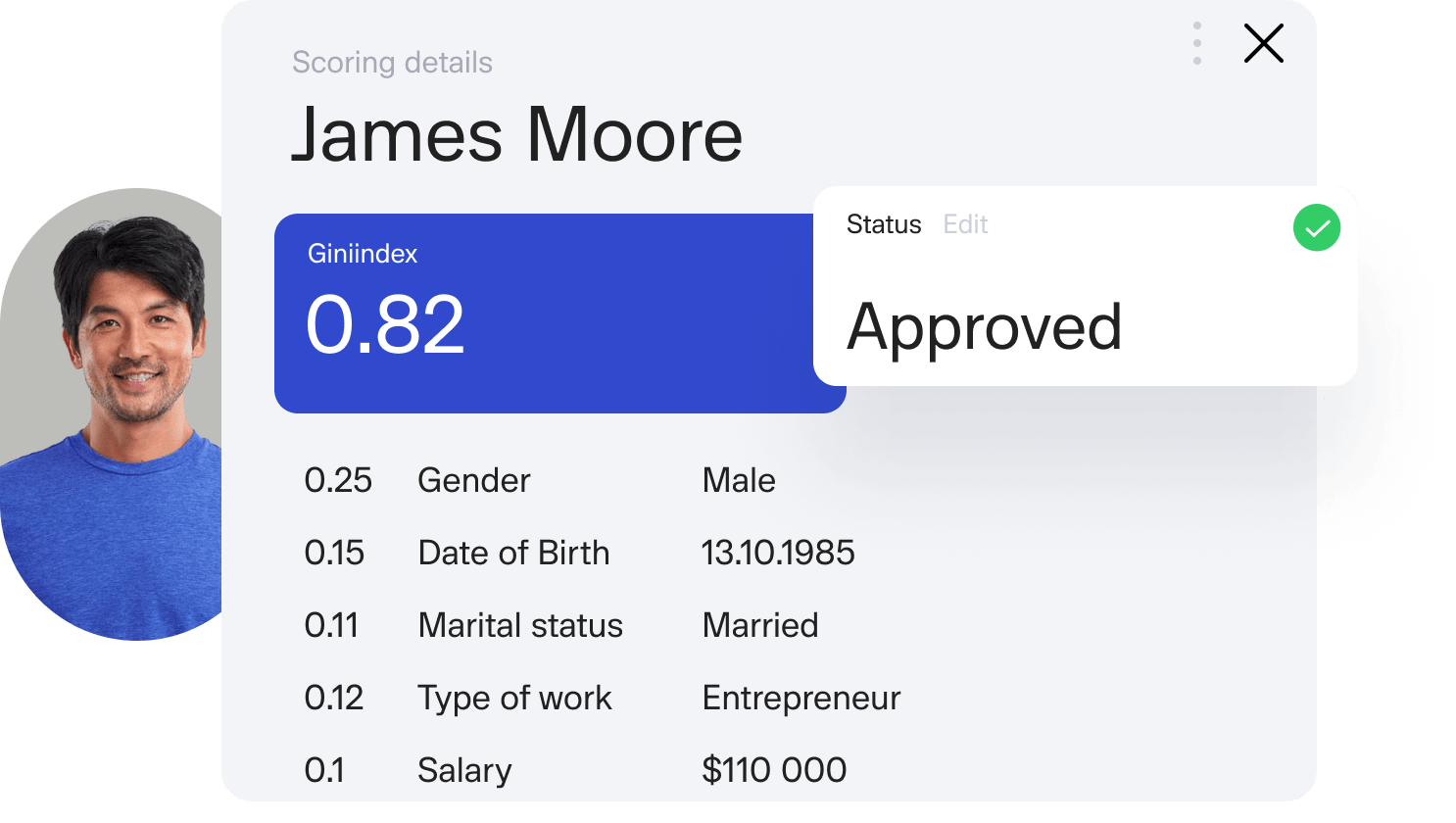

During application scoring, risk teams need a decision-support layer and must move beyond static scorecards with the help of adaptive models for scoring. Traditional scorecards built before a crisis often become unreliable, as they fail to reflect shifts in borrower behavior driven by macroeconomic factors such as inflation.

AI-powered platforms such as GiniMachine allow risk teams to retrain models on fresh data and deploy scoring models on this basis, without long development cycles or heavy involvement from data science teams.

