HES LoanBox is an AI-powered loan management system

that covers every aspect of loan origination, management, and servicing. Designed to meet Australian regulatory standards, HES LoanBox enables banks and alternative lenders to streamline their lending operations with increased speed, security, and automation. Our solution reduces NPL rate, drives increased revenue, and helps financial institutions serve their customers more effectively and efficiently.

Maximize performance with AI-driven system

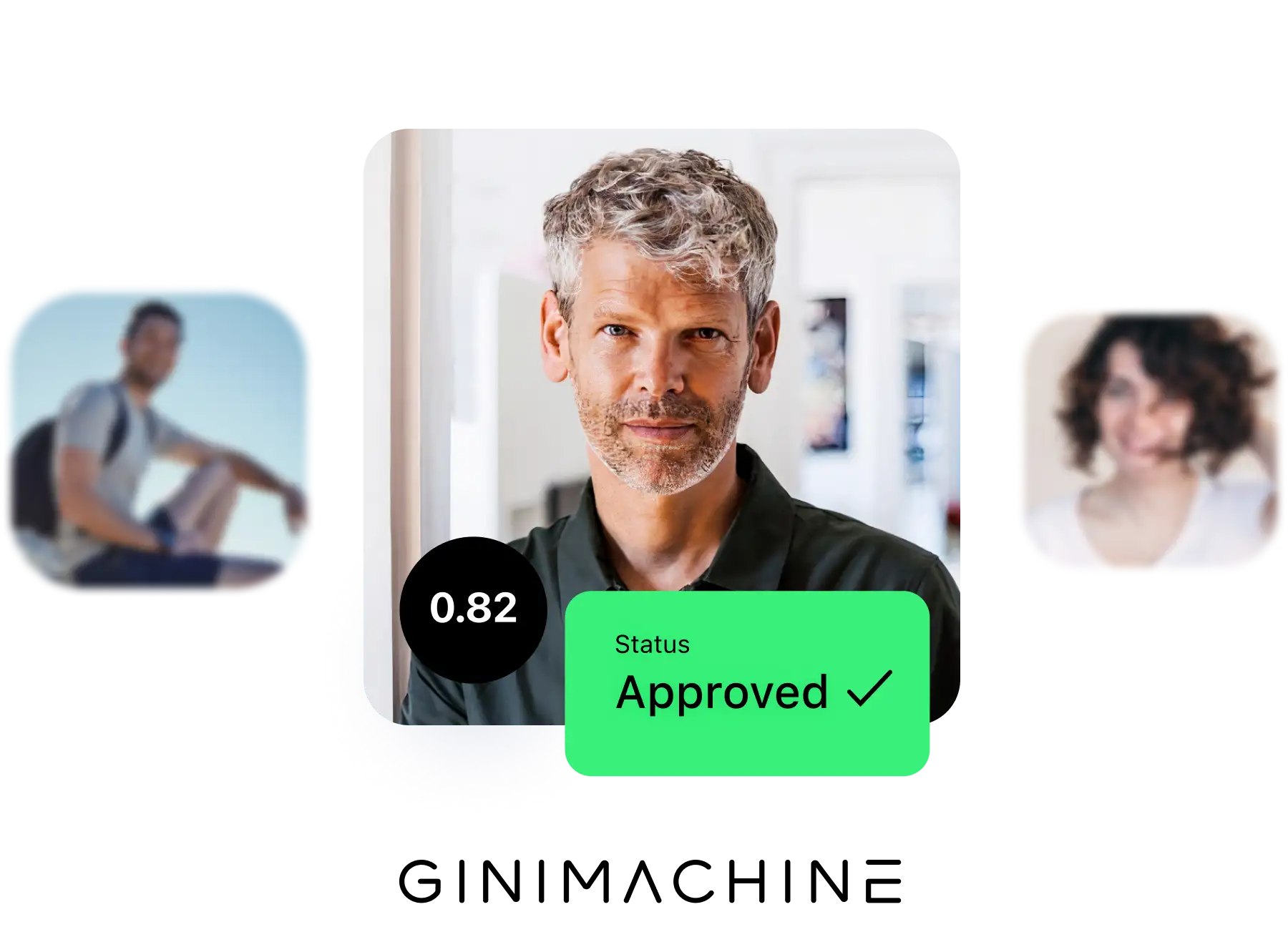

GiniMachine is a no-code AI tool

that extracts insights into borrowers' behavior using machine learning algorithms. Integrated within HES LoanBox, it eliminates guesswork from decision-making, enabling lenders to make informed, data-driven choices with confidence.

HES LoanBox overview

Lending management software

Our software is the go-to option for banks and alternative lenders aspiring to efficient, data-driven, digital loan management – from origination through servicing.

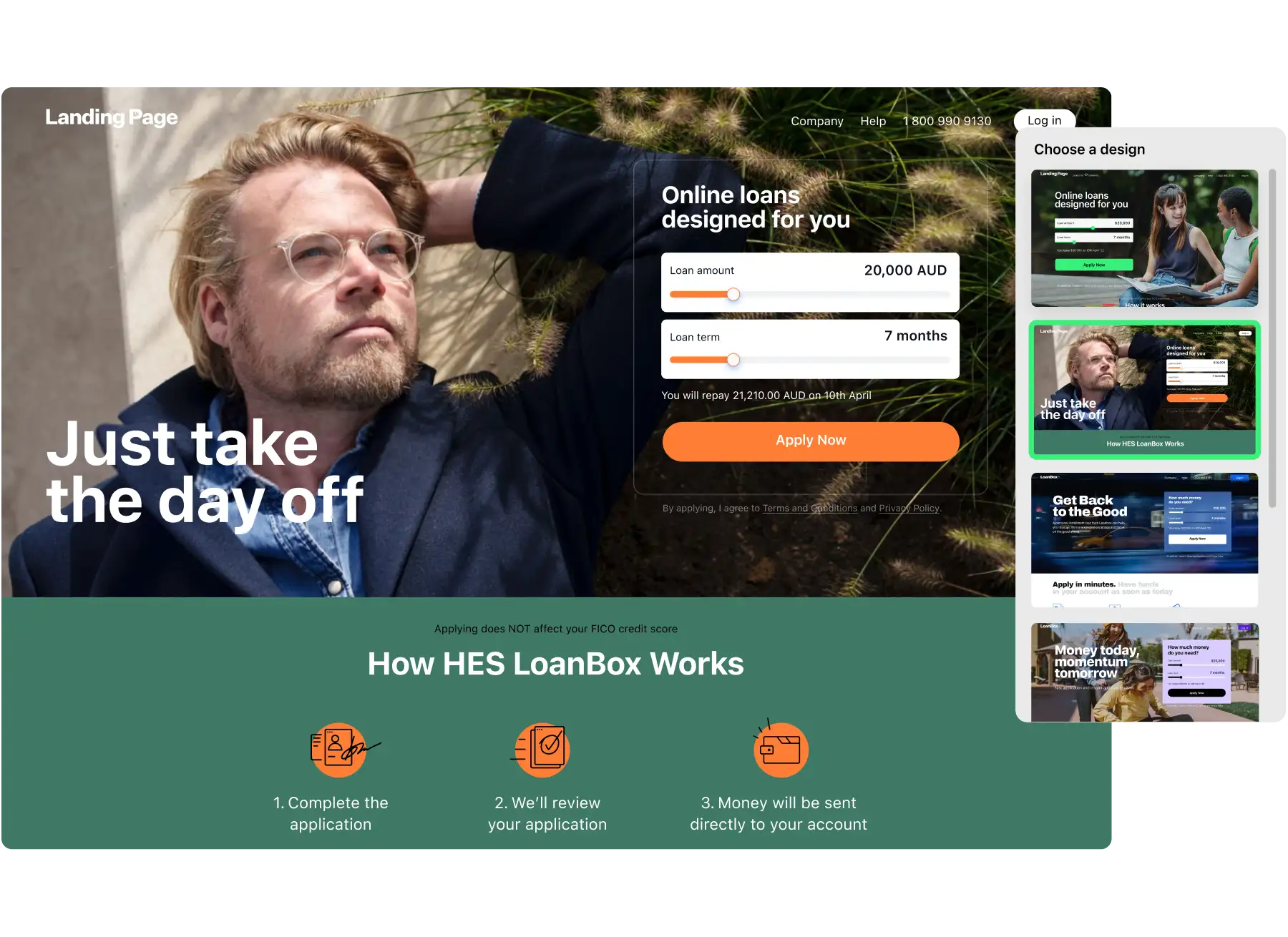

Customizable landing page

Create an intuitive loan website to increase engagement and drive more applications using

customizable white-label solutions.

