Every business must start somewhere. However, it’s often the case that new businesses, especially if it’s the founders’ first business, struggle to gain access to the credit they need to expand and even survive.

Statistics show that access to financing is a significant restrictor when it comes to SME (small to medium enterprises) survival, but why is this and are there any solutions to this pressing problem?

According to the Consumer Financial Protection Bureau (CFPB), at least 45 million adults worldwide are ‘credit invisible.’ If we add this to the unbanked, those who certainly don’t have access to financial services, this could be as large as 1.7 billion. But why do these numbers matter?

Small and Medium-sized Enterprises (SME)

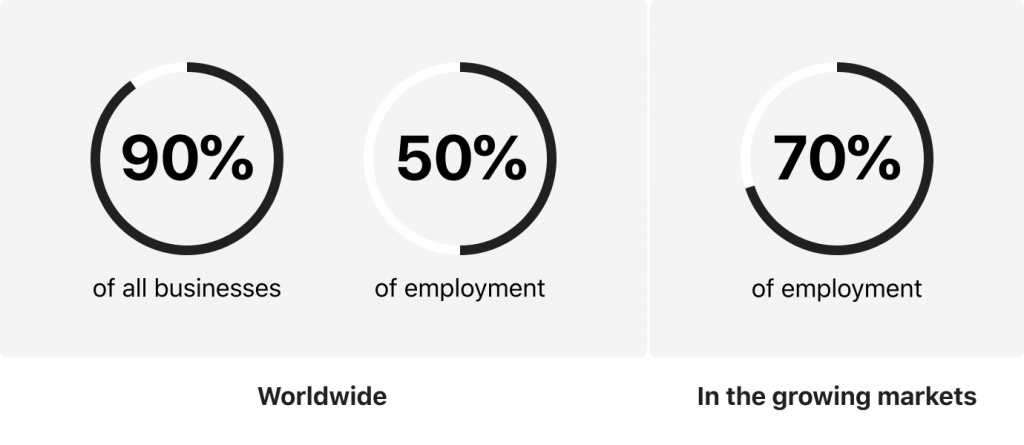

SMEs account for 90% of businesses worldwide and 50% of employment. For growing markets, their role is even more crucial as they provide 70% of all jobs. Unfortunately, the reality for many such businesses is they lack the financial tools they need for further growth. This either occurs as an inability to access any kind of access to credit, or only having access to unreasonable credit services (aka predatory lenders).

In essence, they become ‘invisible borrowers.’ Initially, you may be led to believe that these SMEs are irresponsible or made poor financial decisions to justify their situation. However, this is far from the case. In fact, it can result from:

Being younger and having a limited credit history

Having recently migrated to another country

Not having credit due to a paid-off mortgage

Being unbanked for a variety of reasons

Why Empowering SME Lenders with Alternative Credit Scoring is such an Issue?

How to Choose SME Lending Software and Stay on BudgetImproving access to credit for SMEs, especially those that are currently credit invisible, could lead to substantial economic growth both at a local, national ,and international level. As current providers of over 7 out of 10 of jobs in emerging markets, this can work to reduce the poverty level, increase the market, and help countries grow.

With such positive results, you might be wondering, “well, why haven’t we done something about it yet?” The answer is down to how credit is approved and distributed. Often credit via traditional brick and mortar providers is approved via the 5 Cs of credit: character, capacity, capital, collateral, and conditions, which is heavily influenced by a person’s credit history and credit score. Any issues when undertaking creditworthiness checks could result in a denial by the provider.

Steps SME Lenders Can Take to Improve Credit Access

That said, it doesn’t have to be this way. Indeed, many alternative lending providers are moving away from the traditional method of scoring creditworthiness and seeking more comprehensive and inclusive evaluation methods, such as ‘alternative data.’ And this trend could soon leap into the traditional financial sphere too.

So, what steps can lending providers take to become more inclusive and expand their pool of potential borrowers without increasing their risk?

Step 1: Analyze if your current lending policy and lending software are working

Before getting caught up in onboarding new technology and putting it to work, it’s essential to take a step back and evaluate how effective this solution is for your business and if it fits with your overall strategy. While initially, it might seem like a good idea to roll out alternative data and work from there, this can be a dangerous approach as you will need the correct systems in place to be able to analyze and work with this data for your benefit.

Come up with a strategy of how your business will utilize these deeper insights, how they can form an integral part of your business processes from now on, and how you plan to negate any expected or unexpected risks along the way.

Step 2: Consider the data you use to make decisions

As we said above, alternative data is changing how credit decisions are taken. So, what is alternative data? In essence, it is an expansive term to include additional data that has not been taken into account before. For example, payment behaviors, customer metrics, business statistics and more. By looking at these factors, the lending provider can gain a better picture of who they are lending to and the actual risk, rather than going off old-fashioned data. Adding alternative data solutions to your business doesn’t mean reinventing the wheel, in fact, it can be as simple as onboarding a solution such as GiniMachine, which automates the process and makes it a whole lot simpler.

Step 3: Leverage alternative data to make wider business decisions

Commercial Lending Trends 2023: Navigating the Evolving LandscapeWhen it comes to increasing your potential market, that doesn’t mean that you have to increase your risk exponentially. Instead, the decisions that you make by harnessing alternative data should be based on fact and help ensure a manageable level of risk to your business at the same time.

In addition, alternative data can be utilized to inform wider business decisions, such as targeting specific lending markets, SMEs for example, which preferential terms could be on offer and whether there are any other potential areas your business needs to explore.

Future of SME Lending Software: Making Invisible Businesses Seen

Undoubtedly, having the potential to lend to more borrowers increases the size of your potential market as a lending provider. Whether you come from a traditional financial background or are an alternative lender at heart, the latest solutions on the market can help support your business strategy and get the results you need.

Delivering credit access to previously invisible SME borrowers not only boosts cash flow to your service, but also increases the overall market by allowing small and medium enterprises to thrive and continue to support local and national communities and markets. Choose affordable SME lending software to simplify this process.