Underwriting

During underwriting, the focus shifts from uniform limits and binary approval decisions to calibrated exposure. Lenders can align credit amounts with the borrower’s current risk profile, making the portfolio healthier in the future.

As mentioned above, lenders benefit from adaptability in cut-offs, limits, and decision rules in a controlled way. Ideally, this should happen without rebuilding the entire scoring pipeline and help immediately react to emerging risks. For instance, in our practice, we provided GiniMachine users the possibility to change exposure limits and approval criteria for a deteriorating segment in response to external shocks.

Monitoring

Once loans are issued, continuous monitoring becomes critical. Here, the software should track portfolio dynamics in real time, highlighting shifts in performance across segments, geographies, or products. Such visibility allows teams to detect deviations before they become systemic.

Real-time monitoring can be supported through configurable dashboards and reporting tools for key portfolio metrics, such as delinquency rates, approval dynamics, and borrower behavior. For SME portfolios in particular, where financial conditions can shift rapidly, these measures allow lenders to detect negative trends at an early stage and intervene before they translate into defaults.

Beyond high-level visibility, lenders can opt for segment-level tracking. It allows teams to analyze performance across borrower groups, industries, geographies, or product types and thus detect risk that would otherwise be hidden within aggregated portfolio data.

Most advanced software solutions, like GiniMachine, are able to analyze both behavioral signals (payment patterns, utilization changes) and external data inputs, as well as perform segment-level monitoring.

Collection

Finally, in collections, the same decisioning logic is applied. Borrowers are segmented based on the likelihood of recovery, enabling teams to focus resources where they are most effective while automating low-impact or low-probability cases.

When delinquency volumes increase and overload operational teams, collections efficiency depends on how precisely lenders can allocate their resources. By instant scoring and segmenting the entire portfolio, lenders can quickly identify and separate hopeless debt that can be sold to collection agencies, reducing operational costs associated with low-recovery cases.

A step forward in collections is segmenting the borrowers according to further communication strategies, such as automated SMS or email communication, as well as segments that require more focused and intensive recovery efforts. At GiniMachine, such a targeted approach helps improve both efficiency and recovery rates.