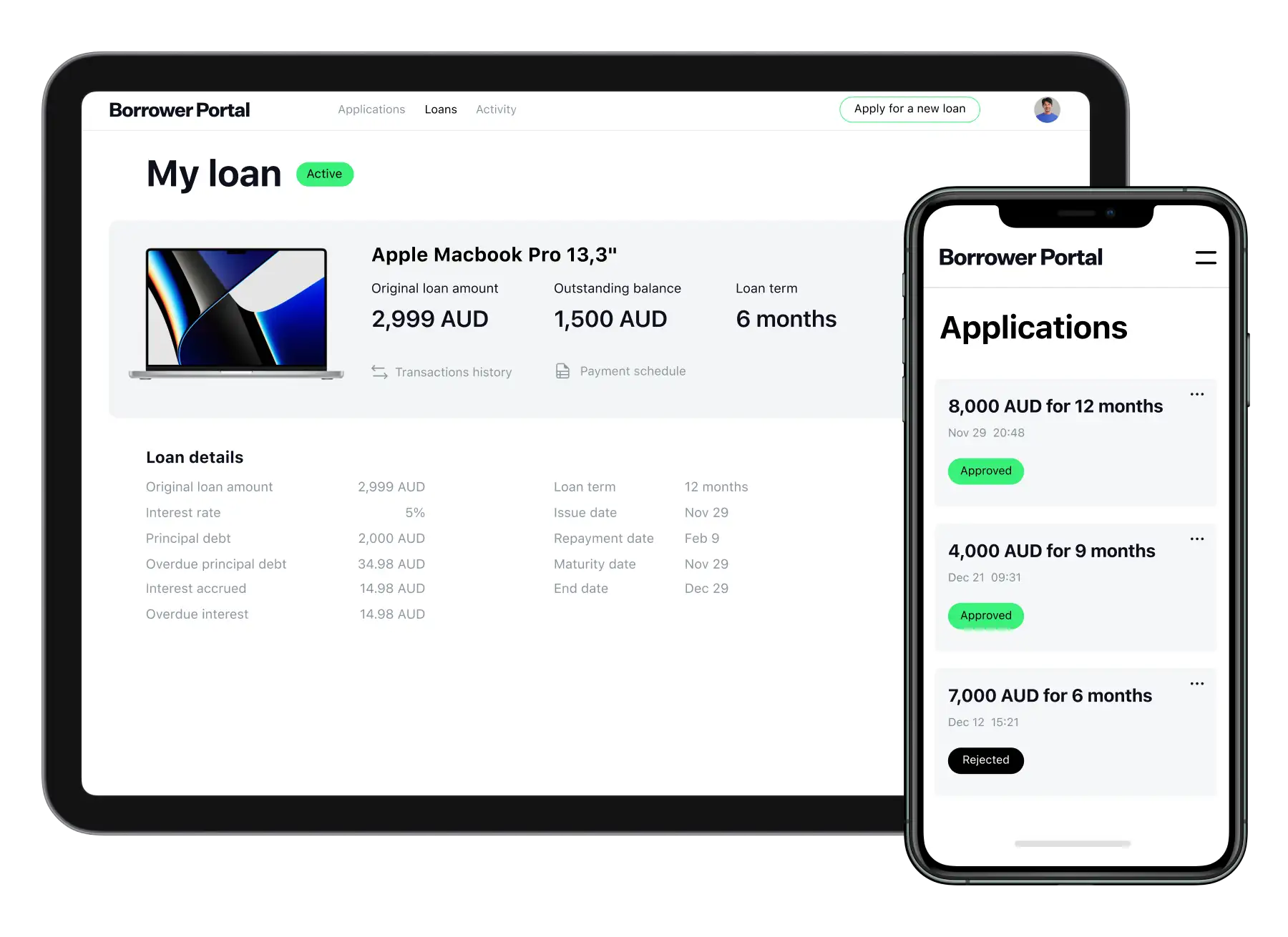

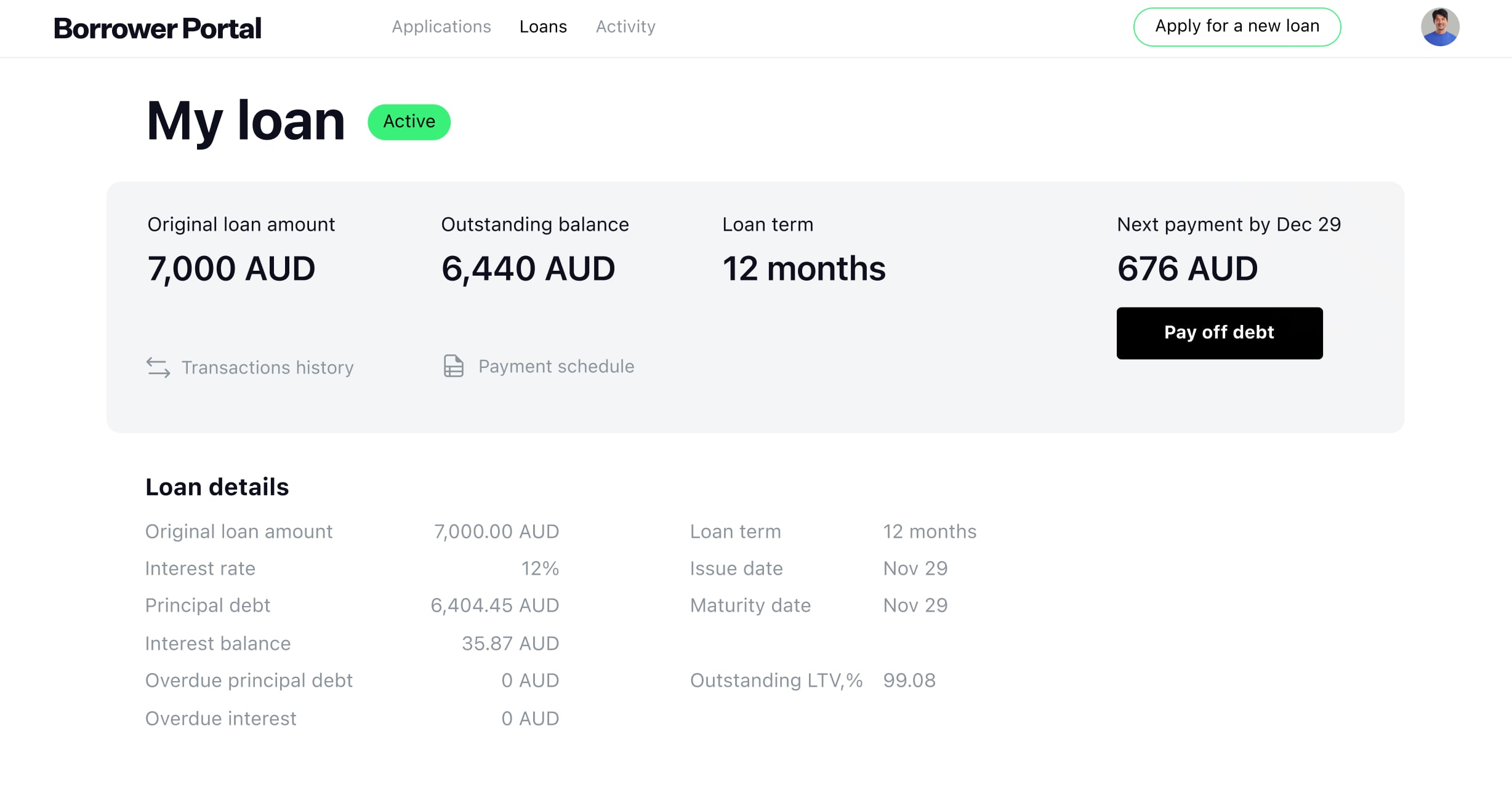

Make your customers' loan process easier

Provide a personal space where borrowers can manage every aspect of their loan journey – from

application to repayment.

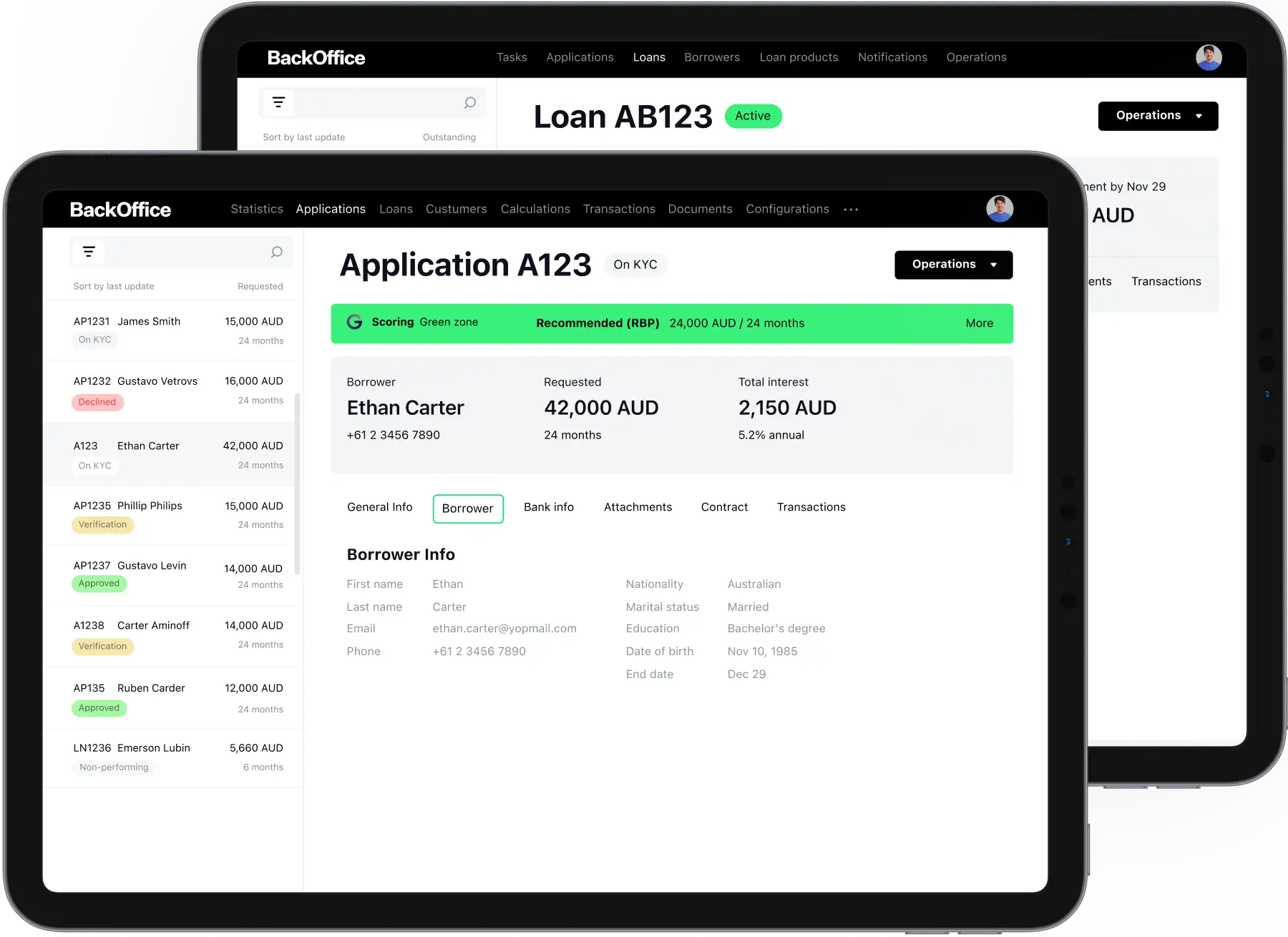

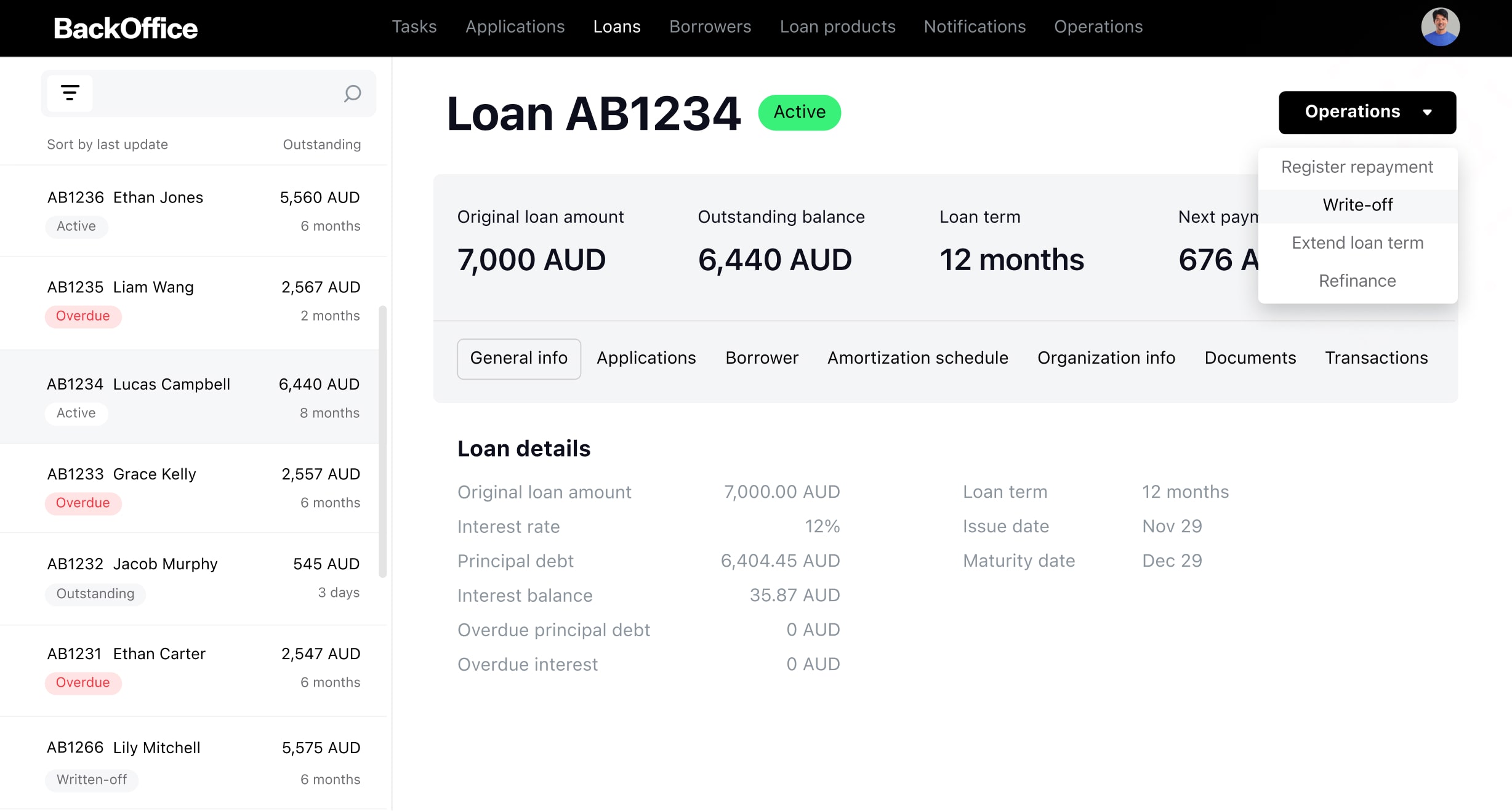

Centralize all lending operations

Streamline your operations with our API-rich Back Office, providing comprehensive loan products,

real-time data, amortization schedules, automated calculations, and everything else needed to

grow your business.