How to Adopt a Solution for Credit Risk Management in Practice

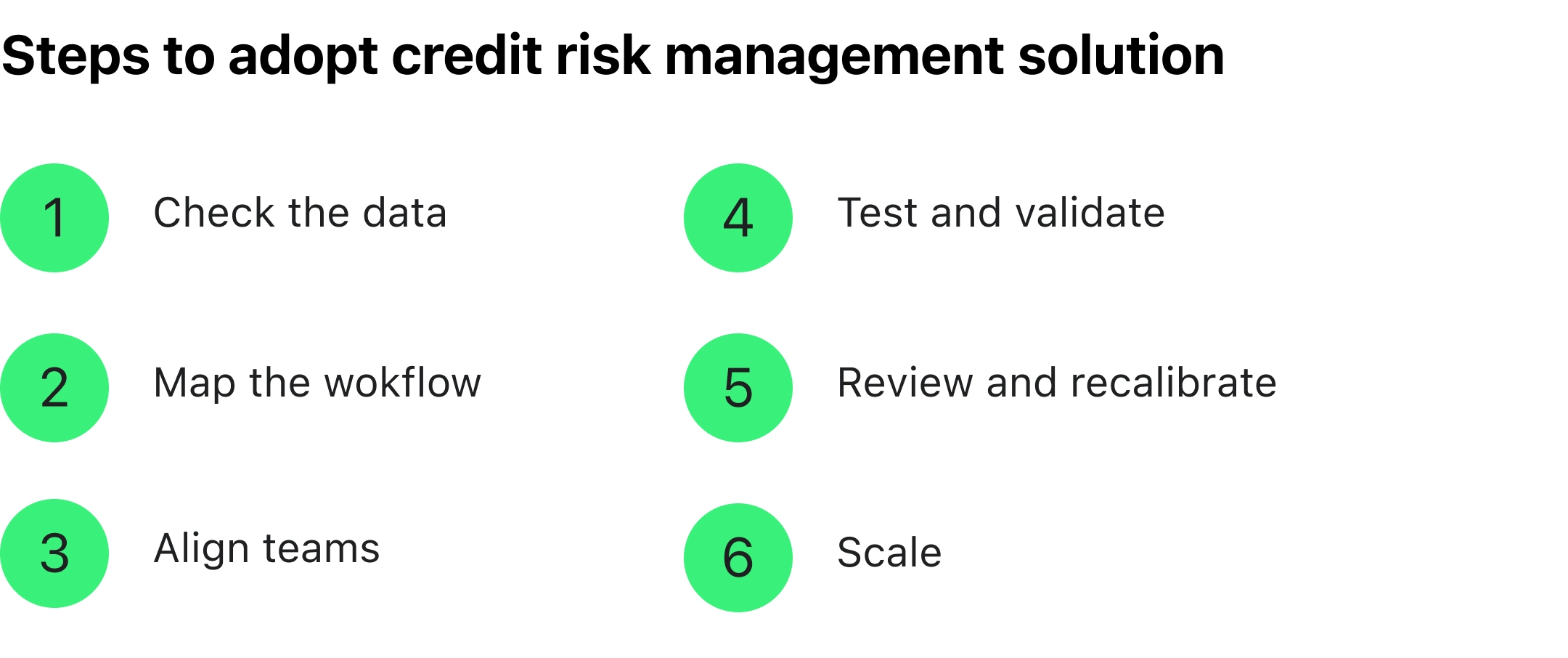

Implementing a credit risk solution works best as a phased operational project, not a full-scale system replacement. Lenders usually get better results when they start with one or two high-impact use cases. For example, you can implement early warning monitoring, portfolio segmentation, or underwriting policy updates — and then expand once the process is stable.

- Check the data

Before any model or dashboard is introduced, the lender needs to assess what internal and external data is available, how reliable it is, where gaps exist, and which variables actually matter for decisioning. Often, the biggest challenge is not model design but data consistency across systems. - Map the workflow

The solution should fit the existing lending workflow. That means defining how data enters the system, where scoring is applied, how exceptions are handled, who owns policy changes, and how decisions are logged and audited. - Align teams on rules and responsibilities

Implementation typically involves a small cross-functional team of risk analysts, data engineers, and portfolio managers, supported by platform specialists. All these actors need to agree on success criteria, approval logic, governance rules, and escalation paths. - Test before full launch and validate

A pilot phase with parallel testing is often the safest way to validate results before full rollout. During this period, lenders can compare old and new decisioning logic, measure impact on approval rates and delinquency, and refine thresholds before going live. - Review and recalibrate regularly

Implementation should be treated as a continuous cycle rather than a one-time launch. Volatile markets change borrower behavior, so the solution must be monitored, tested, and recalibrated regularly, resulting in retraining schedules, version control, and reporting routines that let the lender keep the system aligned with real portfolio behavior. - Scale across portfolios

Once the approach proves stable in one segment, it can be extended to other products, geographies, or borrower groups. At this stage, you can focus on consistency, which includes reusing proven logic, adapting it to segment-specific risks, and maintaining centralized control over policies.

When You Should Consider an Adaptive Decisioning Approach

Not every lender needs to overhaul their entire risk infrastructure immediately. There are certain signals indicating that an adaptive platform like GiniMachine can deliver significant value:

- Rapidly shifting portfolio risk

Delinquency patterns, vintage performance, or borrower behavior are changing faster than manual rules or static policies can track. - Outdated scorecards

Traditional models no longer capture current credit trends or macroeconomic realities, resulting in inaccurate risk assessments. - Operational strain in collections

Your teams are overloaded with exceptions, low-recovery cases, or manual segmentation tasks, slowing response times and reducing efficiency. - Delayed decisioning adjustments

Updates to credit limits, approval thresholds, or risk parameters take too long to implement, leaving portfolios exposed.

If you notice one or more of these conditions, you may benefit from a platform that provides real-time visibility, flexible decisioning, and rapid execution.

Conclusion

Volatility is the new normal, and resilience comes from operational confidence. Lenders who maintain visibility, adaptability, and speed in their decision-making can reduce exposure, respond proactively to shifting risk, and preserve portfolio health.

In uncertain markets, lenders do not need more complexity. They need better visibility, faster adaptation, and software that helps them act on real data. That is the direction we believe credit risk management is moving in—and the direction our solutions are built to support.