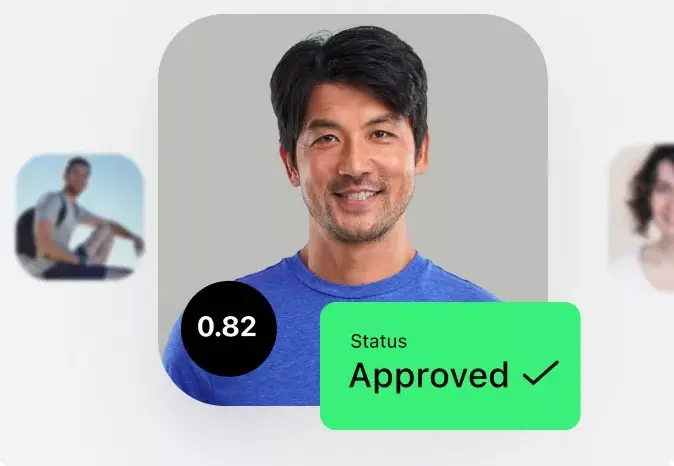

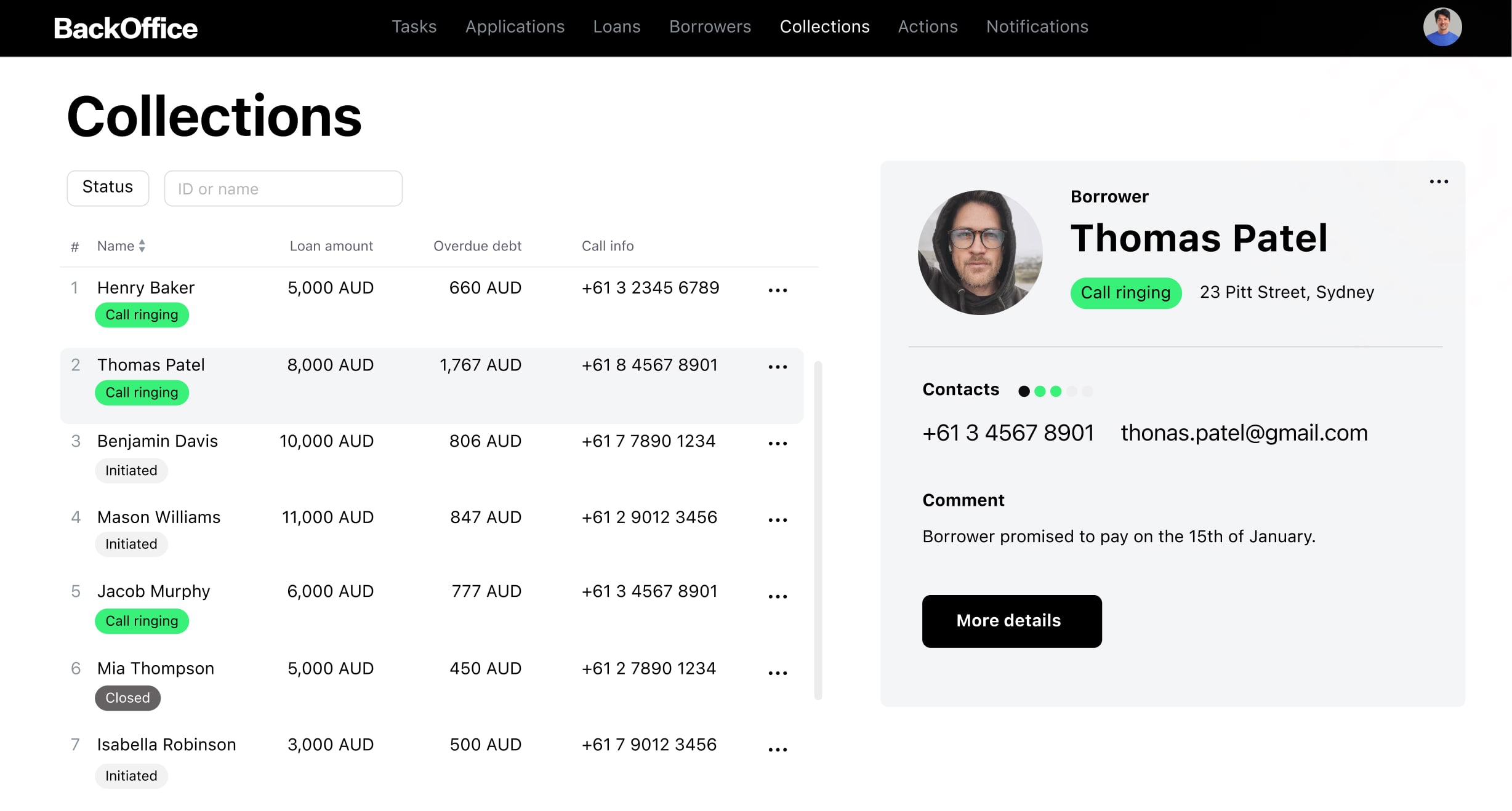

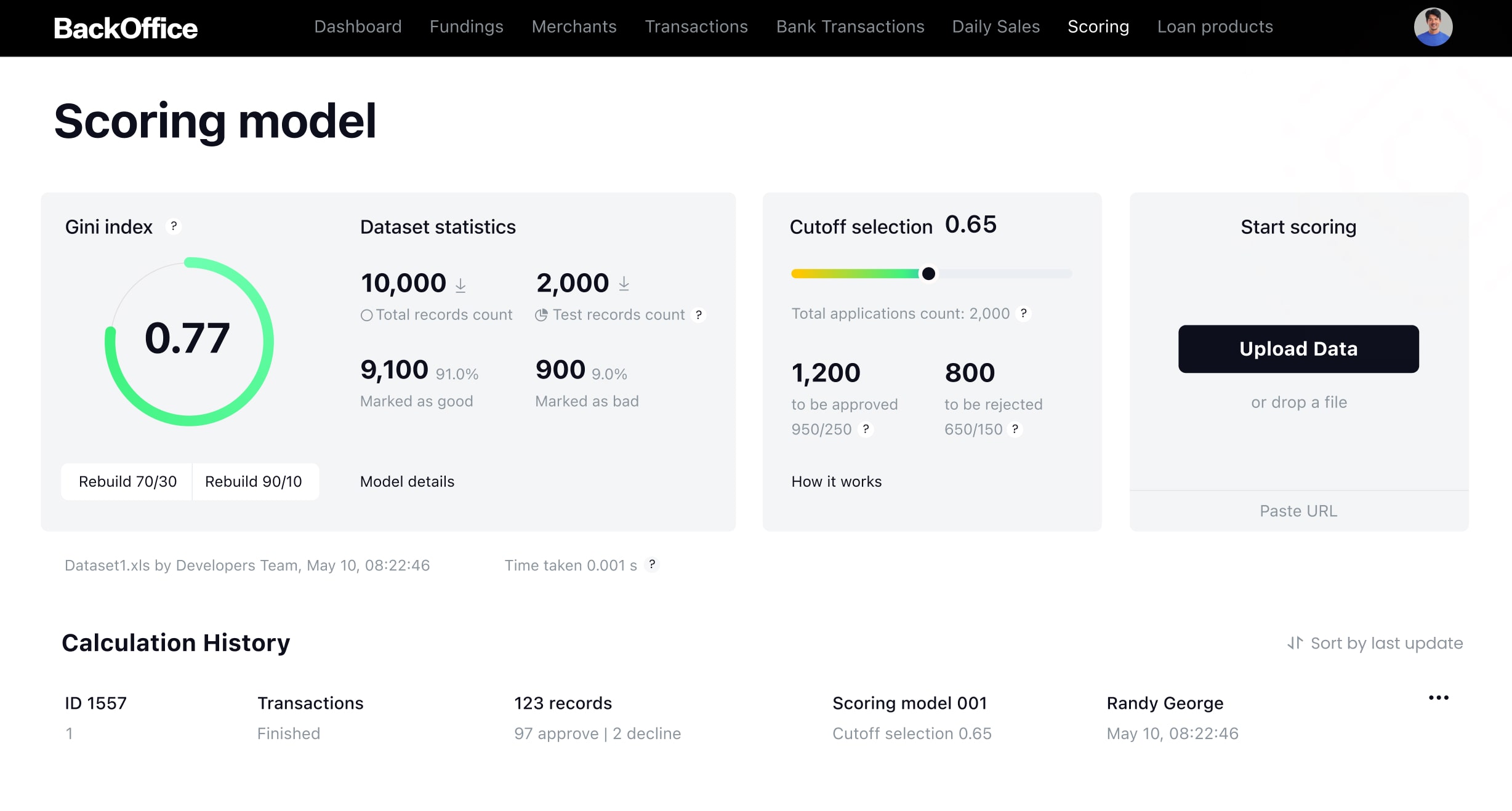

Reduce risk with AI-powered credit scoring

Leverage GiniMachine to analyze complex data patterns, improving accuracy in credit decisions,

minimizing NPLs, and facilitating more dependable credit assessments.

Developed with the newest tech stack

Ensure scalability, performance, and security with HES LoanBox, a cloud loan management system

developed using a modern tech stack that incorporates open-source technologies.

Security and compliance focused

HES FinTech holds ISO 27001 certification. It validates that our company adheres to

international best practices for information security, ensuring that client data remains secure

and confidential.

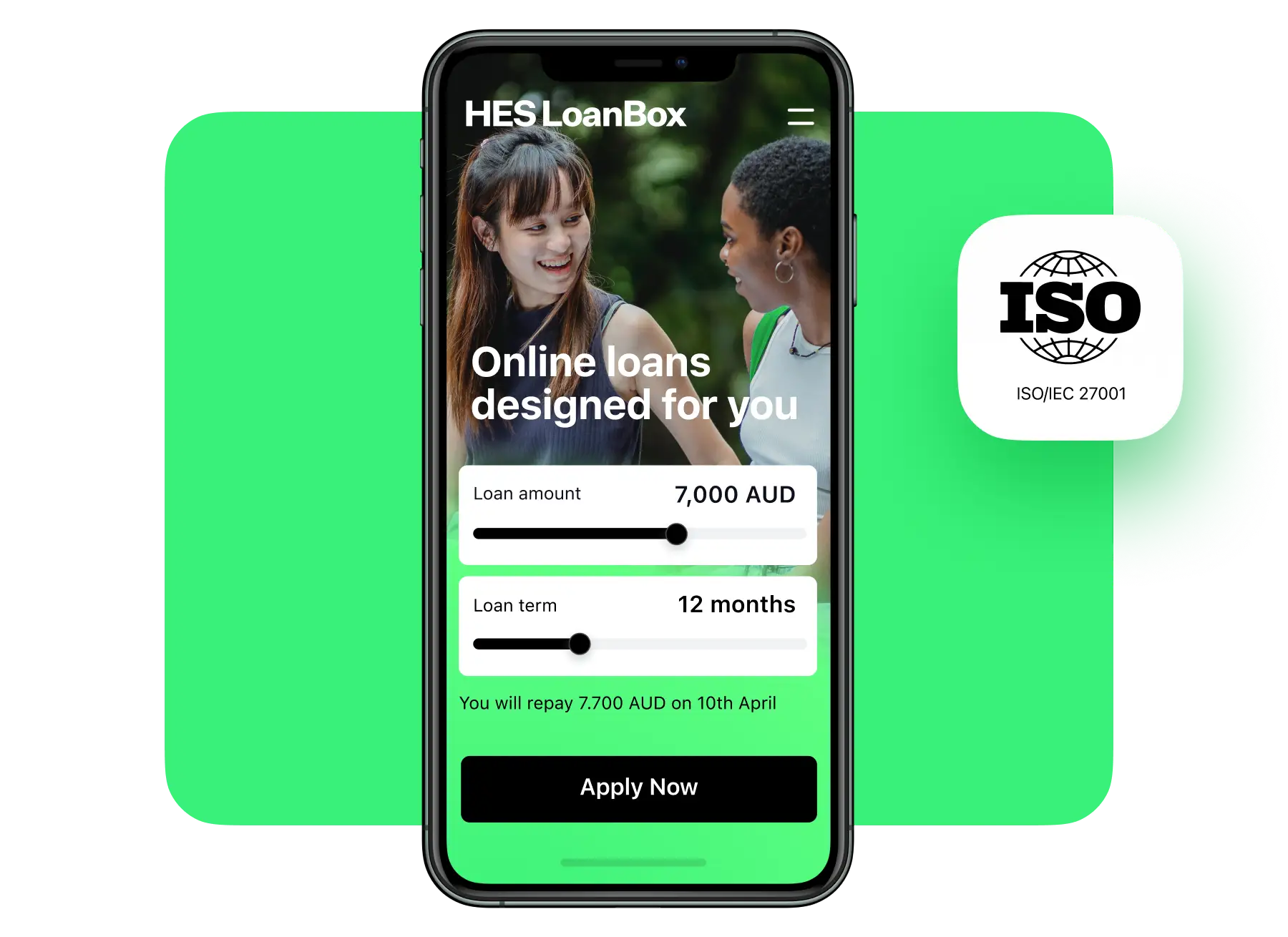

Digital onboarding

Transform leads into loyal borrowers

Landing Page

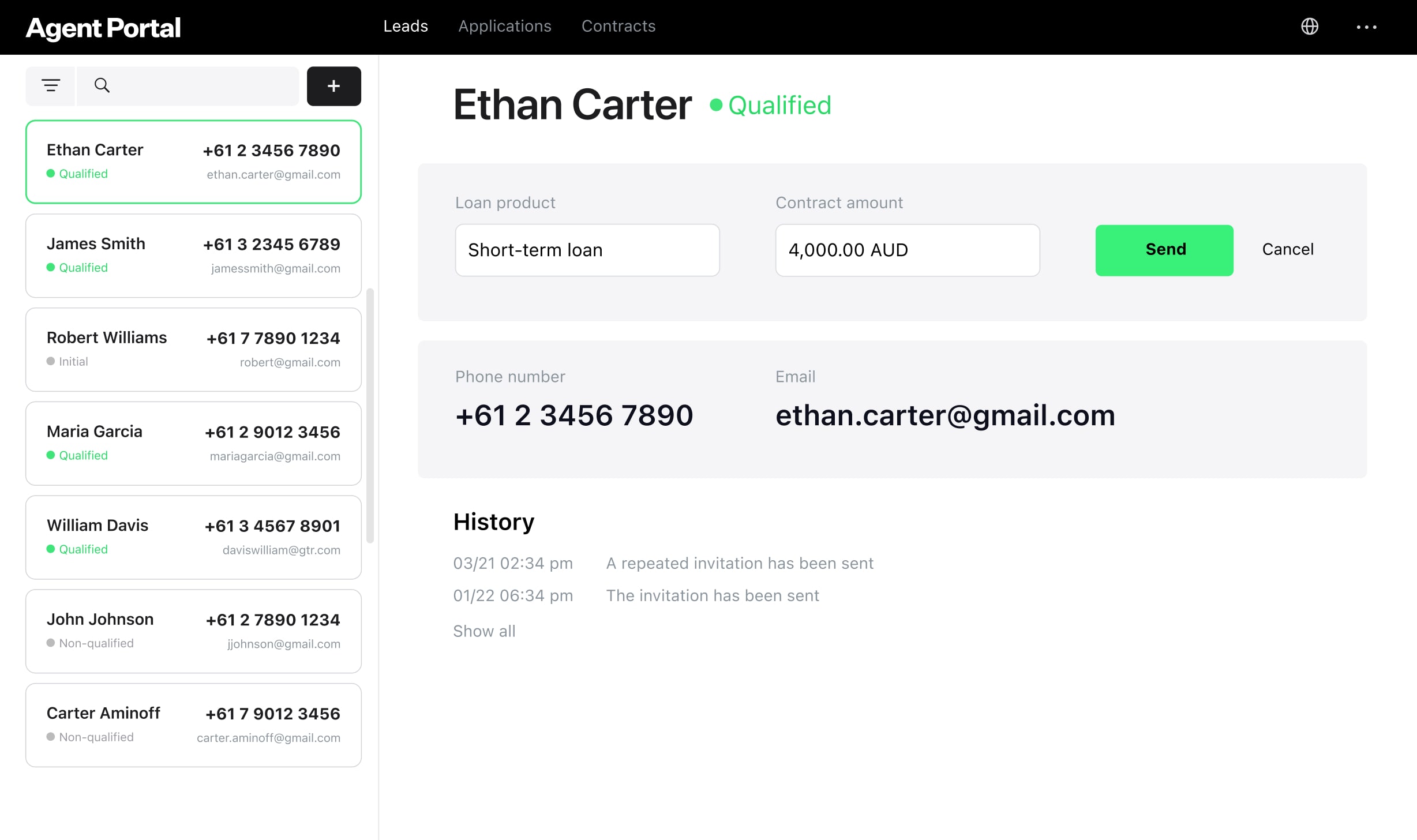

Agent Portal

Integrated plugin

Streamline your lending process

by capturing leads and providing preliminary loan calculations, guiding visitors effortlessly towards application submission. Our landing page seamlessly redirects users to the Borrower Portal for comprehensive loan applications and further processing. Initiate onboarding directly through your website, via agents, or through any integrated applications.

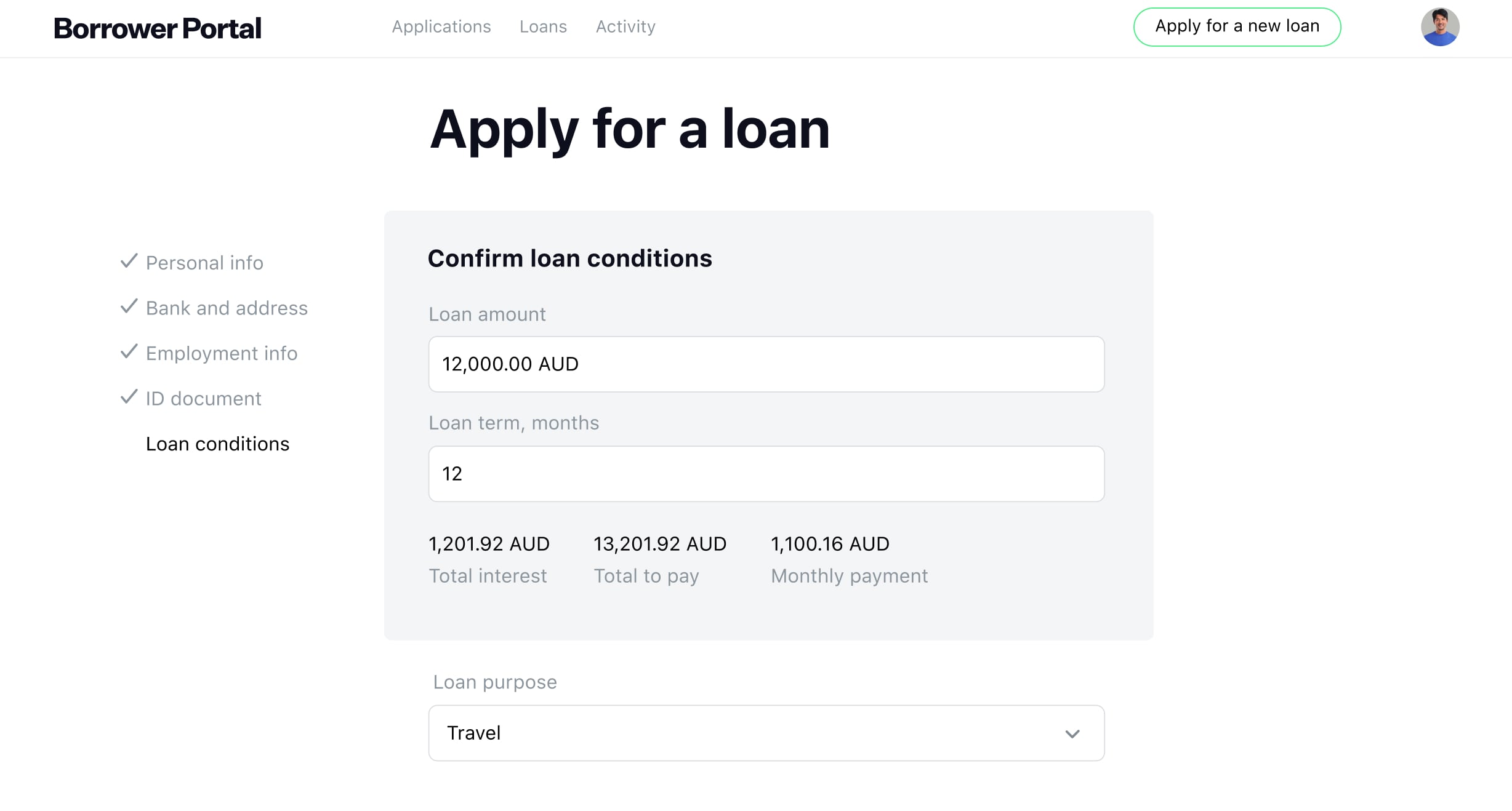

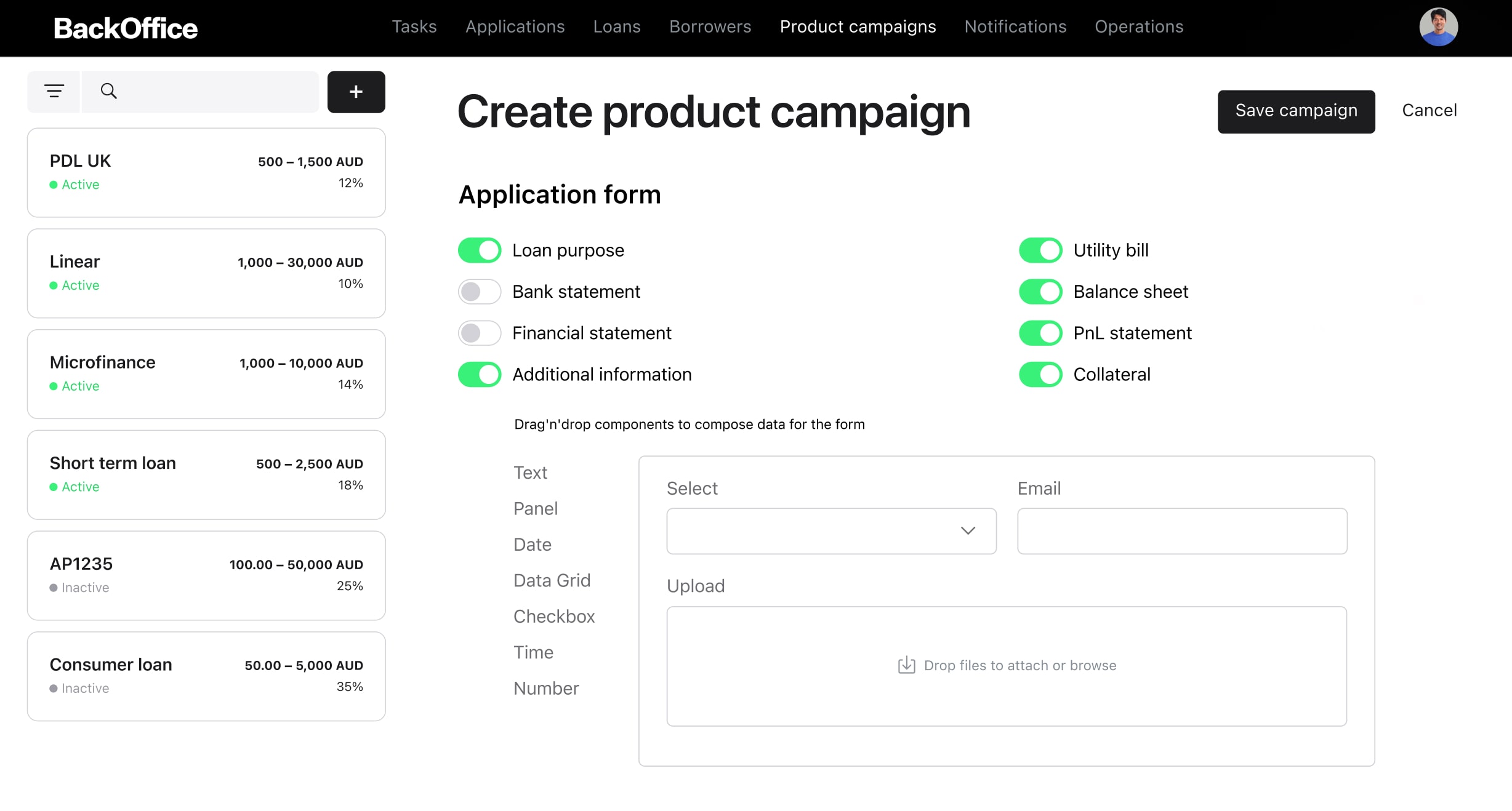

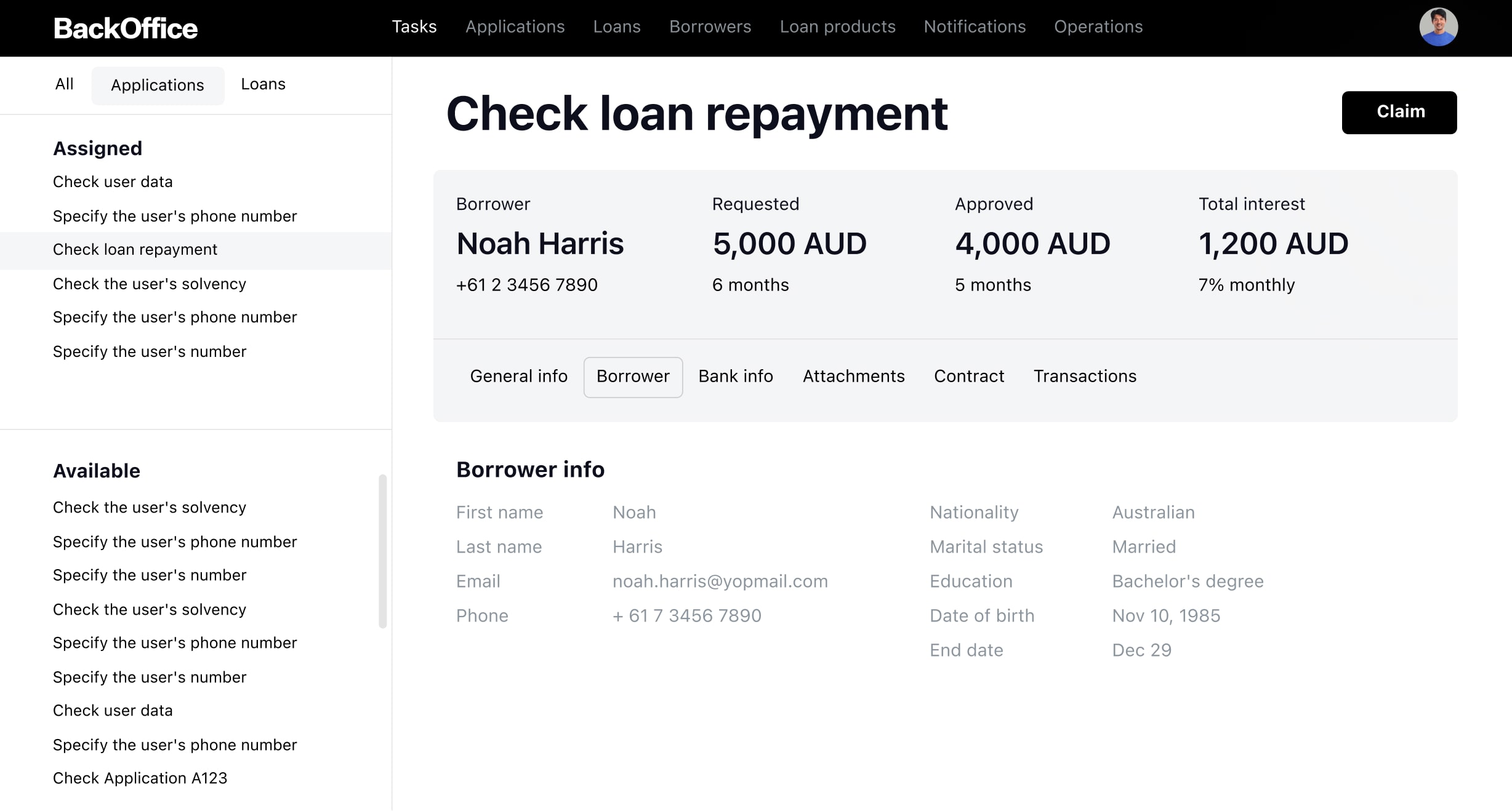

Loan origination

Ensure 24/7

borrower access

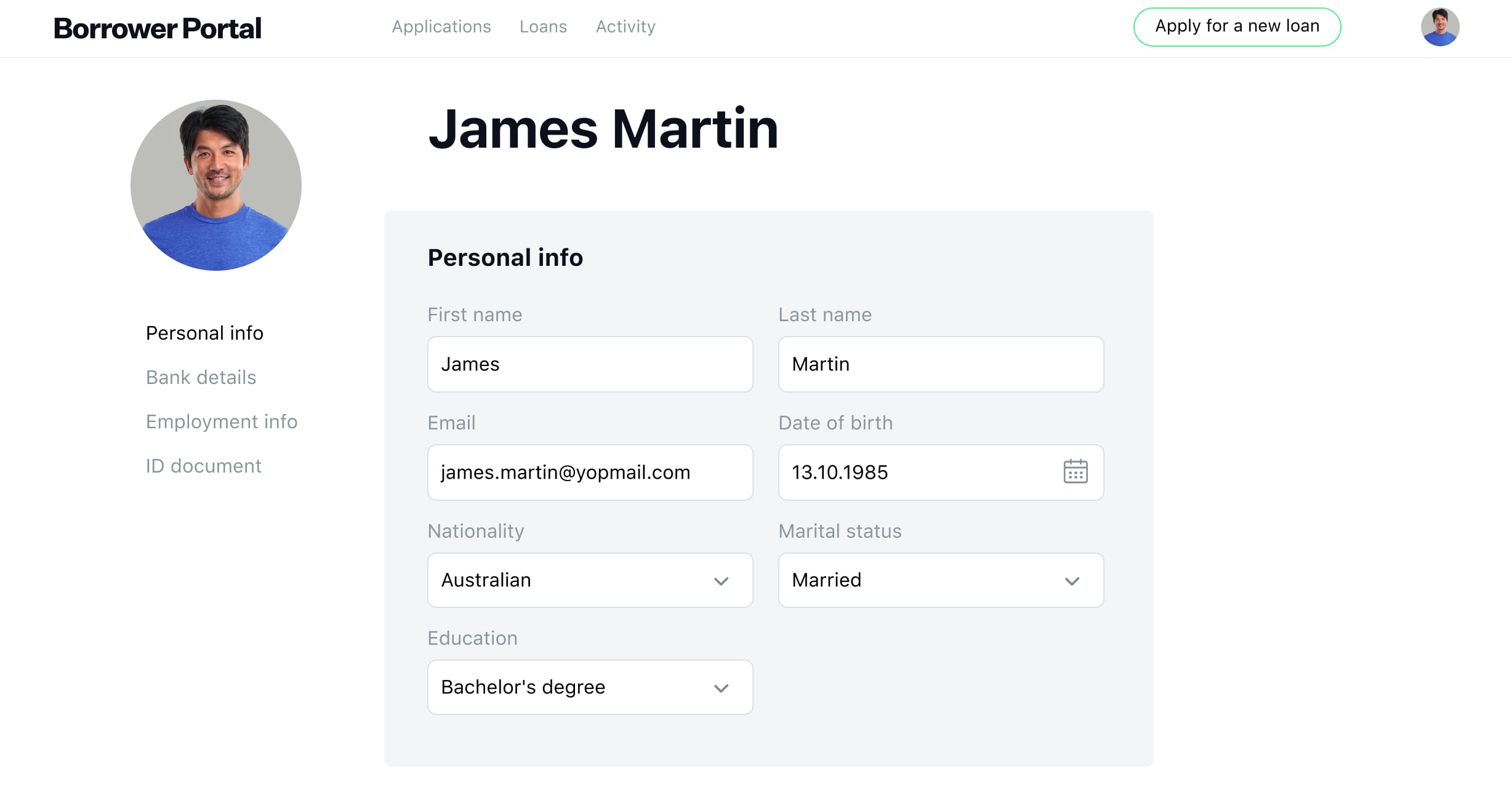

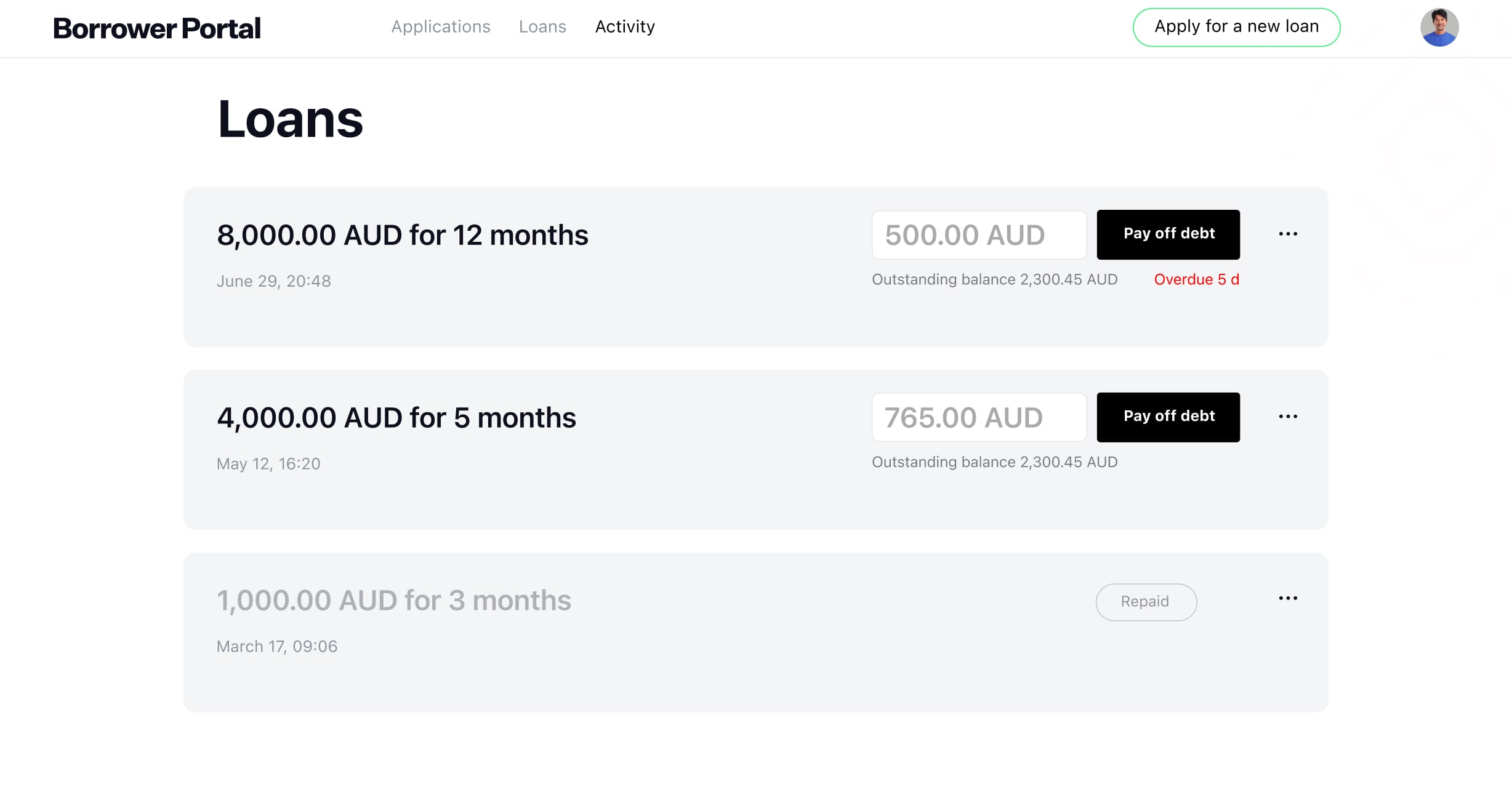

Application flow

Borrower profile

Activity

Decision-making

Empower your customers with an intuitive loan management experience.

Our Portal integrates with local KYC providers and connects with open banking and credit bureaus to deliver comprehensive financial insights. It supports rule-based applications and offers flexible options for document signing, whether online or offline. Customers can apply for loans, track their progress, and manage repayments from any location, at any time.

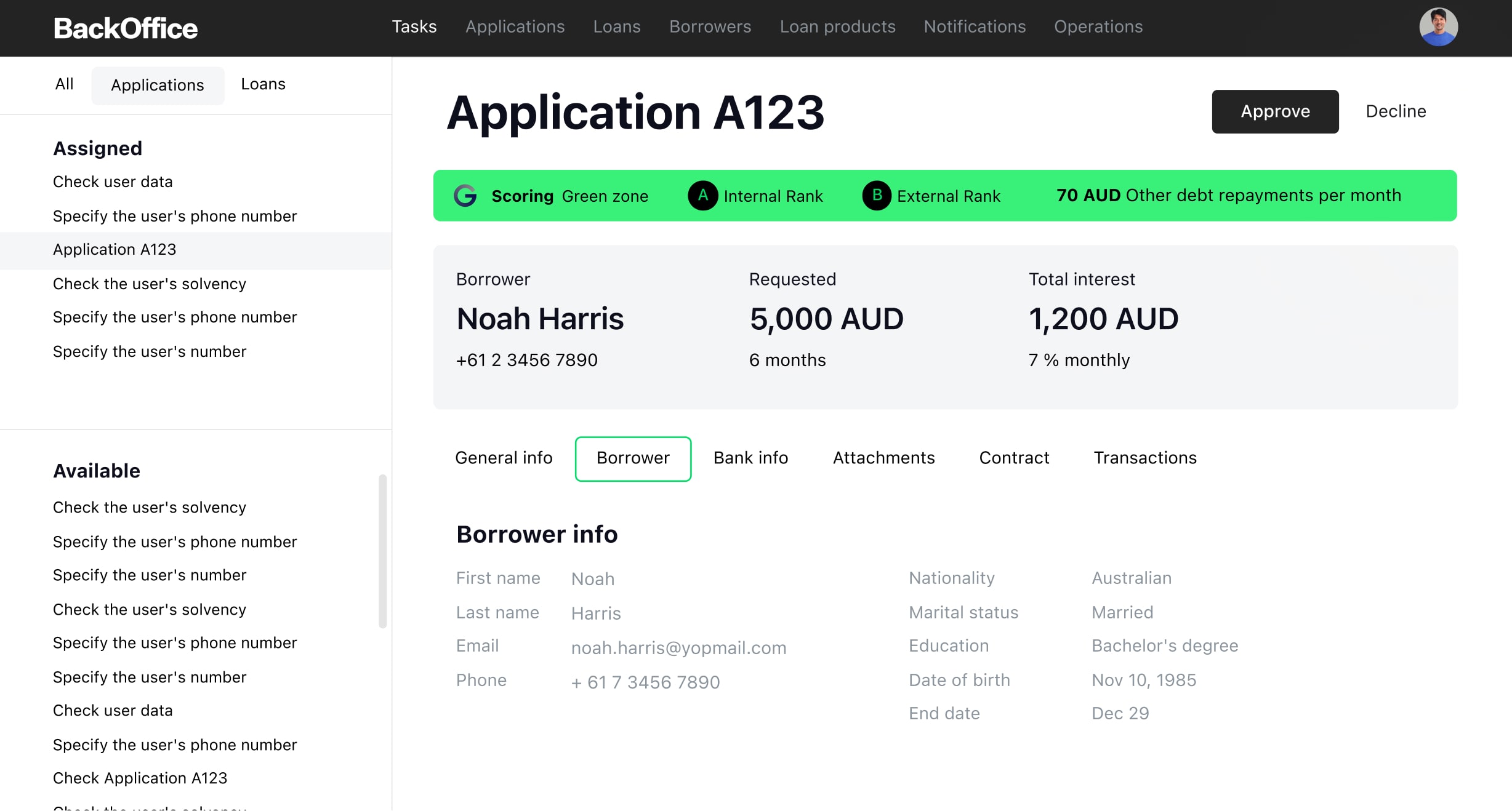

Optimize the core of your lending business with our loan management software.

Featuring end-to-end digital processes, including AI-enhanced verification, scoring, and underwriting, alongside automated decision-making, HES LoanBox streamlines every aspect of lending. Ensure an error-minimised workflow and gain enhanced operational insights with advanced task management tools and detailed reporting.

Obtain credit reports, risk evaluations, and financial information to make well-informed lending choices and efficiently manage credit risk

Open banking

Process payments swiftly and safely, handle transactions, and optimize financial operations using Square`s payment API

Payment processing

Enhance customer interactions and notifications via secure, scalable channels for efficient and effective communication

Notifications

Jumio’s identity verification, eKYC, and AML solutions combat fraud and financial crimes, ensure compliance, and expedite the customer onboarding

KYC

Generate, approve, and electronically sign documents faster with PandaDoc. Quickly get business documents signed using the electronic signature API

eSignature

Ondato provides identity verification, business onboarding, and client lifecycle management for streamlined KYC compliance

KYC

Australian lending market expertise

Our team of BAs has a decade of diverse financial experience, specializing in the Australian lending market and compliance nuances.

Why choose HES LoanBox

Kickstart online lending

90% of our Australian clients launch their online lending platforms and see a fast return on investment. Our loan management system is built for quick deployment and can be easily customised to fit your unique needs, ensuring compliance with Australian regulations and industry standards.

Seamless integrations

With extensive integrations tailored to the Australian market, HES LoanBox aligns with the unique compliance and operational requirements set by Australian regulatory authorities.

Customer support

Receive dedicated customer support to ensure your satisfaction. If you have any questions about our software for lending business, HES FInTech team is here to assist you. Count on us for issue resolution and guidance on optimal use.

Future-proof architecture

At HES FinTech, we are ISO 27001 certified and strictly follow the SDLC to ensure global security compliance. Our lending management software uses an advanced technology stack to guarantee stability and secure data storage for your business.

With HES LoanBox, banks and alternative lenders go the extra mile to provide an

enhanced customer experience for both retail and corporate clients. They also reduce

human biases in credit assessment and manage the entire process with maximum

efficiency—all in compliance with Australian regulatory standards.

44%

boost in staff efficiency

Why HES FinTech software?

Post-lauch support

We handle all software support, maintenance, and development in-house to guarantee the highest

quality of service.

European-founded company

HES FinTech has earned the trust of 102 companies across 32 countries. We deliver solutions

that meet their needs and foster business growth.

Australian clients and partners

The relationship we have built with regional industry players is the best testament of our commitment to excellence and reliability.

Our journey in Australia

HES FinTech has been our reliable technology partner since 2012. I believe much of our success is due to the well-architected HES LoanBox solution.

What types of loans can be managed using HES LoanBox?

HES LoanBox can manage a wide range of loans, such as personal loans, BNPL, home loans, auto

loans, business loans, and more. Our platform is designed to handle various loan products to

meet the needs of Australian lenders.

How does HES LoanBox enhance loan processing efficiency?

HES LoanBox enhances loan processing efficiency through automation and AI-powered tools. It

streamlines every step of the loan lifecycle, from origination to servicing, reducing manual

tasks, and enabling quicker decision-making, which leads to faster loan processing times.

Can HES LoanBox be integrated with our existing systems?

Yes, our API-rich platform allows for easy integration with various financial tools,

databases, and third-party services, ensuring a smooth transition and operation.

How secure is the data stored in HES LoanBox?

We prioritise data security and compliance with Australian regulations. Our software uses

advanced encryption and adheres to ISO 27001 standards for information security management,

ensuring that all sensitive data is protected against unauthorised access and breaches.

Since HES FinTech's foundation in 2012, our software has had zero data breaches.